AI Capex Driving Market Leadership: The dominant theme continues to be AI. Over the past several weeks, we’ve received a combination of mixed real growth data, still-elevated inflation prints, crude holding above $100, and a more hawkish Fed posture. In a typical regime, this would present a challenging backdrop for risk assets. Instead, markets have continued to grind higher, suggesting that hyperscaler capex is overwhelming macro headwinds. MS estimates >$1T in annual AI-related capex by 2027, and this incremental spend is acting as a powerful tailwind for equities tied to compute, infrastructure, and data center capacity.

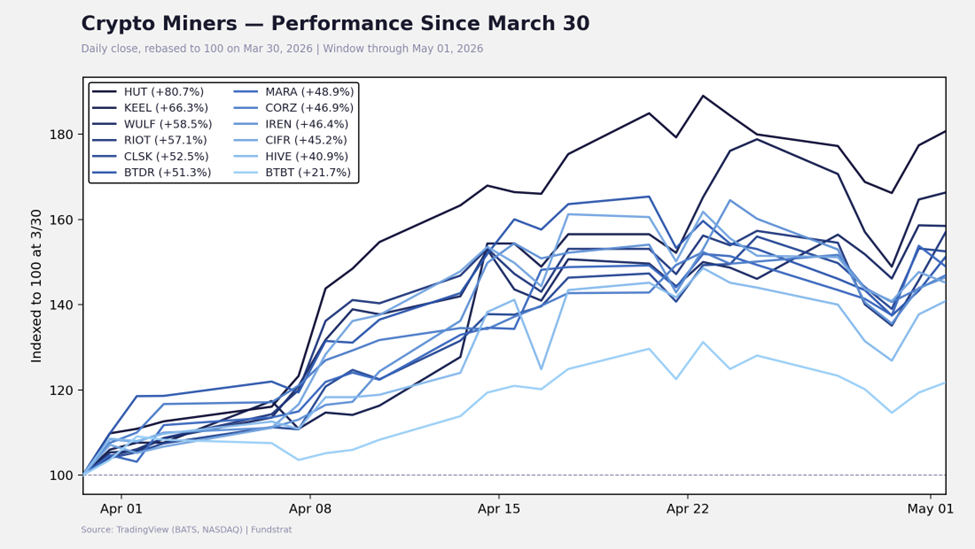

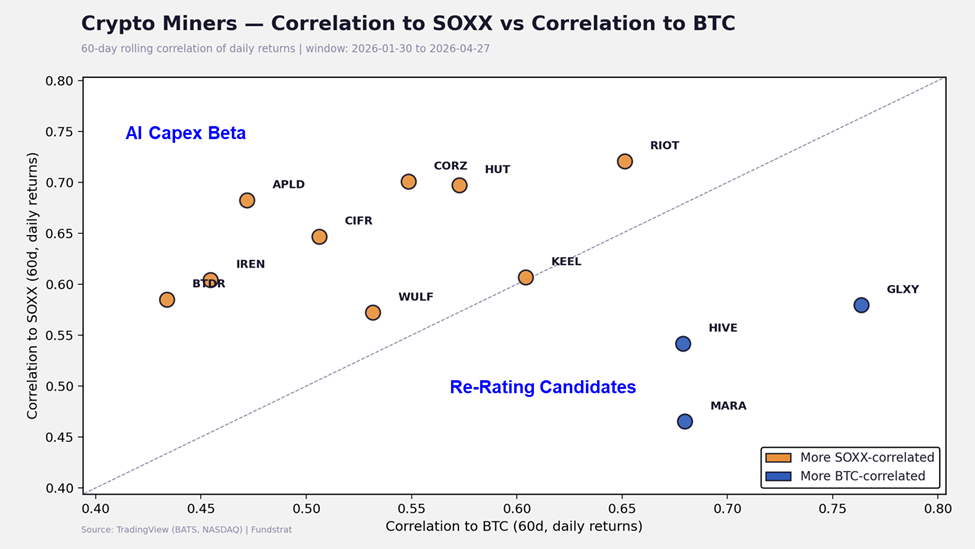

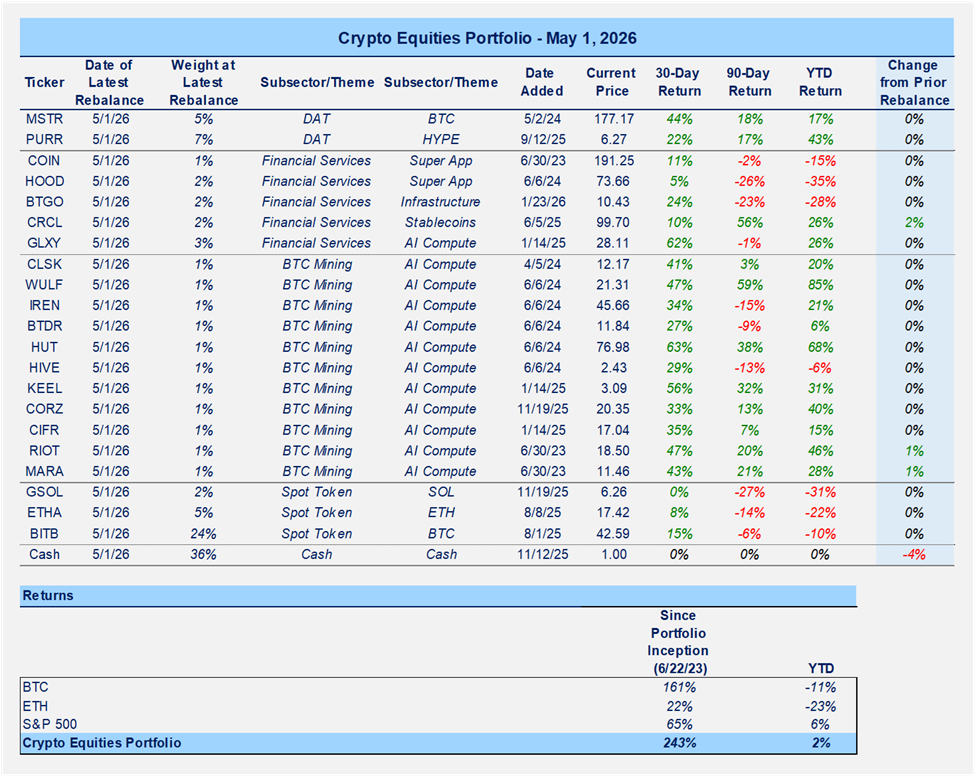

Miners Transitioning from BTC Beta to AI Beta: Within crypto-linked equities, miners have been clear beneficiaries of this shift. Many names are up 50%+ since the March lows, and importantly, this performance is increasingly disconnected from BTC price action. Correlation work suggests miners are migrating away from BTC beta and toward semiconductor/AI beta, reflecting their evolving role as compute providers. Rising GPU rental prices and sustained demand for high-performance compute reinforce this dynamic. Over time, we expect most miners to continue moving toward the “AI infrastructure” bucket in investor perception, which supports multiple expansion.

Adding MARA and RIOT to Round Out Exposure: Against this backdrop, we are adding 1% positions in Marathon (MARA) and Riot (RIOT) to the crypto equities portfolio. Both companies have outlined plans to transition a portion of their capacity toward servicing compute workloads, and we believe they are in the early stages of a broader re-rating. Given the strong performance across the cohort, we are not increasing total exposure at this time, but rather broadening participation to capture dispersion within the theme. Any near-term consolidation would likely be an opportunity to add further.

