- Crypto Selloff Continues, But Capitulation Signals Less Convincing Than February: The crypto slide continued overnight, with BTC trading as low as ~$61k, ETH briefly falling toward ~$1,700, and SOL reaching the mid-$60s. Importantly, some of the relative outperformers that had largely resisted prior weakness, including HYPE, finally began to participate in the drawdown. Whenever we see a rapid selloff of this magnitude, the natural question is whether markets are exhibiting signs of capitulation that might justify getting more aggressive. While there are certainly some indicators moving in that direction, I struggle to see the same type of “hold your nose and buy” setup that emerged in early February.

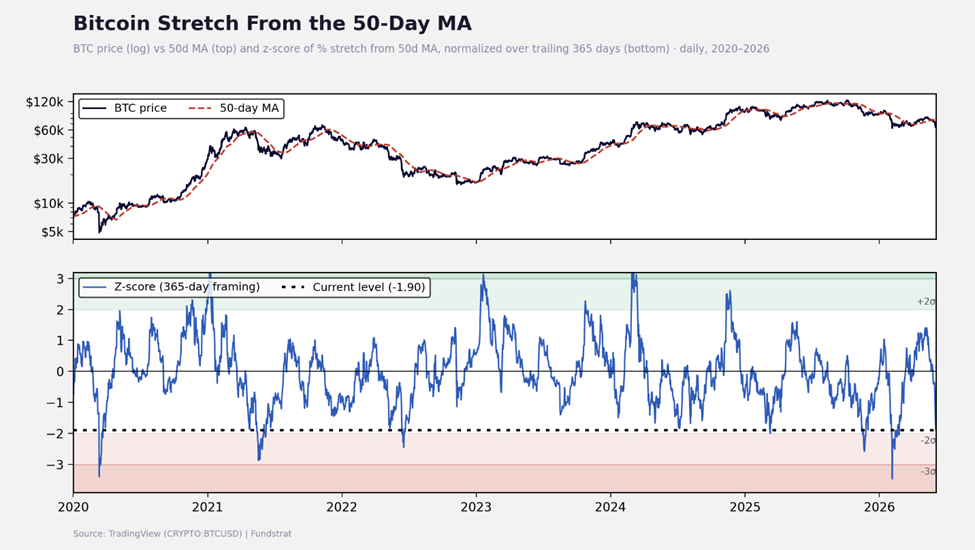

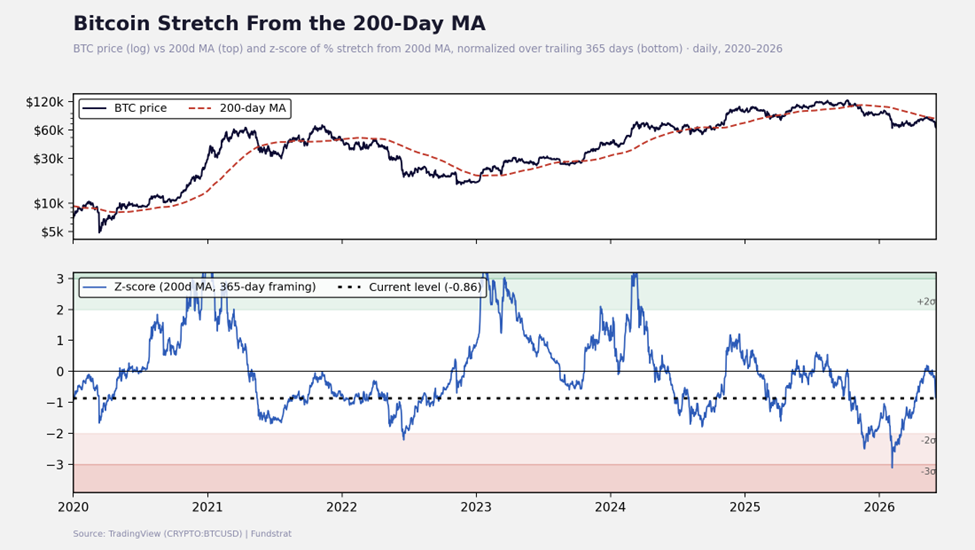

- Price Relative to Trend Remains Less Extreme: One notable difference between today’s environment and February is how BTC is trading relative to its major moving averages. During the February selloff, BTC traded more than three standard deviations below its 50-day moving average and reached similarly extreme levels relative to its 200-day moving average. This time around, despite the severity of the recent decline, those readings have been considerably more muted. While part of that reflects the fact that we are further into a broader downtrend and moving averages have adjusted lower, the signal remains materially less extreme than what we observed during prior washout events.

