Lee, Newton Raise Year-End Targets Despite This Week's Stock Slide

Our Views

- May Core PCE shows ‘war inflation’ has probably peaked, with inflation mainly driven by ‘financial services.’ That arguably means that stock-market gains drove inflation. Ex-financials, core PCE was 0.22%, which is pretty close to the Fed’s target.

- To us, the week’s equity declines in chip and memory stocks represent buyable dips. These dramatic one-day declines of 6% or more have repeatedly been seen in the midst of bull markets, so to us, they are not a sign of a market top.

- We are giving a mid-year update and raising our year-end target for the S&P 500 to 8,000, up from our initial 7,700 outlook. This is mainly due to a higher EPS estimate for 2027.

- This week’s pullback looks buyable rather than the start of anything worse, with mega-cap Technology under near-term pressure but its intermediate-term trend still intact, and the broadening into Financials, Healthcare, Industrials, and Consumer Discretionary keeping the indices buoyant even on Mag-7 underperformance.

- Sentiment has improved in the last week, but isn’t yet frothy, with the AAII poll barely showing more Bulls than Bears as of Thursday.

- Overall, as we near the end of the first half of 2026, the improvement in structure, breadth, and momentum, alongside a mega-cap Technology group that is consolidating rather than breaking down, is why I’m raising my 2026 SPX target to 8,000 from 7,300 to mirror Tom Lee. In my view, it’s right to use this week’s dip to add exposure.

- The crypto selloff we saw this week was broad-based, but BTC appeared to have an additional idiosyncratic supply-driven component. That distinction matters because it makes me hesitant to aggressively buy the dip despite BTC again defending the ~$60k area.

- To me, HYPE remains the clearest relative winner, supported by continued traction in tokenized equity markets, while Solana’s tokenized-asset activity is worth monitoring but still too early to underwrite as something worthy of a trend change.

- More broadly, rate expectations and real yields remain elevated, shifting liquidity conditions in a restrictive direction, and STRC weakness keeps Strategy risk on the radar. While a tech-led bounce could bring parts of crypto with it, I struggle to see this as a place where you want to be a “hero.” I am remaining patient.

- Senate Republicans have left Washington, DC early after weeks of contention with President Trump.

- With the House scheduled to also leave next week for the July 4 holiday, DC is likely to be quiet for the next two weeks.

- The Supreme Court is due to wrap up its current session, with its decision on the president’s attempt to fire Federal Reserve Gov. Lisa Cook yet to be announced.

Wall Street Debrief — Weekly Roundup

Key Takeaways

- The S&P 500 slid 1.95% to 7,354.02 this week, while the Nasdaq Composite sank to 25,297.62, down 4.60%. Bitcoin was at USD $59,715.93 on Friday afternoon, down 5.61% from Monday levels.

- Fundstrat Head of Research Tom Lee cited a stronger EPS outlook as a key reason for his decision to update his year-end S&P 500 target.

- For his part, Head of Technical Strategy Mark Newton views improving breadth as a constructive signal.

"There is no top. There are always further heights to reach." – Jascha Heifetz

Good evening,

Tech stocks led a decline in the equity markets this week, with the S&P 500 ending the week down 1.95% and the Nasdaq Composite notching a steeper plunge of 4.60%. Yet the independent views of both Fundstrat Head of Research Tom Lee and Head of Technical Strategy Mark Newton remain constructive over the longer term. Both strategists raised their year-end targets for the S&P 500 to 8,000.

Lee raised his target first, telling us on Wednesday evening that the resilience of the market and the strong earnings growth shown by U.S. companies warranted an increase from his initial 7,700 target. As he pointed out, at the end of 2025, the consensus outlook for where the S&P 500 EPS would be at the end of 2027 was at $352. That outlook has now risen to $399.

Yet based on 2027E forward EPS estimates, the P/E for the S&P 500 is currently lower than it was at the beginning of the year. This reflects the fact that although the S&P 500 has advanced since the beginning of the year, the earnings outlook has arguably strengthened even more. As he put it, "we have a higher price, but based on these higher earnings expectations, the P/E of the S&P 500 is actually one turn lower. To me, this means that the market's cheaper now than it was on Jan. 1." In fact, Lee pointed out that while his original 7,700 target was based on a 22x PE multiple of forward EPS, his higher 8,000 target is arguably (and perhaps counterintuitively) more conservative, as it is based on a 20x multiple.

For his part, Head of Technical Strategy Mark Newton is inclined to agree in a directional sense. Newton's updated target matches Lee's 8,000, but it is a larger increase relative to his original target of 7,300. Despite declines in tech this week, breadth improved markedly, with Newton highlighting trend breakouts (both absolute and relative) in the consumer discretionary, health care, industrials, and financials sectors.

That's not to say Newton sees a straight line up. "The tech sector looks to be showing increasingly more evidence of consolidation," he told us, and "I fully suspect that technology does need to be watched carefully for evidence of giving way." His reading of various technical indicators and cycles suggests to him for now that "following some consolidation in technology, I see SPX pushing back to new highs and likely making its way to 8,000."

