SCOTUS Tariff Rejection Leaves Investors Largely Unfazed

Our Views

- We believe that Friday’s Supreme Court decision was a risk-clearing event that will ultimately be viewed by investors as disinflationary. Thus, we view the decision as positive for stocks. Because some tariff uncertainty remains, we view tech, software, and crypto as becoming more interesting as they have the potential to avoid much of the coming tariff messiness.

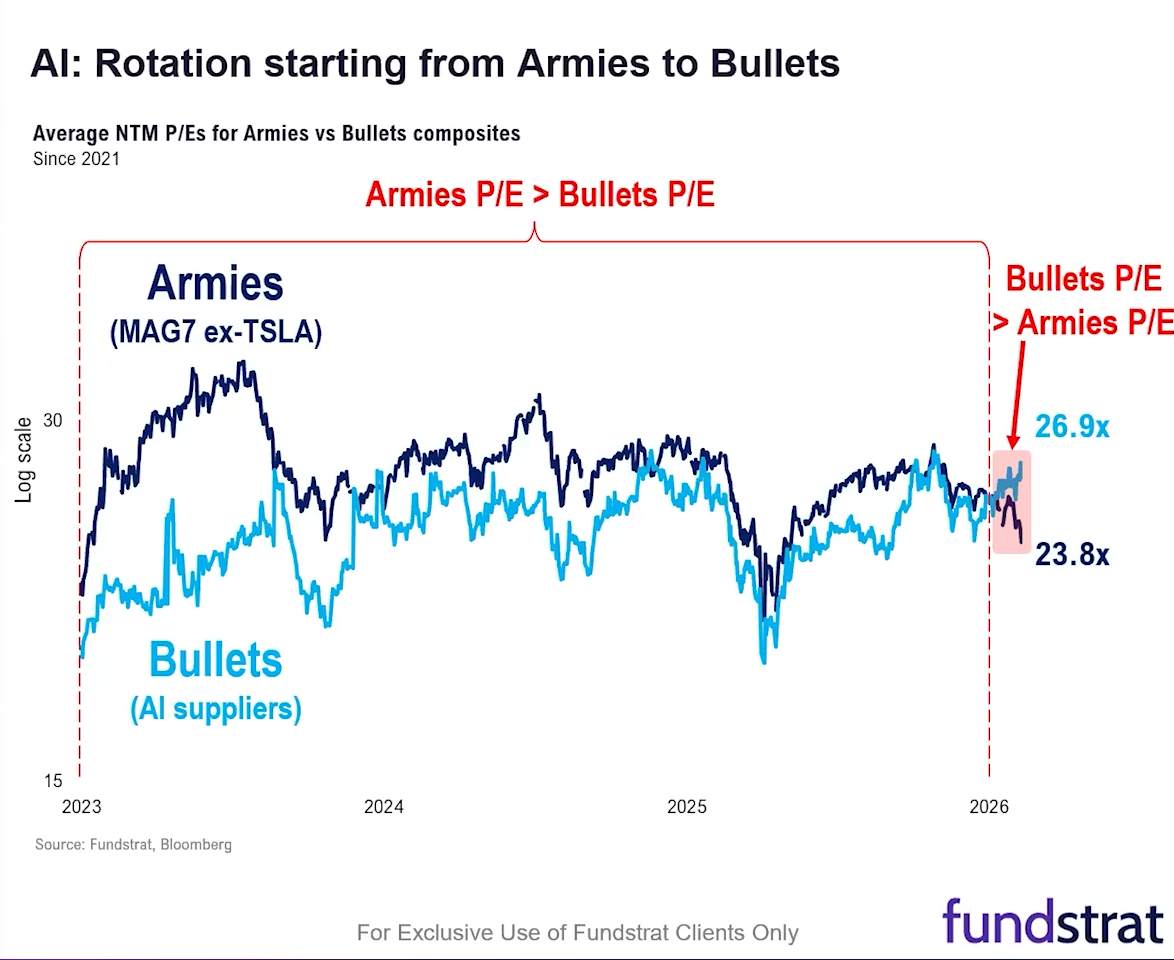

- The markets have felt choppy this month, and while part of that could be attributed to FOMO as gold prices climbed, we also have seen a rotation within the AI trade away from the “armies” (Mag Seven ex-Tesla) and toward “bulletmaker” companies that supply them. This rotation has now caused P/E ratio of bulletmakers to exceed that of the armies’, suggesting that it might be nearing completion.