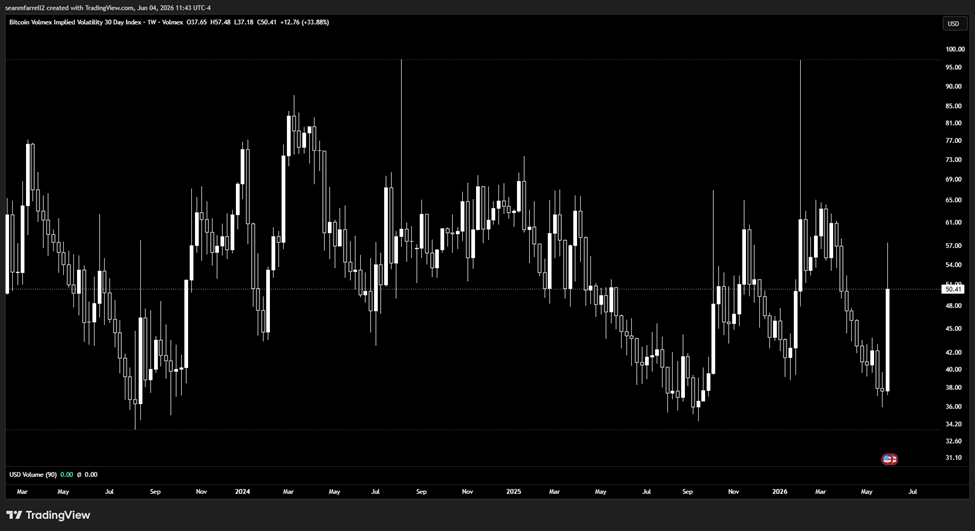

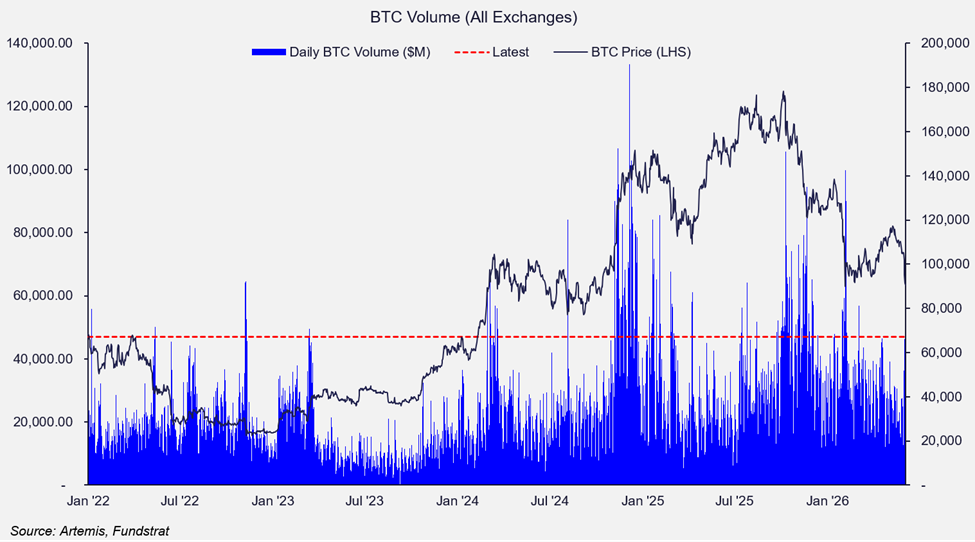

- Volatility and Volume Profiles Tell a Similar Story: The same pattern appears in options and volume data. Back in February, Bitcoin implied volatility index briefly approached 100, while similar spikes occurred during prior major drawdowns. This time around, implied volatility peaked in the high-50s before retreating. Likewise, spot trading volumes have increased meaningfully over the past several sessions, but remain below the levels typically associated with major capitulatory lows. Taken together, the evidence suggests stress is building, but not necessarily the type of indiscriminate panic that often accompanies tradable lows.

