Despite a sharp decline on Friday, the S&P 500 managed to eke out another week of gains, inching up 0.13%. The Nasdaq Composite ended up almost flat, slipping 0.08%. All told, this was arguably a decent showing given last week’s hot inflation prints.

Perhaps most notably, Core PPI for April came in at 1.0% MoM, well above consensus expectations of 0.31%. PPI – wholesale inflation – is viewed as a leading indicator for consumer inflation. Yet as Lee put it, “as big as that number is and as shocking as it is, markets seem to have taken it in stride.”

Still, the PPI metrics matter not just for what they portend for the economy, but also because they still impact Federal Reserve policy. Speaking of which, Kevin Warsh was officially confirmed as the next chair of the U.S. central bank on Wednesday – just in time, because Jerome Powell’s last day leading the Fed was today. Fed funds futures trading implies that the markets now view a rate hike before the end of the year as a likely possibility, albeit barely – a 50.9% as of Friday afternoon.

Our Washington Policy Strategist Tom Block was non-committal about this possibility, but he admitted that “it’s going to be interesting to see how Warsh deals with Trump, because I doubt Trump is going to climb into a shell and stop talking about the need to lower interest rates.” Block also pointed out that the only FOMC member supporting a cut on April 29 was “the guy who’s going to leave to create the spot for Warsh.” Thus, if Warsh wants to deliver a rate cut for the president, it’s likely not going to be easy.

A big part of the rally we’ve seen in recent weeks has come from semiconductors. Lee and Head of Technical Strategy Mark Newton had similar views about this. Given the exuberance shown by chip stocks lately, Lee remarked that “to me, if I was looking to put fresh money to work. I’d rather be focused on the Magnificent Seven, which is only up 5% year-to-date. Or software, which is down 14% for the year. As we’ve noted before, I think the signs of capitulation are there for software.”

Newton concurred, asserting that “semis have gotten very, very stretched,” and consequently are, in his view, a poor risk-reward. “Historically, when they’ve gotten this high with regards to monthly RSI [momentum], they go sideways or down,” he noted. Consequently, he suggested that “it’s right to look at other areas such as software.”

