- Progress on the Iran Front Improves the Backdrop for Liquidity-Sensitive Assets: The biggest story over the past several days has been continued progress toward an interim peace agreement between the U.S. and Iran. While there are still reasons to approach the deal with skepticism, particularly given the negotiation period and the general headline volatility, markets appear increasingly willing to give the administration the benefit of the doubt. Crude oil has rolled over meaningfully, Treasury yields have moved lower, and broader risk assets have responded favorably.

- The Timing Could Not Be Better for the Fed: The decline in crude is particularly important ahead of this week’s FOMC meeting. Chair Warsh enters his first meeting facing a difficult balancing act between inflation that remains above target and a desire not to let elevated short-term rates stymie the economy. Lower energy prices, weakness across parts of the commodity complex, and the lack of meaningful inflation pass-through into core CPI provide him with greater flexibility to frame recent inflation pressures as potentially transitory. While I still expect relatively hawkish projections from the rest of the FOMC, the odds of a “dovish hold” appear higher today than they did a week ago.

- The Rates Market Is Beginning to Reflect This Possibility: Over the past several trading days, Fed Funds futures have started to remove some of the hike risk that had been priced into the curve. We have discussed for much of this year how crypto has been fighting a less supportive liquidity backdrop. If crude continues to weaken and the Fed adopts a more balanced tone, there remains meaningful room for easing expectations to rebuild across the rates market. This does not guarantee higher crypto prices, but it does represent an incremental improvement in the environment relative to where we stood several weeks ago.

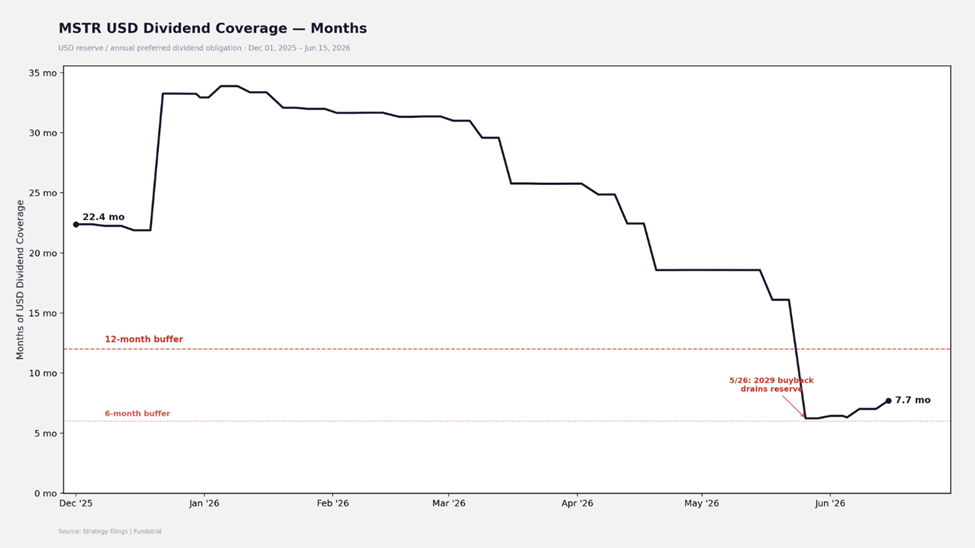

- Strategy Has Stabilized, Even If the Flywheel Has Not Fully Returned: The most important crypto-specific development remains Strategy. Last week, we discussed the company’s decision to split common stock issuance proceeds between BTC purchases and rebuilding the USD reserve. This week’s filing suggests that the pattern remains intact. Strategy once again raised roughly $200M through common stock issuance, allocating approximately half toward BTC purchases and half toward reserve replenishment. While these flows are unlikely to generate significant incremental BTC demand in the near term, they do materially reduce concerns surrounding a recursive unwind scenario and provide a clearer roadmap for rebuilding confidence in the preferred structure.

- Reserve Coverage Remains the Missing Piece: The key challenge is that reserve coverage still sits below the level that I believe would fully restore investor confidence. The reserve now covers roughly 7.7 months of STRC dividends, a meaningful improvement from recent lows but still well short of the ~12-month threshold that appeared to support investor confidence earlier this year. Until STRC trades back toward par, it is difficult to envision this channel generating the same magnitude of BTC demand that investors became accustomed to during the first half of the year.

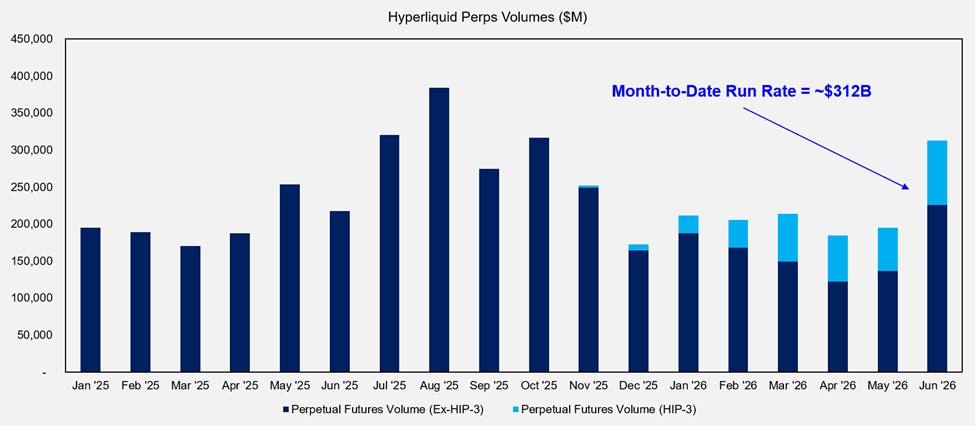

- Hyperliquid Continues to Strengthen Its Position: While BTC demand remains somewhat constrained, Hyperliquid continues to stand out. The SpaceX pre-IPO market generated significant volumes and garnered a lot of attention, further validating the tokenized equity narrative that has increasingly become a differentiating factor for the platform. More importantly, Hyperliquid appears to be attracting attention from a broader audience than it was several months ago. Conversations with investors who sit at the intersection of TradFi and crypto increasingly include Hyperliquid, suggesting the protocol may be beginning to tap into a new cohort of market participants.

- Fundamentals Continue to Support the HYPE Thesis: Beyond the narrative, the operating performance remains impressive. Through June 14th, Hyperliquid generated roughly $150B in perpetual futures volume, implying a monthly run rate north of $300B. Those are volumes more commonly associated with much stronger market environments and translate directly into protocol earnings and tokenholder buybacks. While valuation remains sensitive to future growth assumptions, the combination of strong fundamentals, expanding awareness, and continued product traction suggests there is reason to believe the worst of the recent HYPE correction may already be behind us.

- Bottom Line: I am not yet rushing to deploy dry powder. However, the tactical setup appears meaningfully better than it did a week ago. Geopolitical tensions are easing, which should allow Warsh to approach Wednesday’s press conference with a more dovish tilt, and there remains meaningful room for easing expectations to rebuild in the rates market should he take that path. Further, despite my HYPE profit-taking two weeks ago, there is reason to believe the worst of that correction may already be behind us. While I still think patience is warranted on the majors, I find myself incrementally more constructive than I was several days ago.

Tickers in this video: BTC 0.64% HYPE -1.77% STRC MSTR

______________________________

PS: If you are enjoying our service and its evidence-based approach, please leave us a positive 5-star review on Google reviews —> Click here.