- Perpetual Futures Markets Have Seen Significant Deleveraging: One area where we have seen more convincing signs of stress is within derivatives markets. Long liquidations across perpetual futures markets have accelerated sharply and are now approaching levels last seen during the October drawdown. This confirms that a meaningful amount of leverage has been flushed from the system over the past several days. While constructive, I do not think this factor alone is enough to offset the more muted signals coming from spot markets, volatility measures, and broader positioning indicators.

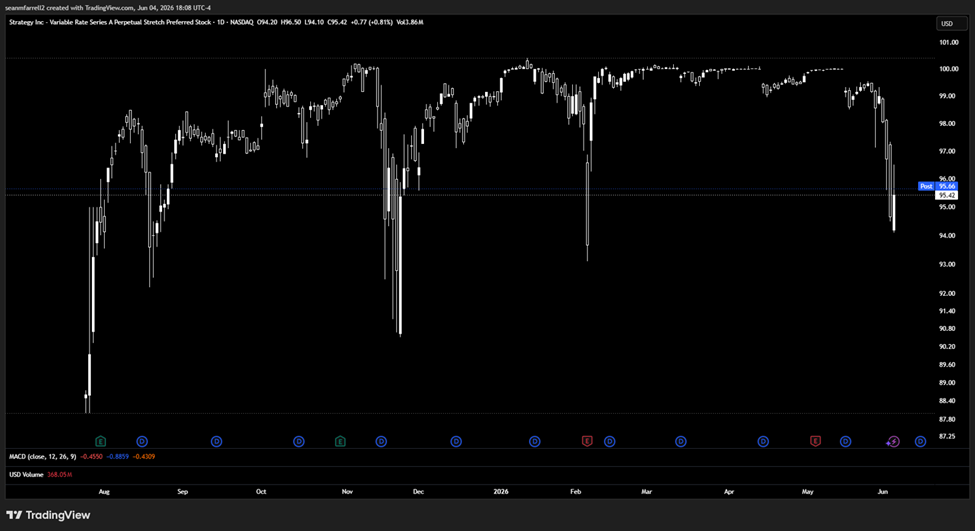

- Strategy Remains a Key Variable: The most important idiosyncratic risk facing crypto remains Strategy and STRC. The good news is that STRC closed modestly above yesterday’s levels and MSTR managed to finish the session higher. However, STRC remains materially below par, suggesting investors remain uncomfortable with the current reserve situation and the company’s ability to continue supporting the preferred security without additional capital raises. One development I will be watching closely is whether next week’s 8-K filing reveals substantial common stock issuance and meaningful replenishment of the USD reserve. If that occurs, it would likely help alleviate some of the fears currently weighing on crypto markets.

- Macro Backdrop Less Supportive Than Prior Washouts: Another important distinction relative to February is the broader market backdrop. The recent crypto drawdown is occurring after a powerful rally across broader risk assets. Meanwhile, traditional risk measures remain near cyclical lows. The VIX closed below 16 today, versus approximately 22 during February’s selloff and above 20 during the October drawdown. In other words, crypto is currently experiencing significant stress while broader risk markets continue to exhibit relatively little stress. This is very different from the backdrop that accompanied prior crypto washouts, where broader risk sentiment had already deteriorated materially. If we begin to see consolidation in equities or AI-related leadership groups, it could create an additional headwind for crypto.

