Note: As part of our transition from FS Insight to Fundstrat Direct, my notes will transition from sean.farrell@fsinsight.com to sean.farrell@fundstratdirect.com. Please add the new address to your contacts or safe sender list to ensure uninterrupted delivery. The research and insights you rely on will remain exactly the same — only our name and sender address are changing. If you have questions, please visit our FAQ here.

See End of Note for Comments on Portfolio Changes

Context: Framing My YTD Views on Crypto

Before discussing the current setup, I think it is worth stepping back and summarizing my views on the crypto market over the course of the year to provide context for this note.

Coming into 2026, my stance on crypto was somewhat measured. This caution was driven primarily by several factors. First, positioning across broader risk markets appeared stretched. The VIX was subdued, the MOVE index was near cyclical lows, cash allocations were historically low, and credit spreads were near historical lows. Second, these positioning dynamics were unfolding in the presence of several identifiable volatility catalysts, including government shutdown risks, trade policy uncertainty, questions surrounding AI capex sustainability, and ongoing concerns regarding the trajectory of Federal Reserve leadership.

Third, I had growing concerns around market flows. Strategy was trading close to 1x mNAV, raising the possibility that its ability to raise capital for incremental Bitcoin purchases could become constrained. At the same time, miners were increasingly selling into rallies as they raised cash for both operating expenses and AI infrastructure investments. Meanwhile, liquid crypto funds broadly had a challenging start to the year, raising the likelihood of redemptions and capital outflows during Q1.

All of this was occurring while prices were not yet at levels I would consider “deep value.” In addition, many of the fiscal and monetary tailwinds that I remain optimistic about were unlikely to meaningfully impact markets until the second half of the year.

Despite this cautious backdrop, I did identify several tactical opportunities along the way. In January, I expected the potential for a short-term rally driven by beginning-of-year flows and oversold conditions. We did see a reasonable bounce, though that rally ultimately rolled over after what proved to be a false breakout.

I was once again tactically optimistic following the capitulatory price action observed on February 5th. Prices declined at a historically extreme pace during that episode, creating an attractive near-term risk-reward for a bounce. As a result, we moved some cash in our model portfolios back into risk at the time. That said, my view remained that this was a rally to rent, not own.

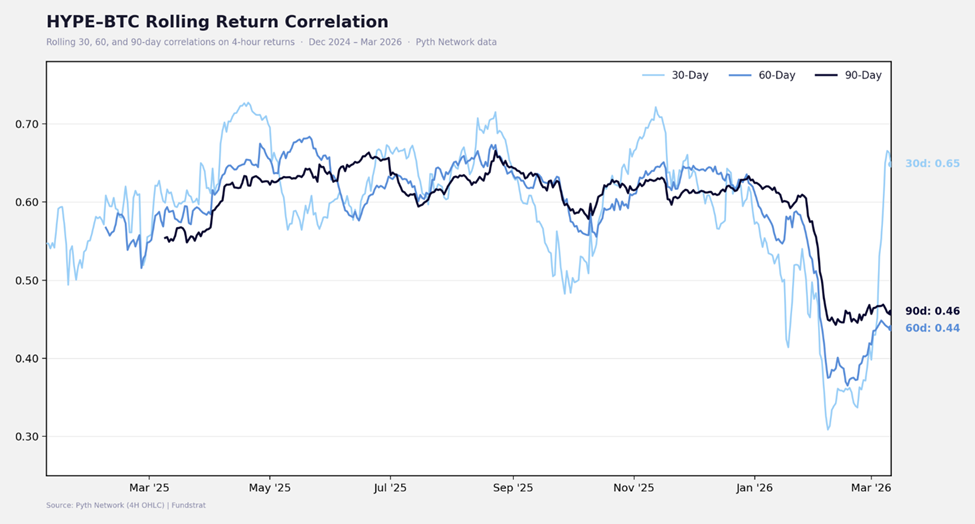

Since then, the market has largely remained range-bound. Bitcoin has oscillated between roughly $63K and $72K, while ETH and SOL have carved out similar ranges. The most notable outlier during this period has been HYPE. The project has executed effectively on its TradFi-oriented HIP-3 markets, generating revenue streams that are not purely endogenous to crypto. As a result, HYPE’s correlation to BTC has declined meaningfully over the year. The platform has also attracted mainstream attention, including coverage from Bloomberg, as traders used it to observe oil price discovery during the opening weekend of the war in Iran.