- For these reasons, we would save dry powder and prepare to be buyers of tech (Mag 7), crypto, and software in the coming weeks as they make their way to their lows.

- Equity markets have remained range-bound over the last four months as part of underlying intermediate-term uptrends. While S&P in equal-weighted terms is far more bullish, the decline in Software and “Mag 7” has served as a headwind to both SPX and QQQ, immediately joining suit at new highs.

- Underlying volatility across equities has picked up measurably at a time when defensive positioning has grown stronger in recent weeks, and this has caused investor sentiment to grow more pessimistic from levels that previously had become more bullish.

- The good news is that broader market breadth and equal-weighted SPX have not broken down similarly to this time last year, nor in late 2021, which both preceded market selloffs. While Value remains preferred over Growth, and momentum is out of favor, there still look to be plenty of sectors that are working well.

- Overall, my bias is that early week equity weakness likely stabilizes by Wednesday, and begins to turn higher in a rally between now and early March. Upside should be capped near 7150-7200, and I feel like it’s difficult having much conviction in U.S. equities compared to much of the world, barring some immediate stabilization and strength out of technology.

- Despite crosscurrents involving geopolitical tension, declining cash positioning, and stresses in private credit, crypto has shown constructive relative strength this week. Bitcoin and select altcoins showed periods of outperformance versus equities and maintained a modest Coinbase premium, and to me this suggests steady spot demand. Relative resilience in the face of tightening financial conditions is notable.

- The macro backdrop remains mixed, with positioning still somewhat extended and several crosscurrents worth monitoring. At the same time, crypto’s relative resilience and improving regulatory prospects support a cautiously constructive near-term view.

- If AI adoption proves meaningfully disruptive to labor markets, fiscal stimulus would likely result. That path implies greater structural debasement risk over time. A smooth productivity boom that resolves debt imbalances without labor dislocation remains possible, but it requires a narrow and highly benign transition. On balance, a disruptive adoption path would likely be constructive for assets like BTC and ETH.

- SCOTUS threw out the centerpiece of President Trump’s tariff platform on Friday, which means it is likely to be a major topic in his State of the Union address next Tuesday.

- Republicans in Congress will likely face challenges in the effort to re-implement the tariffs by passing legislation, including from within their own party.

- Meanwhile, Trump has major foreign policy initiatives to consider as well, including the possibility of military action against Iran and efforts to rebuild Gaza.

Wall Street Debrief — Weekly Roundup

Key Takeaways

- The S&P 500 gained 1.07% this week, closing at 6,909.51. The Nasdaq Composite ended the week at 22,886.07, up 1.51%. Bitcoin slid about 1.61% from Monday levels, at USD 67,668.43 on Friday afternoon.

- Fundstrat Head of Research Tom Lee sees the Supreme Court's decision as largely good for stocks.

- Head of Technical Strategy Mark Newton sees stocks as still in a bull market, noting improved breadth across non-tech sectors.

"It is not the events in our life that define our character, but how we deal with them." – Eric Heiden, five-time Olympic gold medalist in speed skating

Good evening,

It was a trading week shortened by a holiday, but Friday undoubtedly made investors sit up and take notice. The S&P 500 rose 1.07% for the week, while the Nasdaq climbed 1.51% over the same period. Yet there seems to be little question that most impactful development this week came from the Supreme Court, which overturned the tariffs imposed by President Trump under the International Emergency Economic Powers Act on April 2, 2025. By a 6-3 vote, the Supreme Court ruled that the IEEPA does not give the U.S. president the ability to impose tariffs. (Justices Brett Kavanaugh, Clarence Thomas, and Samuel Alito dissented.)