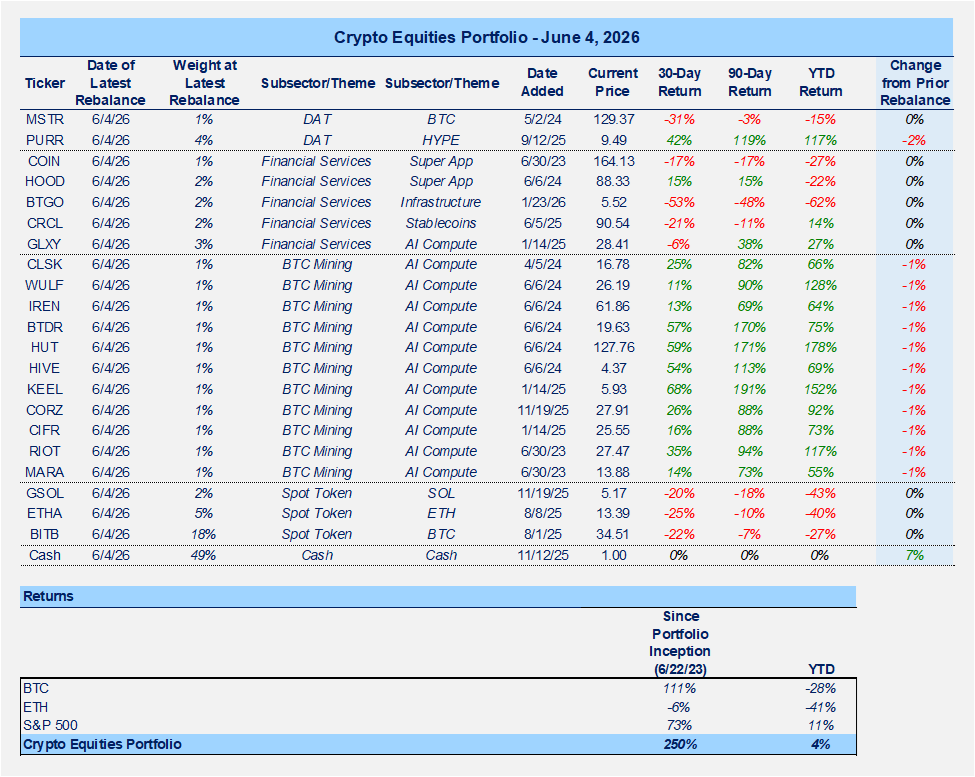

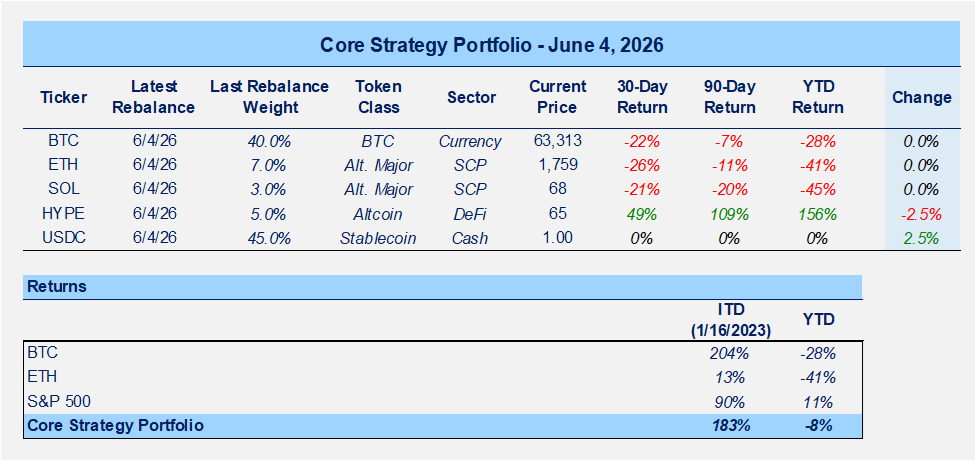

- Taking Additional Profits in HYPE and Miners: Given the combination of less-conclusive capitulation signals, unresolved Strategy-related risks, and the possibility of broader market rotation, I believe it is appropriate to continue harvesting gains from some of the strongest-performing areas of the portfolio. Within the token portfolio, I reduced HYPE from 7.5% to 5%. Within the crypto equity portfolio, I further reduced PURR and trimmed allocations across the mining basket. This is not a cyclically bearish call on these assets. I think there will be another chance to lean into these names. Rather, it reflects a desire to preserve gains, increase flexibility, and recognize that several of these positions have materially outperformed during a period when the broader market backdrop is becoming more challenging.

- Bottom Line: While there are certainly signs of stress and some evidence of capitulation emerging within crypto markets, the overall setup is materially less compelling than what we observed during the February drawdown. That does not mean prices cannot bounce from current levels. In fact, a meaningful short-covering rally remains entirely possible. However, from a risk/reward perspective, I continue to favor patience on the majors while harvesting gains from recent winners and maintaining additional flexibility until either capitulation becomes more convincing or some of the key idiosyncratic risks begin to resolve themselves.

Tickers in this video: BTC -1.29% ETH -2.36% SOL -2.76% HYPE -2.01% PURR 0.01% STRC MSTR

______________________________

PS: If you are enjoying our service and its evidence-based approach, please leave us a positive 5-star review on Google reviews —> Click here.