Chart of the Week

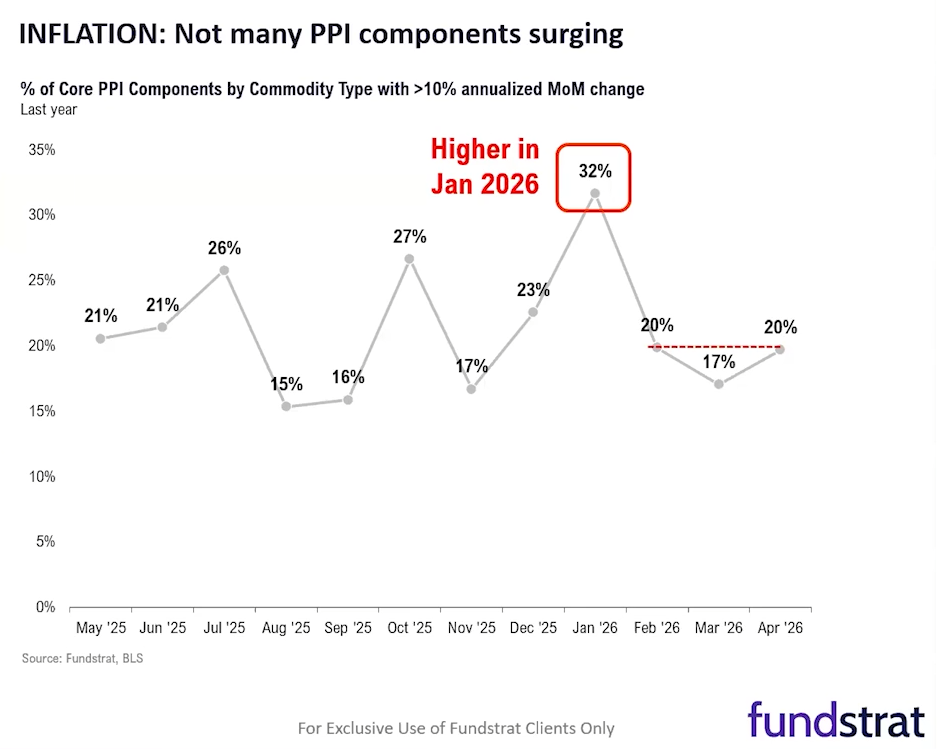

Although the extent to which core wholesale inflation (PPI) came in above consensus expectations was shocking, Fundstrat’s Tom Lee noted that a deeper dive into the PPI print shows less cause for alarm. “Only 20% of PPI components had a 10% annualized change,” he pointed out. As a point of reference, that’s roughly where it was in February, and the number was higher in the January PPI release. In fact, we’ve seen this figure higher on multiple occasions over the past 12 months, as shown in our Chart of the Week.

On a vote of 54Y to 45N the Senate confirmed Kevin Warsh to succeed Jay Powell as Fed Chair. Powell’s term as Chair ends on Friday but his term as Governor runs until 2028. At his last press conference Powell said he plans to stay on as a Governor. Warsh will be in place to chair the June meeting of theFOMC when the next rate setting decision will occur.

The push back to new all-time highs for SPX has not yet been reached for QQQ -1.76% ( 1 point away) but we’re continuing to see outsized strength from NVDA which is driving Technology while the rest of the market is down. 10 of 11 sectors are lower today and Financials, Energy, Utilities, and REITS are all down more than 1%, creating yet another negative breadth day. While Technology investors certainly are cheering the move in Large-cap Technology, the broader stock market is showing the weakest amount of overall breadth since mid-April and only 45% of all Russell 3000 stocks are trading above their respective 20-day moving averages. As shown below, momentum gauges like RSI continue to drop, while price is pushing higher which is certainly a technical negative. Yet, the key will be the break in the actual price trend and for now, that has not happened. Long term interest rates remain higher following this morning’s hot PPI print, but are down from earlier highs. Meanwhile WTI Crude has turned negative after retreating from earlier $103.67 down $2 dollars to $101.67. At this point, a close down under 7399 for S&P Futures (front month ES -2.38% _1 shown below) would be a minor trend break, while Ichimoku support lies at 7331. SPX cash has support from 7307 up to yesterday’s lows at 7338.54, and this cannot be violated without breaking the uptrend. So those are the key levels to watch on the downside. As for upside, SPX likely has strong resistance anywhere between here and 7465 (S&P Futures with RSI indicator shown below)

SOX -PHLX Semiconductor index has pulled back to near a support level from the uptrend from late March as of mid-day Tuesday. The area of importance lies near 11169 and until violated, trends are intact and very well could hold today into tomorrow. However, momentum has begun to turn down sharply and RSI has dipped to the lowest levels since early April. I think for today this is the more important development. There might not be a peak in price just yet but it looks like momentum is starting to give way and eventually this will likely result in prices moving lower. I think the EWY adjustment at the end of May could have importance as a negative catalyst for Semiconductors globally, and it’s important to watch for evidence between now and the end of May for a breakdown in both SOX and also EWY.

This research is for the clients of Fundstrat Direct only. Fundstrat Direct Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or Fundstrat Direct at fundstratdirect.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of Fundstrat Direct. At the time of publication of this report, Fundstrat Direct does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

Fundstrat Direct is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

Fundstrat Direct is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of Fundstrat Direct (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by Fundstrat Direct clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of Fundstrat Direct, which is available to select institutional clients that have engaged Fundstrat Direct.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

Fundstrat Direct does not have the same conflicts that traditional sell-side research organizations have because Fundstrat Direct (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by Fundstrat Direct and/or affiliates of Fundstrat Direct. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of Fundstrat Direct.

This research is for the clients of Fundstrat Direct only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but Fundstrat Direct does not warrant its completeness or accuracy except with respect to any disclosures relative to Fundstrat Direct and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where Fundstrat Direct expressly agrees otherwise in writing, Fundstrat Direct is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fundstratdirect.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.