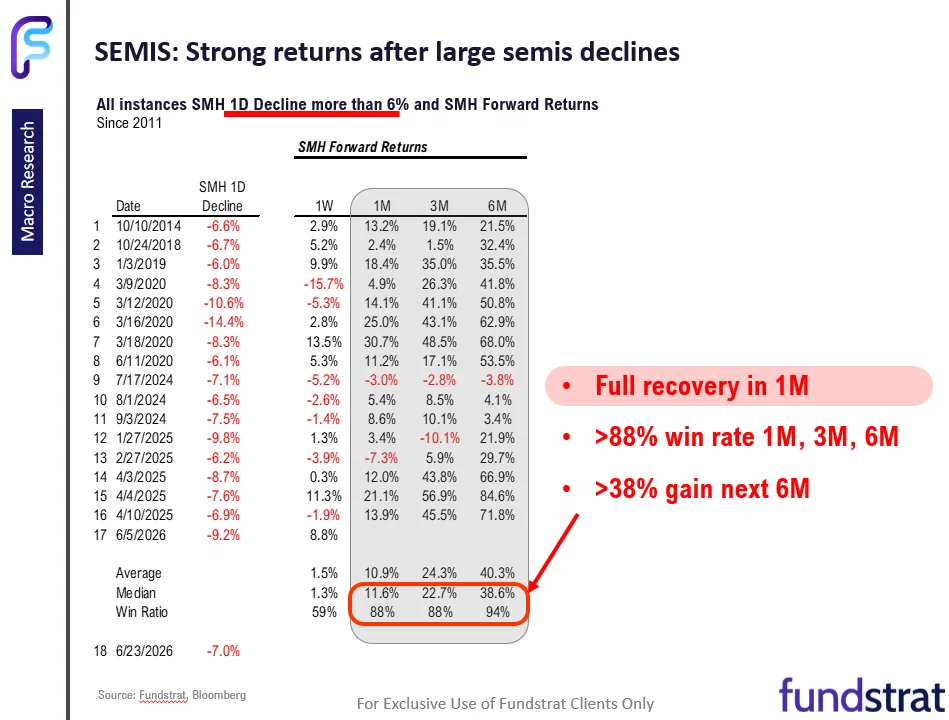

It's worth talking about technology and the week's declines. Semiconductor stocks SMH plummeted 7.0% on Tuesday. While the number is understandably uncomfortable to many, Lee pointed out that such moves have been far from rare in bull markets. In fact, since 2011, there have been 17 similar 1-day declines in SMH of 6% or more. The median gains one month after those declines are at 12%. Looking forward one, three, and six months later, the win ratio after these declines has been 88%, 88%, and 94%, respectively. To Lee, this means that such declines in chip stocks have "proven to be a buyable pullback basically every time." This is perhaps better illustrated through our Chart of the Week:

Elsewhere

Double earthquakes slammed Venezuela on Wednesday evening, and the death toll as of this writing was at least 920 and widely expected to rise to as high as 10,000 or more. The quakes, which registered 7.2 and 7.5 in magnitude, hit La Guaira province, north of capital city Caracas. Although the U.S. and other countries have begun sending help and supplies, aid efforts are being hampered by damage to Venezuela's main international airport and to roads leading to the affected areas.

The as-yet unresolved Iran war made its impact felt in Washington as four Senate Republicans crossed party lines to vote for a nonbinding resolution calling on President Trump to withdraw U.S. forces from the Iran conflict. Multiple sources reported that Trump engaged in a shouting match with Sen. Bill Cassidy (R-La.) on Wednesday, while also chastising the other Senate Republicans who voted for the resolution – Sens. Lisa Murkowski (Alaska), Rand Paul (Ky.), and Susan Collins (Maine). The House had passed the same resolution on a bipartisan basis earlier this month. It is worth noting that Cassidy has since reversed his position on the resolution.

OpenAI is reportedly considering a delay in its IPO, in large part due to the post-IPO declines of SpaceX shares. The AI giant had been expected to go public in the third or fourth quarter of this year, but the SpaceX price action, along with dampening retail sentiment over AI in general, has led some OpenAI executives to suggest waiting until next year.

The Supreme Court ruled in favor of Bayer in a liability lawsuit over the company's Roundup weedkiller, overturning a previous $1.25 million verdict that had sought to hold Bayer responsible for failing to warn customers that the product was associated with increased cancer risks. If upheld, that verdict would likely have strengthened the chances of tens of thousands of other similar lawsuits. While the plaintiff had argued that Bayer's federally approved labeling violated state laws, the Supreme Court found that federal law pre-empts those laws.

New York City Mayor Zohran Mamdani scored a political win within his own party, with the three candidates he backed scoring a clean sweep in Democratic primaries over rivals backed by the old-guard Democratic establishment. It's unclear whether these wins are conclusive evidence of a shift within the broader Democratic party outside of New York City, but the results are reportedly giving more centrist and moderate Democrats food for thought.

Anthropic openly accused China's Alibaba of a "brazen" distillation attack on its Claude model. Specifically, Alibaba was alleged to have trained its own model by illicitly harvesting responses from Claude, thus mimicking what Anthropic called Claude's "most valuable capabilities, such as agentic reasoning, software engineering, and long-horizon tasks." Multiple Chinese AI companies have been accused of distilling leading U.S. frontier models in the past.

Europe continues to grapple with what climate scientists have confirmed to be the hottest heat wave in recorded history. In France, hundreds of deaths have been linked to the blistering temperatures, leading to a ban on mass gatherings. Germany has seen roadways melted, while Sweden reported that rail tracks twisted in the extreme heat. The impact of this event will be felt well after the heatwave recedes, with output of agricultural products such as grain, fruit, and wine likely to be significantly lower than expected.

And finally: The International Olympic Committee has agreed to provide $10,000 stipends to each and every participant of the Summer and Winter Olympic Games, setting up a $140 million fund for the purpose. In keeping with the Olympics' mission of promoting an amateur ethos in athletics, the stipends are being characterized as grants rather than salaries. The first round of athletes eligible for the stipends will be those who participated in the February Winter Games in Milan-Cortina.