I will not spend much time revisiting the broader reasons why I remain unconvinced that the market has definitively put in its final cycle lows. Instead, I want to focus on the current setup and why recent market dynamics may be worth paying close attention to.

Zooming In: STRC Demand and Crypto Resilience

Yesterday in my Crypto Comments video, I discussed the unusual degree of resilience Bitcoin has shown despite a clear deterioration in the broader macro backdrop. Over the past several sessions we have seen equities sell off, crude oil approach $100, volatility rise, and both investment-grade and high-yield credit spreads widen meaningfully. Under normal circumstances, these developments would place significant pressure on crypto markets. Instead, Bitcoin has largely held its ground and has even shown relative strength versus traditional risk assets.

High-Yield Spreads at YTD Highs:

IG Spreads at YTD Highs:

This divergence is notable. Since Sunday, the BTC/ES ratio has risen roughly 9%, highlighting Bitcoin’s ability to hold up even as equities have struggled. Historically, Bitcoin has tended to trade closely with broader risk sentiment, particularly with high-yield credit conditions. Yet in recent sessions we have seen credit spreads widen while BTC has remained stable, suggesting that other forces may currently be supporting the market.

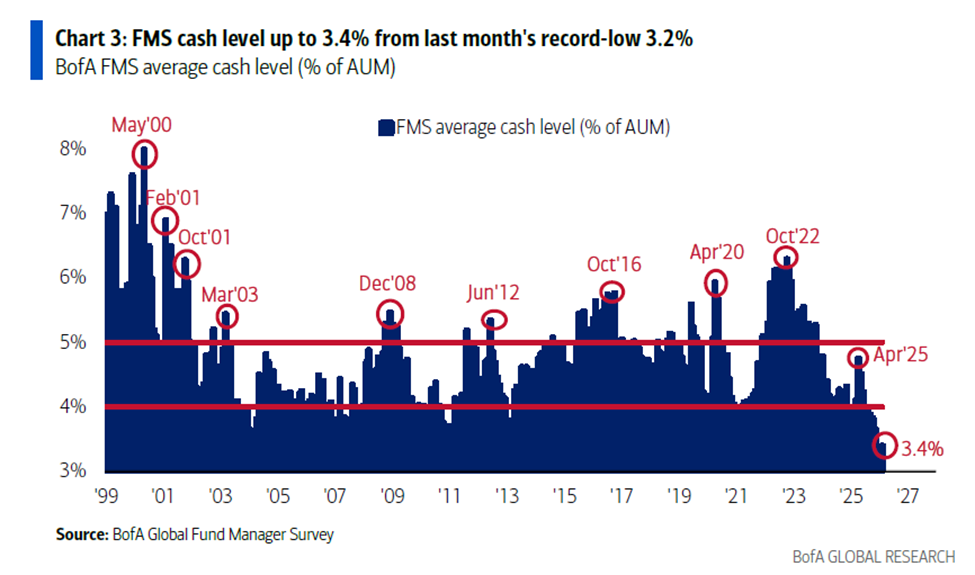

Part of the explanation may lie in positioning dynamics. It is true that investors across traditional markets have increasingly reached for downside protection, with customer put-delta exposure approaching multi-year extremes. However, the equity market is a month removed from having historically low cash allocations, per BofA’s February Fund Manager Survey. In other words, meaningful hedging and degrossing are just starting to take shape in equity markets.

Cash Allocations Were at Historical Lows:

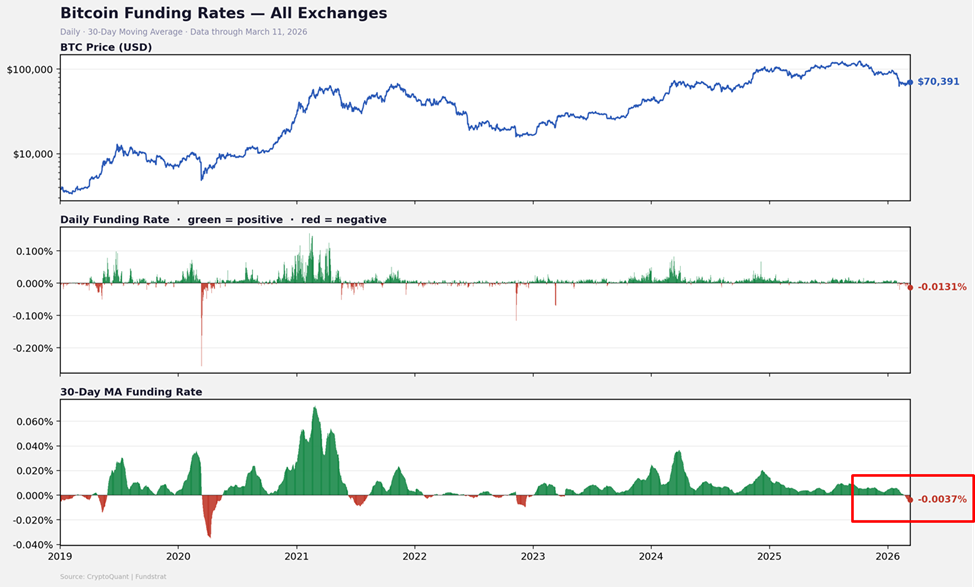

Meanwhile, we have already had multiple capitulatory events in crypto since October, with February 5th being the most recent. Sentiment is also clearly dire as evidenced by the bearish lean in derivatives markets. Put/call skew has been bearish for quite some time, and funding rates have turned persistently negative, with the 30-day average moving below zero. Historically, sustained negative funding often coincides with periods when positioning has sufficiently reset to allow markets to stabilize or move higher.

Funding Rates Persistently Negative:

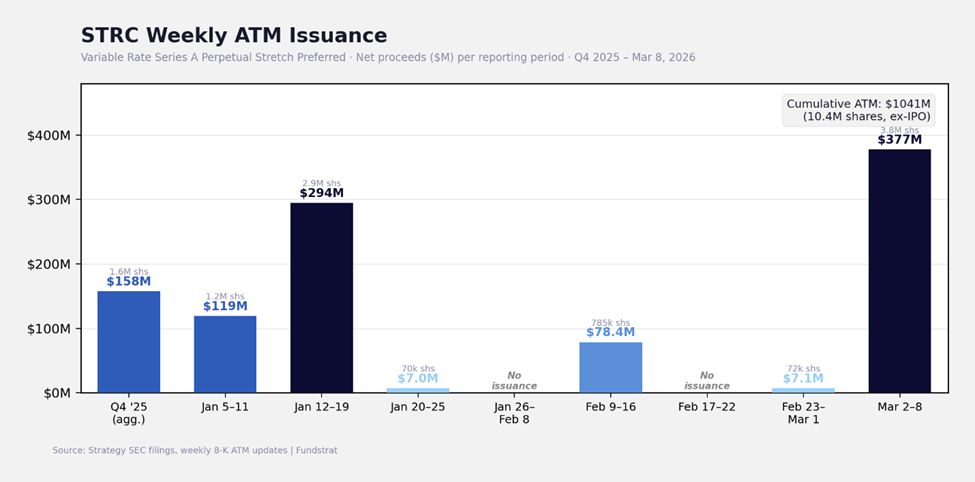

However, positioning alone may not fully explain Bitcoin’s resilience. Another important factor may be structural demand coming from corporate treasury buyers, most notably Strategy. Over the past several weeks, Strategy has once again become a consistent source of Bitcoin demand through the issuance of both common equity and, more recently, its floating-rate perpetual preferred security, STRC.

STRC is designed to trade near $100 and maintains demand by resetting its monthly dividend rate, currently 11.5%, to a level that keeps buyers engaged. When the security trades near par, Strategy is able to issue additional shares via an ATM program and deploy the proceeds directly into Bitcoin. Importantly, this preferred instrument appeals to a different investor base than the company’s common stock, effectively allowing Strategy to tap a new pool of capital.

Activity in this market appears to be accelerating. STRC trading volume reached roughly $746 million yesterday, suggesting potentially meaningful issuance through the ATM program. If even a modest portion of this volume represents primary issuance, the resulting proceeds could translate into substantial incremental Bitcoin purchases. In an environment where spot market liquidity remains relatively thin, flows of this size could have an outsized impact on near-term price dynamics.

This dynamic may help explain why Bitcoin has been able to absorb recent macro stress better than many other risk assets. In effect, the market may currently be experiencing a tug of war between deteriorating macro conditions and a growing source of structural demand.

Does Market Resilience Signal Positive Forward Returns?