Revisiting CRCL with a More Constructive View: I had historically been somewhat measured in my view on CRCL. I still have my doubts. They have unfavorable economics, as they pay >50% of reserve income to their distribution partners. This compresses their margins materially and leaves them susceptible to rate cuts. However, there are a few developments that have pushed me in a more constructive direction:

- Inflationary data has pushed out rate cuts, and even if we do eventually get cuts, it would seem that the terminal rate is above historical Fed targets. I believe the market may be coming around to a terminal rate of 3% or higher. This pushes up longer-term revenues for the company.

- USDC has not declined with the broader crypto market, demonstrating use cases beyond speculation. While historically USDC was largely correlated with crypto prices, it holding up in the face of bear market price action suggests there is some non-speculative traction worth respecting, and the market is likely to hold CRCL to their ~40% USDC CAGR guidance.

- Recent regulatory developments around stablecoin yield and the inability for issuers to pass yield on to end customers may provide them with leverage to restructure their distribution deals with partners such as Coinbase, improving margins.

- As is evident, this earnings season, AI matters more than macro. The capex cycle is continuing to expand, with total capex budgets from hyperscalers now reaching ~$1.1T by 2027. There is also evidence in non-hyperscaler earnings that AI is proving to be a tailwind, particularly in the realm of agentic commerce (see Salesforce, Intel, Bandwidth Inc., and Twilio earnings calls).

- CRCL has expressed that a tailwind for them will be agentic commerce and agents transacting on-chain via USDC. I suspect this will be a major topic of conversation that they lean into next week.