Writing the majority opinion was Chief Justice John Roberts, who cited the major questions doctrine in his reasoning. This is a Supreme Court rule that in "extraordinary" cases with unusually significant economic and political significance, the executive branch (i.e., the president or White House) must have clear, explicit congressional authorization to take the action in question.

The decision most directly affects tariffs Trump sought to impose on what he called "Liberation Day." A number of other tariffs imposed last year are unaffected – for instance tariffs imposed based on Section 232, applying to imported steel, aluminum, copper, and autos. Lawsuits challenging those are still pending in lower courts. (Section 232 allows for executive-branch trade actions on the basis of threats to national security, rather than the IEEPA's focus on emergencies.)

For now, the decision arguably removes a sentiment overhang – a cloud of skeptical, nervous, or negative emotion that keeps investors cautious and on the sidelines. In this respect, "this is a risk-clearing event," Fundstrat Head of Research Tom Lee suggested shortly after the decision.

Hours after the decision was released, the president announced plans to impose a global 10% on all imports, regardless of country-of-origin, using authority granted by Section 122. This statute, which is being invoked for the first time ever, empowers the president to unilaterally impose a baseline tariff on all countries for up to 150 days, after which Congressional approval would be needed to sustain it. Still, Lee suggested that because the removal of elevated tariffs (at least temporarily) could have a disinflationary effect, it could also push the Federal Reserve in a dovish direction. Thus, the decision "is positive for stocks, in our view," Lee told us.

Yet looking further out, there is arguably a likelihood of market uncertainty as investors await clarity on the White House's long-term response. Trump has promised to re-enact the tariffs without the IEEPA, but uncertainty about which of the multiple potential long-term options he will pick could weigh on stocks in general. However, Lee noted that tech, software, and crypto "suddenly look more interesting, because they are not caught up in the tariff messiness." Also adding to idiosyncratic uncertainty are what happens to the trade deals the president brokered with other countries – and of course, there's the issue of whether refunds will be issued for tariffs collected thus far and if so, how.

As Lee noted late Friday morning, the decision was not exactly a surprise – and we arguably see this in the VIX, which largely stayed calm throughout the day. The S&P 500 and Nasdaq rose immediately after the announcement, retreated slightly in anticipation of Trump's remarks, and then continued to rise, ending the day up 0.7%. The Nasdaq Composite ended the day up 0.9%.

Because the crux of the decision is that Congress must authorize tariffs, we consulted our Washington Policy Strategist Tom Block about the potential paths forward. In his view, any regular Congressional approach to authorizing the tariffs would almost certainly end up filibustered by Senate Democrats, but aides to Republican legislators are researching the possibility of using "the Reconciliation process the Congress used to pass the One Big Beautiful Bill Act last year." If the tariffs can be framed as a budgetary issue, Reconciliation would enable them to be passed on a simple majority vote and without the possibility of filibuster. Block also pointed out the importance of paying attention to farm-state Republicans, whose constituents have been hurt by retaliatory actions taken by countries targeted by the tariffs.

Looking at the rest of the week's market activity, Head of Technical Strategy Mark Newton acknowledged that these days, "the market overall feels extraordinarily volatile, given the software, crypto damage, along with the recent decline in the Magnificent Seven." Yet, in his view, "it really has not been."

"This has been a bull market," he reminded us during our weekly huddle, "but it's just been important to be in materials and energy, of course, and also industrials and not just be in technology, where everybody is still overweighted." He reiterated, "I see a lot of great parts in the market. It's just not tech."