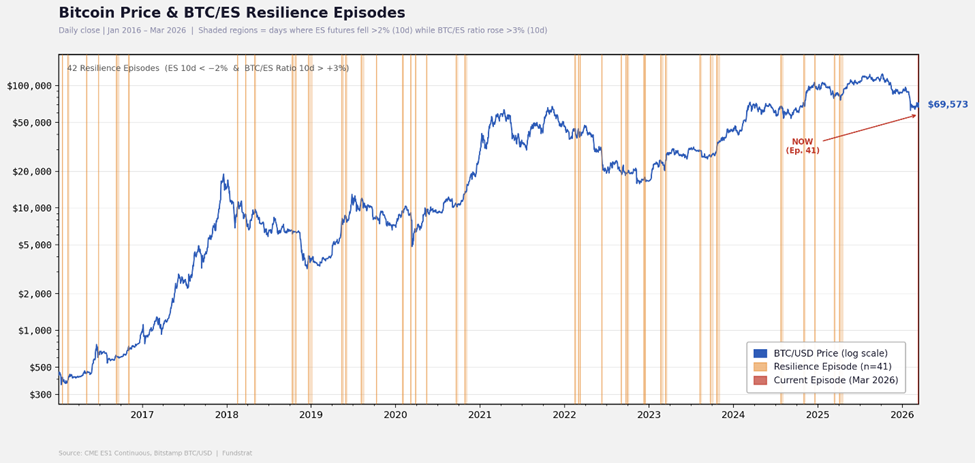

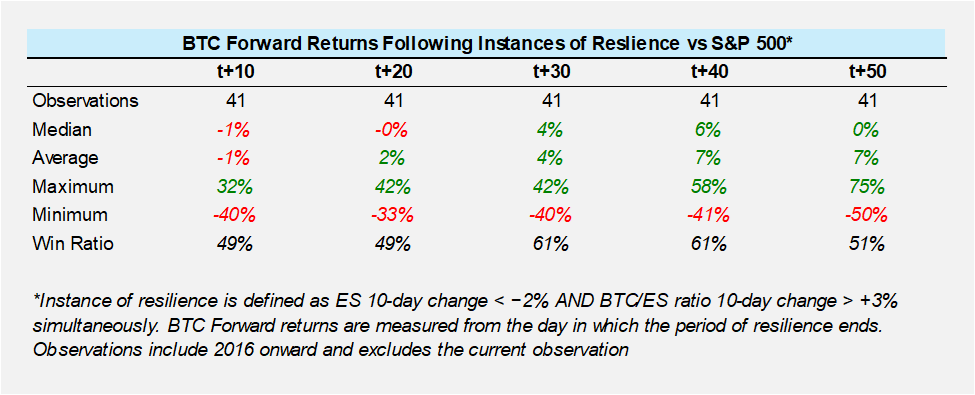

Given the unusual resilience Bitcoin has demonstrated during the recent bout of macro stress, I conducted a simple study to determine whether similar episodes in the past have tended to precede positive forward returns.

Specifically, I identified instances since 2016 where S&P 500 futures declined more than 2% over a ten-day period while the BTC/ES ratio rose more than 3% over that same timeframe. In other words, periods where traditional risk assets were under pressure, while Bitcoin demonstrated relative strength.

There have been 41 such observations over this period.

Historically, forward returns following these episodes have tended to skew somewhat positive, particularly over longer horizons such as 30 days and beyond. Intuitively, this reflects situations in which Bitcoin is able to absorb selling pressure even as broader markets weaken, often signaling that positioning has reset or that incremental demand is entering the market.

However, the signal is far from definitive. The distribution of outcomes is wide, and similar episodes have occurred in both bull and bear market environments. In several instances, Bitcoin’s resilience ultimately proved temporary as broader macro deterioration eventually pulled the asset lower alongside other risk assets.

As a result, episodes of relative strength during equity drawdowns should be viewed as a mildly constructive signal, but not a reliable indicator that a durable uptrend has begun. In the current environment, where macro risks remain elevated and financial conditions continue to tighten, this resilience is better interpreted as an encouraging data point rather than a decisive shift in the market regime.

Two Roads Diverge

Looking ahead, the forward-looking setup for risk assets appears increasingly binary.

On the constructive side, it is clear that fear has begun to get priced back into markets. Volatility has moved higher, credit spreads have widened, and investors have increasingly reached for downside protection. In crypto specifically, funding rates have turned persistently negative and positioning appears to have reset meaningfully from the crowded long conditions seen earlier in the year.

The challenge, however, is that we have not yet seen outright capitulation in equity markets. Remember that we are operating from a baseline of a fully allocated market. While risk assets have weakened and volatility has risen, positioning resets in broader markets have been relatively orderly thus far. Historically, durable lows across risk assets tend to coincide with some form of forced deleveraging or capitulatory price action in equities.