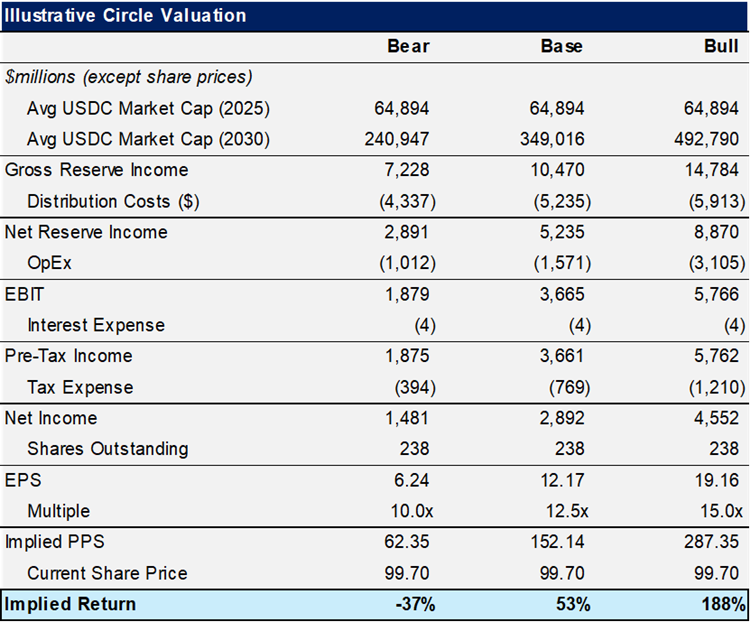

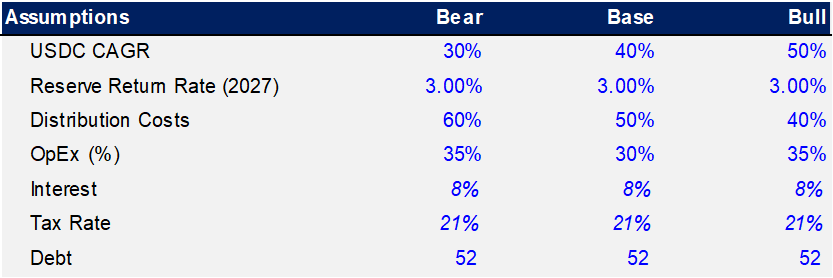

- Presently, in my model, if we assume 40% CAGR, a reserve return rate in 2030 of 3%, distribution costs moving to 50%, and net margins of 28%, and apply a 12.5x multiple to EPS, that gets us to ~$152 per share. This does not contemplate any non-reserve income that could develop via the Circle Payments Network.

- In summary, the thesis here, and the rationale for re-inclusion, includes: (1) terminal Fed funds rate expectations moving higher, (2) a potential regulatory moat from stablecoin yield language in the market structure bill, and (3) thematic tailwinds from agentic finance.

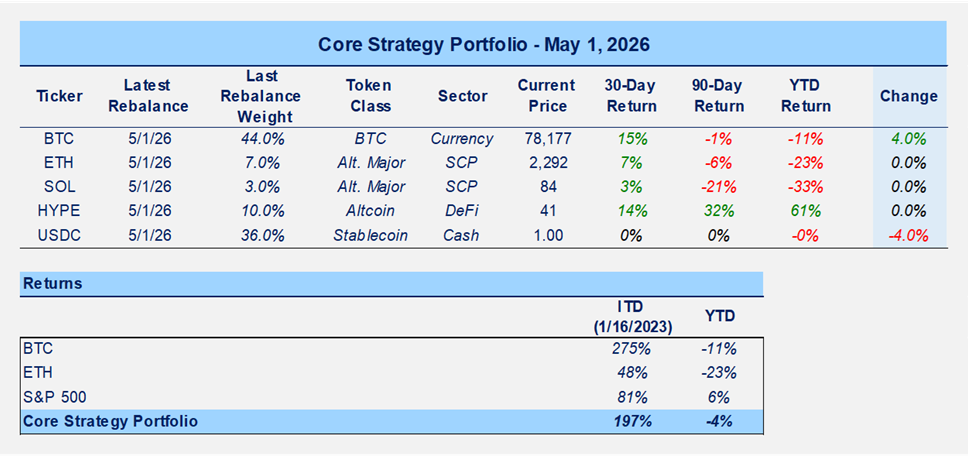

Portfolio Updates: We are adding a 2% position in CRCL, alongside the 1% additions to MARA and RIOT, funded from cash. In the token portfolio, we are reallocating 4% from USDC into BTC. The goal is to modestly increase risk exposure to names with AI adjacency while maintaining flexibility in the broader portfolios.

Tickers in this video: BTC -0.28% USDC -0.02% MARA RIOT CRCL

______________________________

PS: if you are enjoying our service and its evidence-based approach, please leave us a positive 5-star review on Google reviews —> Click here.