"For now, the equity market is holding up thanks to outperformance in many other sectors which have come to the text rescue, which I think is a good sign." In fact, he noted, "breadth is still sloping higher," citing the advance-decline ratio in the Russell 3000. Breakdowns in this metric preceded the April 2025 decline, as well as the late 2021 decline. Thus, in Newton's view, "if we start to see evidence of this breaking, then that'll be a bigger concern for the equity market."

As for tech, Lee has been discussing the recent rotation away from the metaphorical AI "armies" – basically the Magnificent Seven excluding Tesla, and into the so-called "bulletmakers" – those supplying the armies. As many will recall, this is a group that includes companies in energy, memory chips, infrastructure, and networking. As Lee pointed out in our Chart of the Week below, this rotation has resulted in the bulletmakers now having a higher P/E ratio than the armies. To him, this suggests that "we're pretty far through the rotation out of the Mag Seven." He stressed, "We don't necessarily want you to be a hero here, but I do think that means an opportunity is emerging when we rotate back into the 'armies', and I'd keep some dry powder."

Elsewhere

Warren Buffet went bullish on The New York Times, taking a 5.1% stake in the so-called "paper of record" on behalf of Berkshire Hathaway. The acquisition, disclosed in a regulatory filing, was one of his final decisions on behalf of BRK-B.B, as Greg Abel took over as CEO at the beginning of 2026. Some observers saw a certain symmetry in the decision, as Buffet worked as a paper boy in his youth – though NYT has admittedly posted some promising numbers in recent years.

Amazon is now the largest U.S. company by annual revenue, surpassing Walmart, claiming the title of the "Fortune 1 company." Walmart had held the top spot uninterrupted since 2009. It's yet another arena, one of many, in which Amazon and Walmart are widely expected to compete in the near-term.

James Talarico, seeking a Senate seat representing Texas, got an inadvertent boost from CBS after the network prohibited talk-show host Stephen Colbert from airing an interview with him. According to Colbert, the network's order was issued out of fear of triggering the FCC's "equal time" rule – and regulatory penalties. Late-night talk shows such as Colbert's have previously been viewed as exempt from this rule. The ensuing controversy, a debate over free-speech rights, was followed by millions of views on YouTube (far more than Colbert's usual television-audience numbers) and a significant surge in his fundraising efforts. Talarico is running in a Democratic primary against Rep. Jasmine Crockett, with both vying to oppose the incumbent Sen. Ted Cruz (R).

Former South Korean president Yoon Suk Yeol was given a life sentence after he tried to impose martial law on Dec. 3, 2024, an attempt that included ordering the military to seal off the National Assembly building to prevent lawmakers from meeting to overturn his decision. Prosecutors had been seeking the death penalty. Yoon still has the option of appealing the verdict or sentence to the Supreme Court,

Meta founder and chief executive Mark Zuckerberg took the stand in a civil lawsuit alleging that Instagram was deliberately designed to be addictive and harmful to the mental health of children. Zuckerberg denied any deliberate efforts to get users addicted to Instagram and objected to the assertion that social media can damage mental health. He also defended the company's age-verification efforts, though he expressed regret that they had not been implemented more quickly. The effect of social media on young users is being closely reviewed around the world, with social-media youth bans being considered or having been implemented in nine countries to date.

And finally: Brad Reese, whose grandfather invented the famed Reese's Peanut Butter Cups, has accused The Hershey Co. of hurting the Reese's brand reputation by changing the recipe to use lower-quality (and lower priced) substitutes, such as "vegetable oils and fats" instead of milk chocolate and "vegetable fats" instead of actual peanut butter. Cocoa prices have surged in recent years on global commodity markets. Hershey's said that the classic Peanut Butter Cups themselves remain unchanged, though it is true some other Reese's candies no longer list milk chocolate in their ingredients.

Important Events

Est.: 0.30% Prev.: 0.47%

Est.: 88.0 Prev.: 84.5

Est.: 0.3% Prev.: 0.7%