Tactically, this creates a somewhat binary near-term setup for risk assets. Given outsized implied volatility in equities and the negative skew, one could imagine that if macro conditions stabilize and risk sentiment improves (perhaps some constructive development on the geopolitical front), the positioning reset that has occurred could allow for a meaningful bounce across crypto markets. However, if the deterioration in macro conditions continues and equities ultimately move toward a capitulatory phase, it is difficult to envision crypto being spared on either an absolute or relative basis.

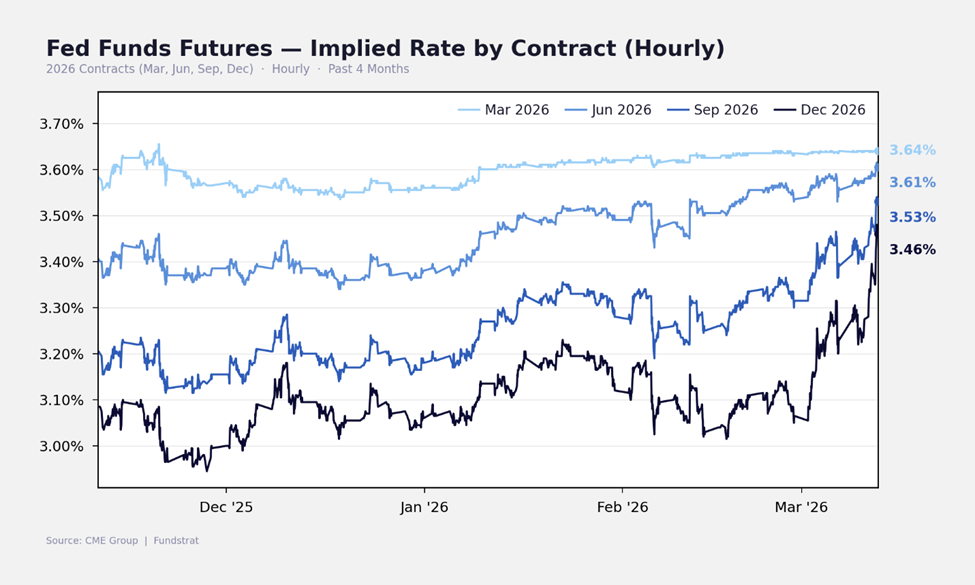

One should also consider, beyond the geopolitical risk premium that remains embedded in markets, that we have a Fed meeting and a new dot plot next week. Given developments across the commodity complex and Powell’s approaching departure, I struggle to see an overtly dovish SEP or press conference.

In that context, the resilience we are currently observing in crypto likely reflects positioning/whale dynamics rather than a full decoupling from broader risk markets, and I would expect that a decisive move for broader risk lower would see crypto play catch-up. This would mirror the dynamic we saw in June 2022 as opposed to April 2025.

Takeaway

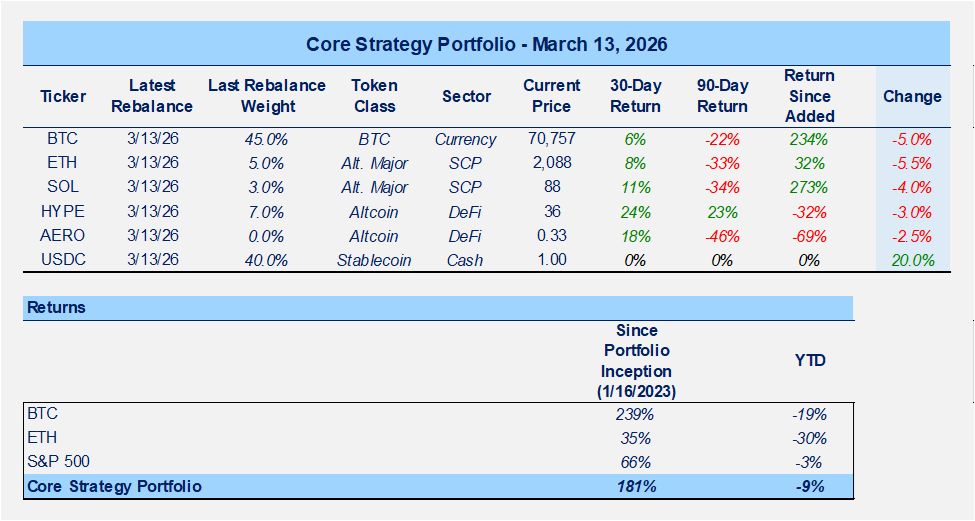

Given the shifting balance of risks, we believe it is appropriate to raise cash levels and concentrate risk exposure in higher conviction assets.

Changes being implemented:

- Increase BTC concentration within the token portfolio

- Reduce SOL allocation by approximately half

- Reduce ETH allocation by approximately half

- Reduce HYPE allocation by ~30%, though it remains overweight relative to other altcoins given its lower correlation and fundamentals tied to HIP-3 TradFi markets

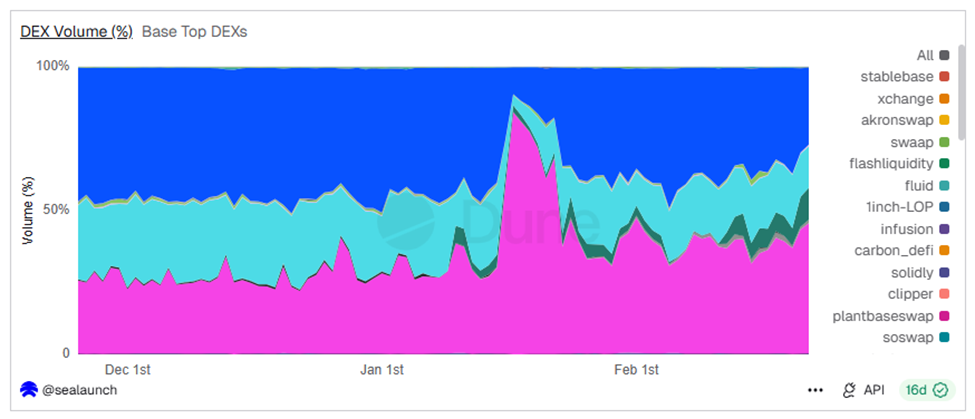

- Exit AERO due to its reflexive characteristics and declining DEX market share on Base

- Double the stablecoin allocation

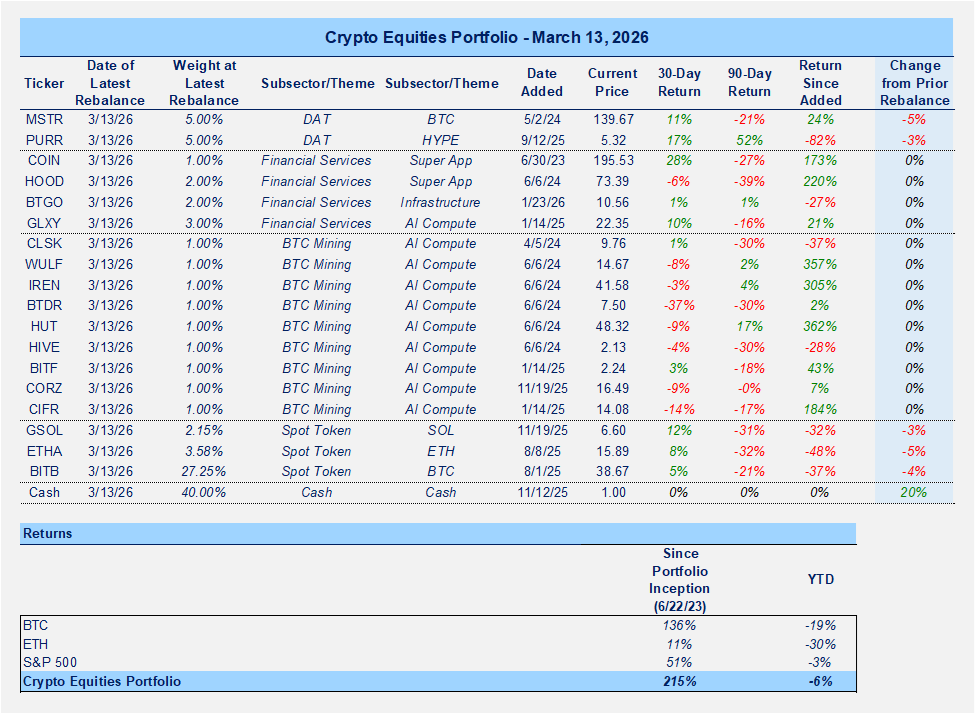

We are implementing similar adjustments within the crypto equities portfolio:

- Raise cash levels to approximately 20%

- Align token exposure weightings within the equity portfolio with the revised token portfolio allocations

- Reduce the MSTR position by half, reallocating proceeds into spot BTC exposure

AERO Market Share Declining: