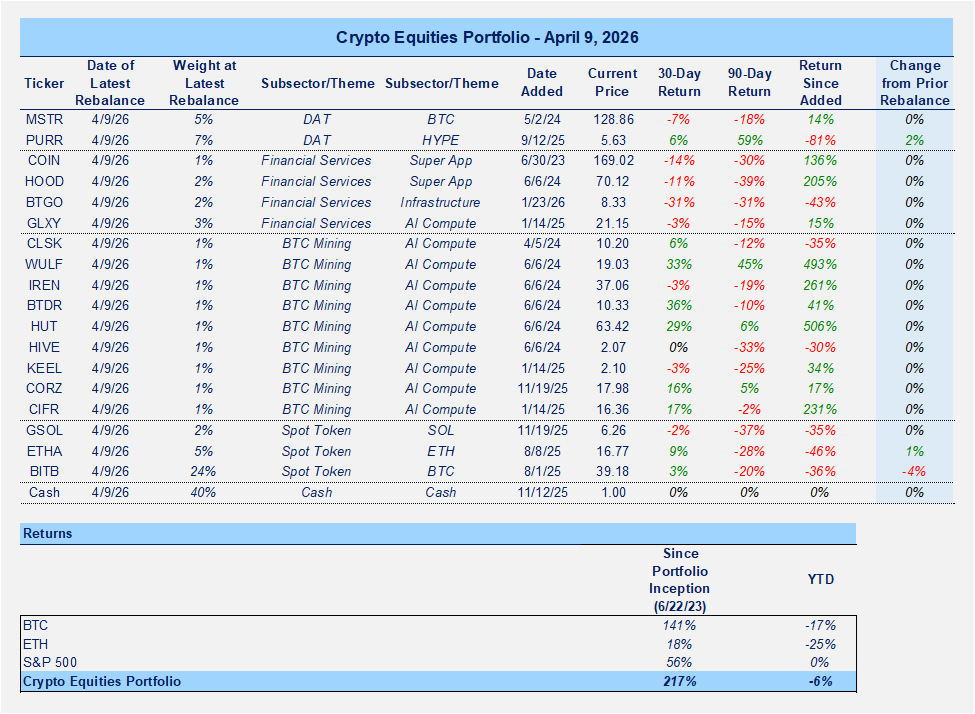

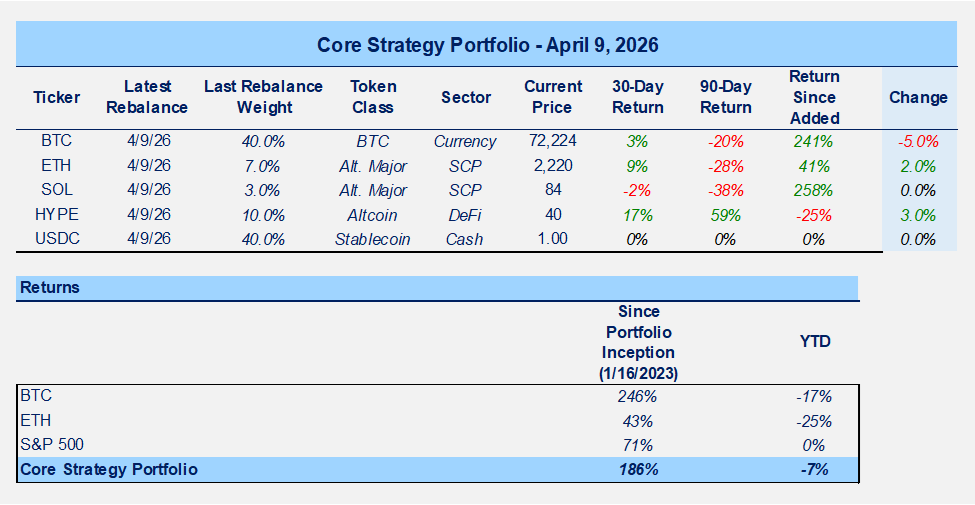

Portfolios:

Please See End of Note for Commentary on Portfolio Changes

Benefit of the Doubt

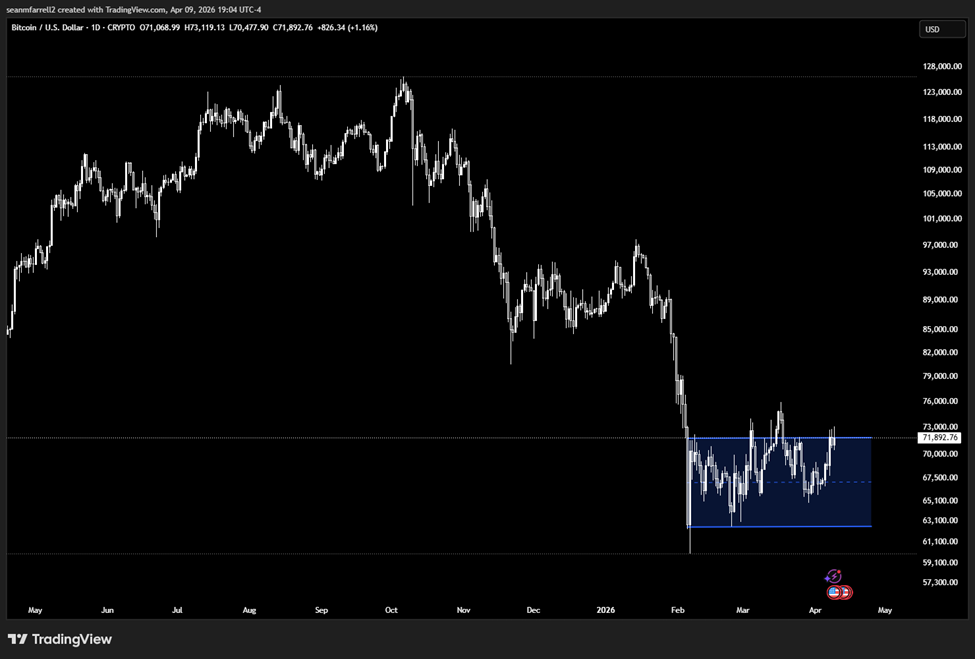

The market has found some relief since Tuesday on the back of a ceasefire agreement between the US and Iran. We have seen oil come off its highs, VIX and MOVE roll over, and spreads start to tighten. This has led to a commensurate rally in crypto, with BTC moving back to the top of the range we have been meandering in for the better part of the past two months.

HY Spreads:

Back to Top of Range:

Stepping back, I still have my concerns on the setup through Q2 and Q3. Leading indicators for near-term inflation are elevated, while a hawkish-leaning Fed remains guided by Chair Powell and a labor market that, while clearly softening, has yet to signal the type of deterioration that would warrant a policy response. This leaves us in a situation where rate expectations are likely to remain elevated for at least the next couple of months, while the balance sheet continues to expand at a modest rate. At the same time, intermediate-term trends in bond market volatility appear to be moving higher. In other words, the liquidity picture remains mixed through at least the first half of the year.

The liquidity backdrop is only one of the reasons I remain hesitant to call this the start of a new bull market. That said, today I want to zoom in and discuss why I think the odds of continuation higher, say toward ~$80k for BTC, have increased.

Benefit of the Doubt on Geopolitical Risk

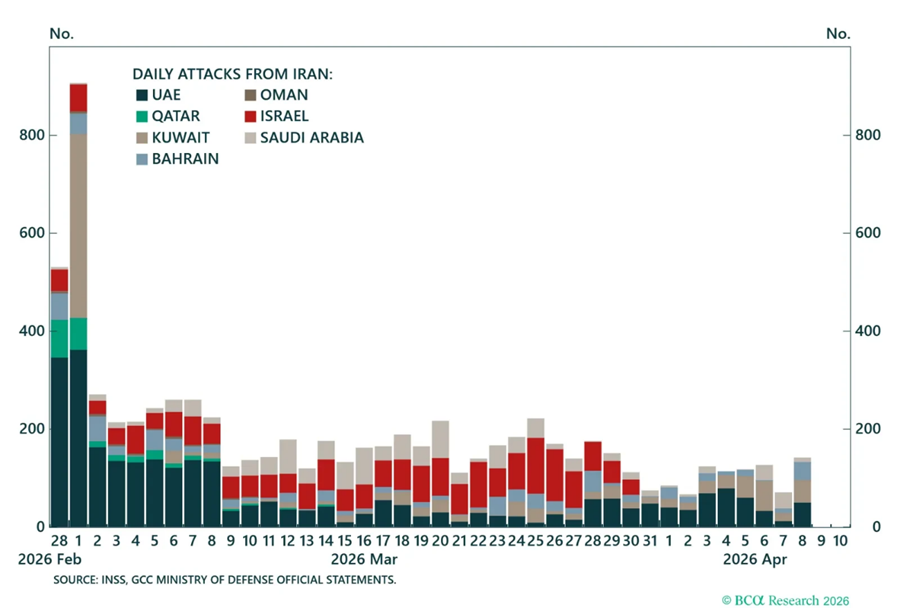

Despite both sides ostensibly agreeing to a ceasefire on Tuesday, there have been a number of headlines suggesting that is not fully the case. Reports of continued bombings (with some data to support this, see below), rhetoric from Iran suggesting disagreement over whether Israel’s conflict with Lebanon falls within the scope of the ceasefire, and indications that ship traffic through the Strait of Hormuz remains limited all point to an unresolved situation. Despite this, the market has largely shrugged off these developments, suggesting that it is optimistic about a path toward de-escalation in the coming days.

Bombings Continue (Data through 4/8):

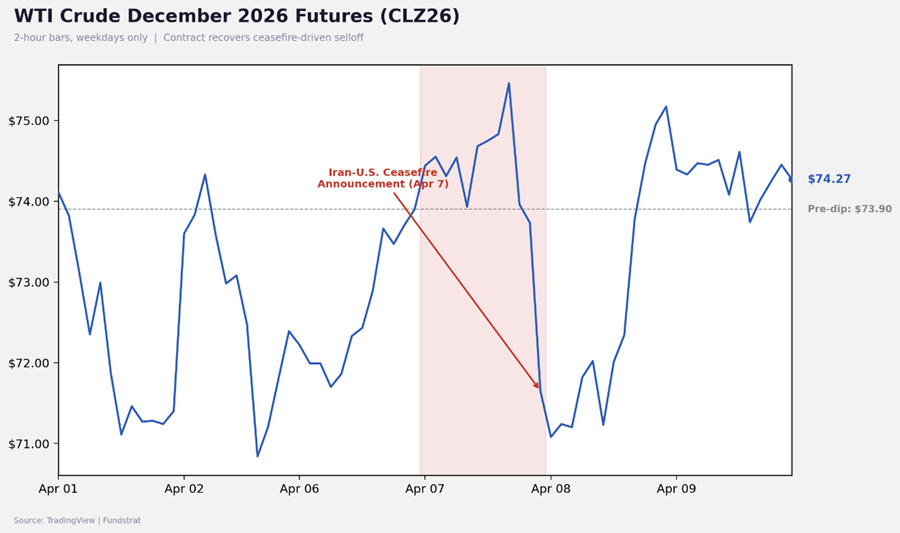

I will admit that crude and Brent futures, particularly in longer-dated contracts, continue to reflect some degree of disruption risk. That said, oil is highly sensitive to near-term supply and demand dynamics, while risk assets are more forward-looking. This helps explain why equities showed resilience ahead of the ceasefire announcement. The bottom line is that while strong price action in the face of bad news does not preclude a drawdown, it is generally a constructive signal for forward returns.

Not Much Relief in Crude Futures Post-Ceasefire:

Progress on War Could Allow Markets to Look Through Inflation Data

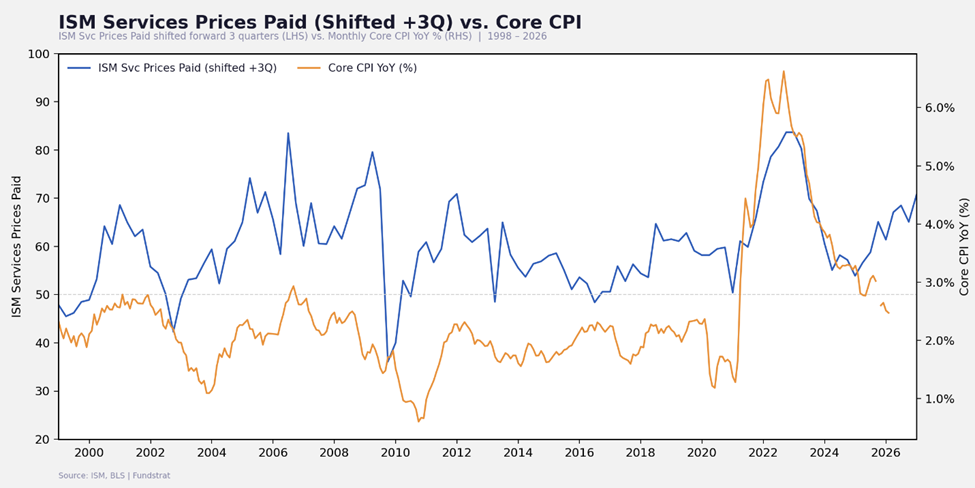

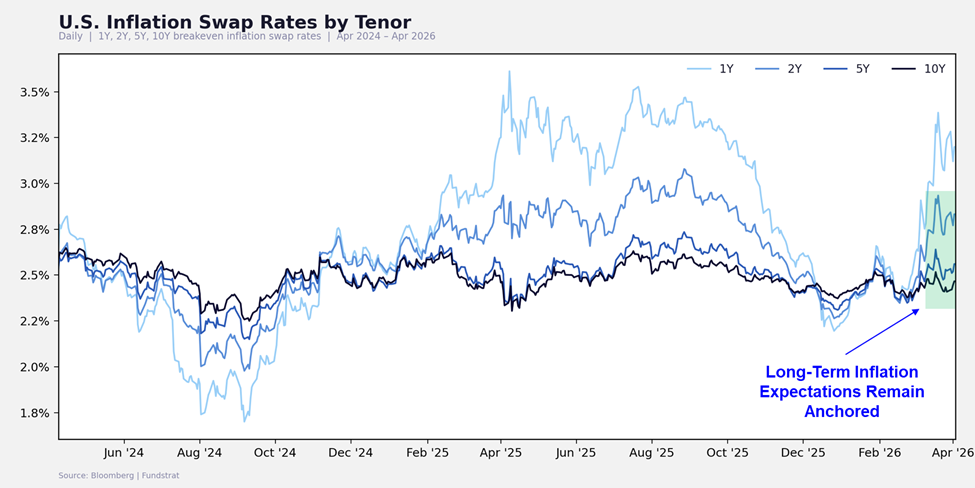

As noted above, leading indicators for inflation are moving higher (see ISM services prices paid vs core CPI below), and both the market and the Fed expect some increase in inflation this year, and potentially next, due to the war. However, both the market, via swaps, and the Fed, via recent commentary, appear to agree that any war-driven inflation is likely to be transitory.

ISM Services Prices Paid vs Core CPI:

Inflation Swaps Reflect Transitory Effects:

Over the medium term, this remains a headwind as it delays the Fed’s reaction function. However, focusing on this week, where CPI is a key event, I suspect the same optimism that is supporting risk assets in the face of geopolitical risk could also allow the market to look through a potentially strong print. This will be the first CPI release that reflects the effects of the war in Iran, and expectations are already skewed toward an uptick. Combining expectations for a firm print, optimism around a resolution to the war, and commodities steady, but off their highs, the setup suggests that, barring a material upside surprise, markets can look through the data.

Positioning Has Unwound to Some Extent

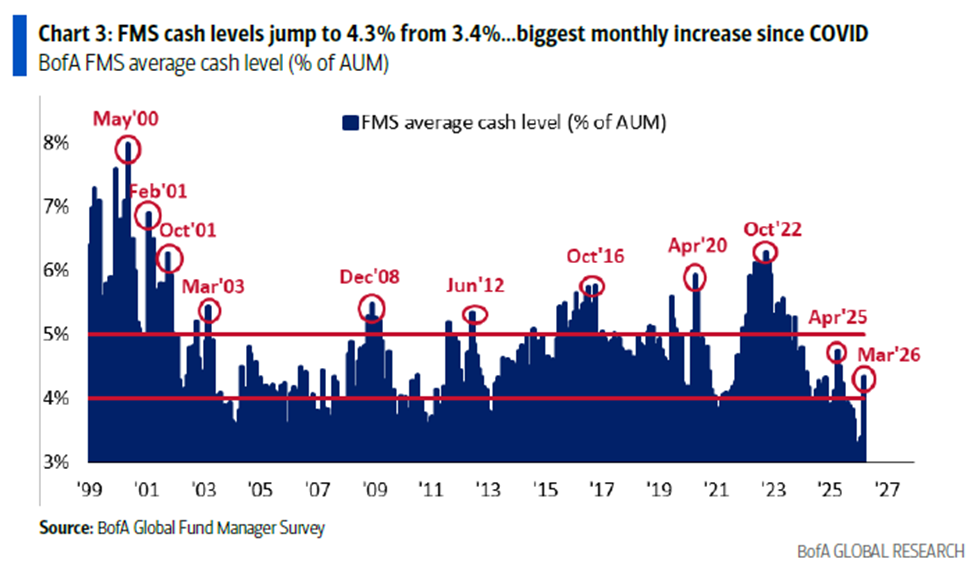

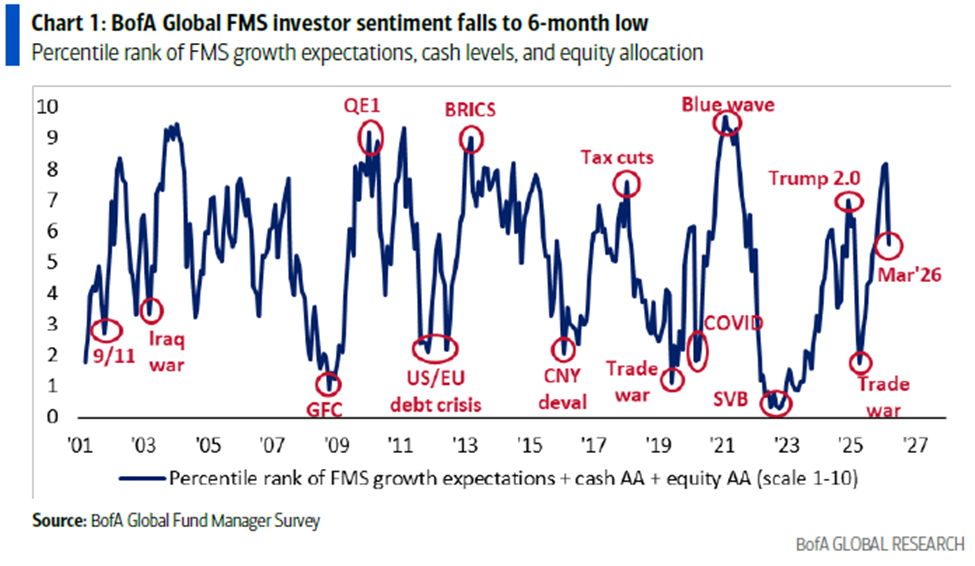

I spoke about this in a Comments video last week, but over the past month it does appear that we have seen some degree of de-grossing. According to the BofA fund manager survey, cash levels rose from 3.4% to 4.3% from February to March, the largest monthly increase since COVID. Their measure of investor sentiment also fell to a six-month low. While this does not provide a strong contrarian bullish signal, it does remove positioning/sentiment from my list of key downside risks.

BofA FMS on Positioning:

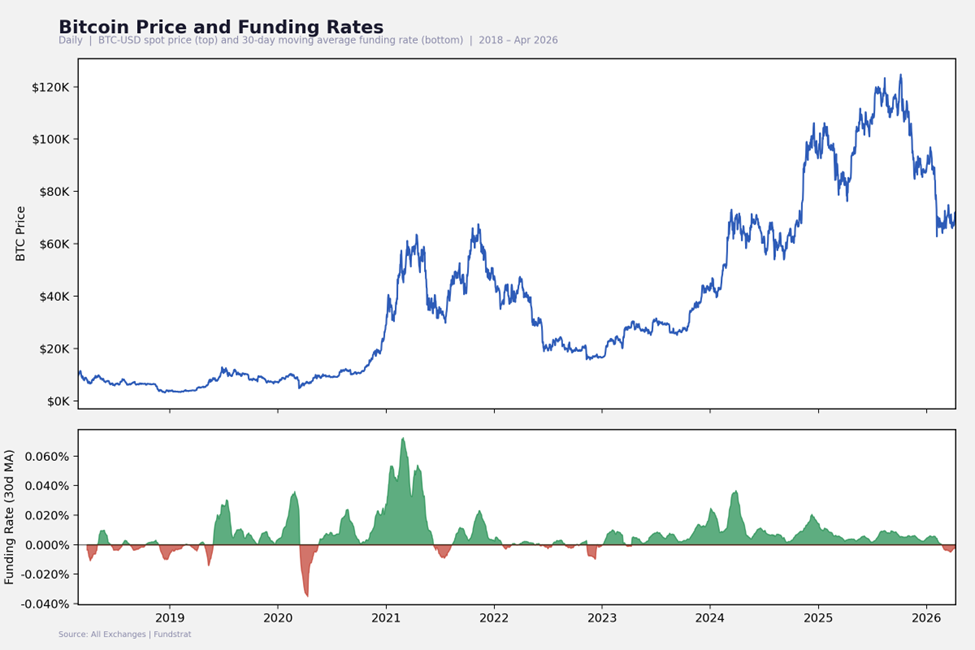

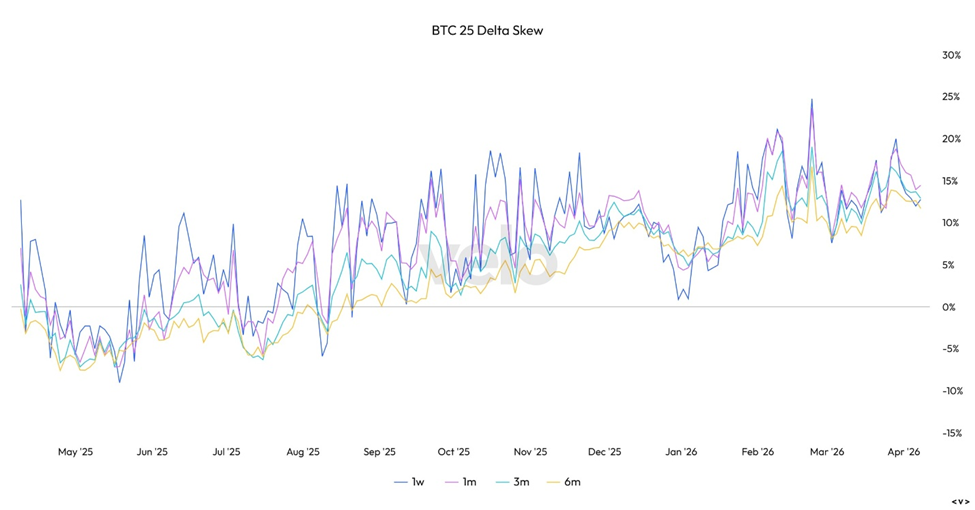

Looking specifically at crypto, positioning also appears relatively defensive. 30-day average funding rates remain in negative territory, and options skew suggests that puts remain rich relative to calls across all tenors. This indicates that the market is not overly extended on this recent bout of resilience and retains room to move higher when viewed through this lens.

Defensive BTC Positioning:

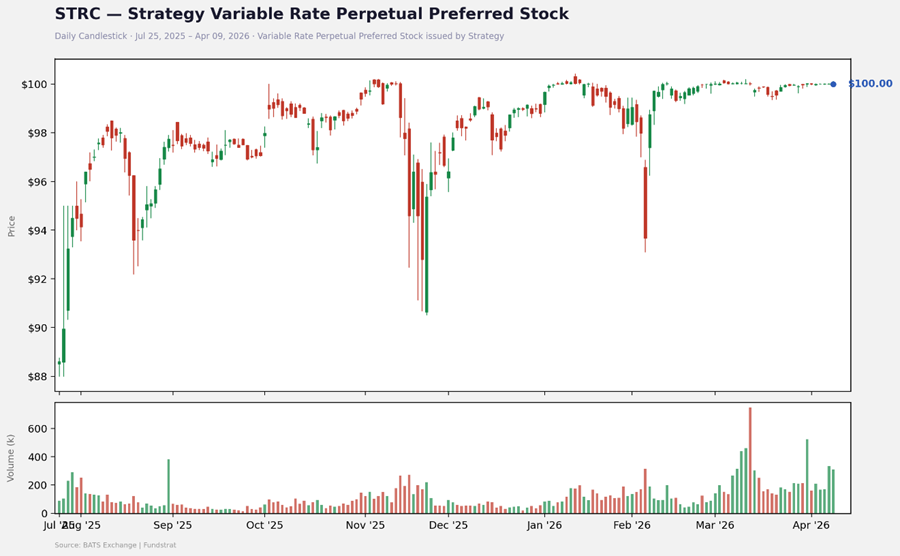

STRC Likely to be an Incremental Buyer Through Next Week

While the market has been largely bereft of inflows over the past six months, one bright spot has been the traction of Strategy’s STRC perpetual preferred stock. STRC pays a variable yield (currently 11.5%) and is designed to trade near par. When it drifts below par, MSTR may increase the stated yield, and when it is at or above par, it can issue additional STRC via its ATM program.

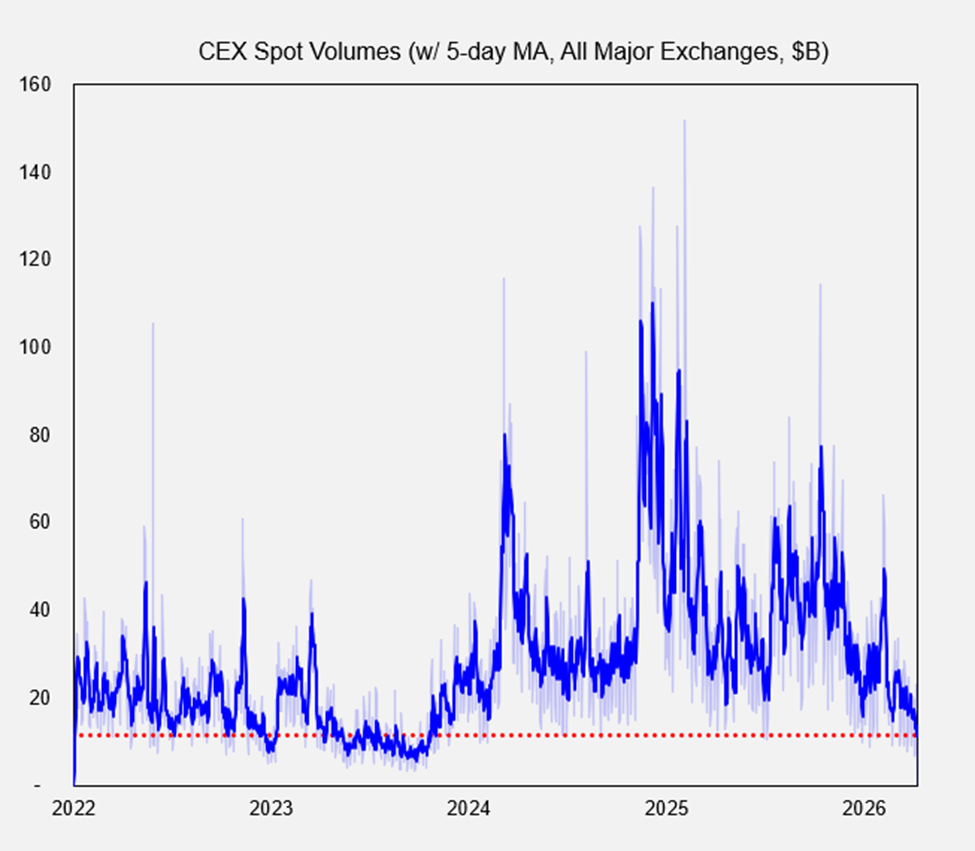

STRC has been trading around par for the past week, and volumes have increased accordingly. If this persists into next week, issuance could accelerate ahead of the upcoming ex-dividend date on 4/15. A fair question is how much impact an incremental $500 million to $1 billion in BTC flows could have. While it depends on broader market activity, it is worth noting that overall crypto volumes remain cyclically low, meaning incremental demand from large participants can have an outsized impact.

I do acknowledge that miners continue to sell their trove of BTC to fund AI capex, creating an opposing whale-driven flow. While it is difficult to quantify the balance precisely, I am optimistic that STRC-driven demand can outweigh this pressure in the near term.

STRC Volumes Increasing:

Dearth of Spot Volumes:

Room for Financial Conditions to Ease

As discussed above, I believe the primary risks are a re-escalation of tensions in the Middle East and a materially strong CPI print (well beyond market expectations). However, given the current balance of factors, I think there is a reasonable case that markets can look through these risks in the near term. If so, there is room for financial conditions to continue easing as the geopolitical risk premium rolls off.

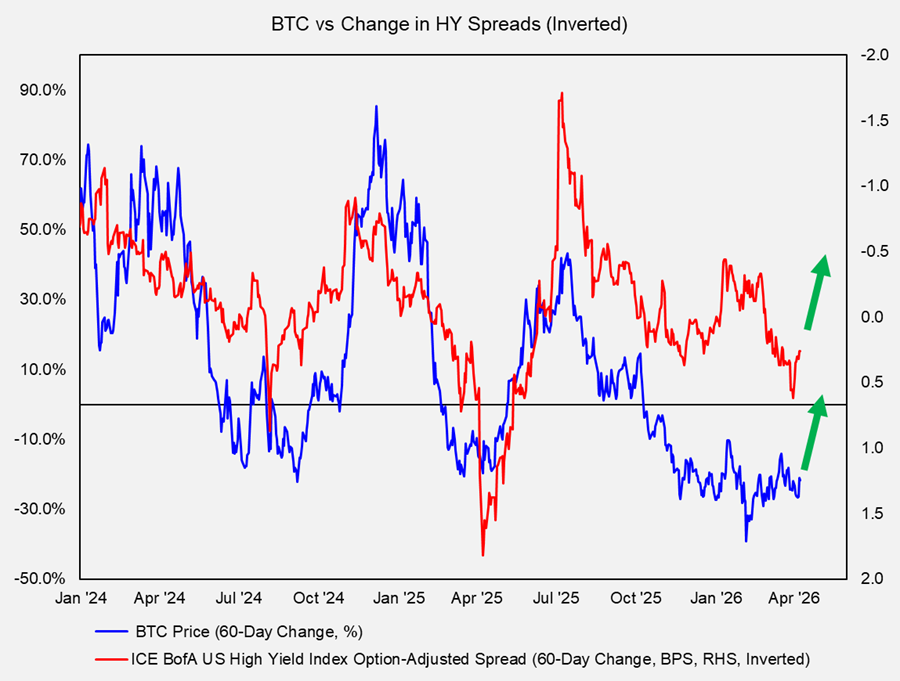

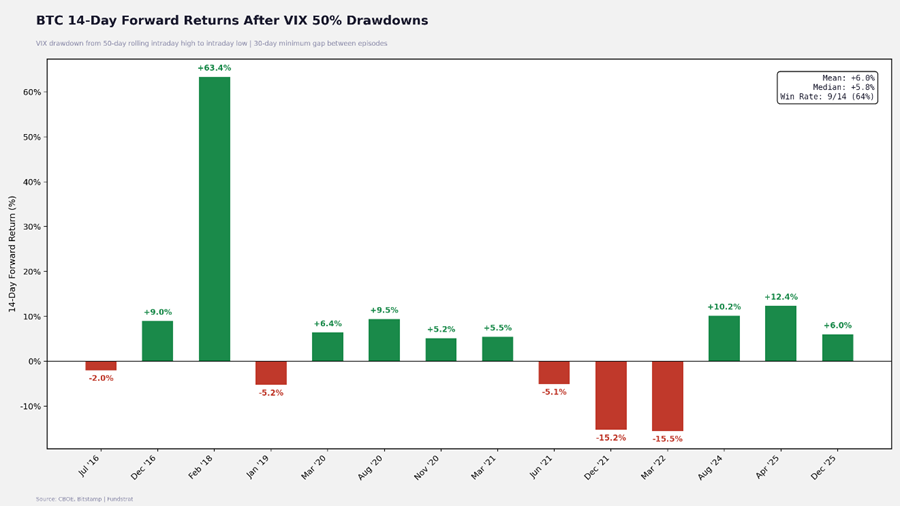

VIX, MOVE, and high-yield spreads have all come off their highs and could continue to move in a constructive direction. The impact of tightening spreads is already showing up in BTC price action. Notably, the VIX has declined ~50% from its intraday high on 3/9.

Historically, similar declines have been associated with strong forward returns for BTC, with a median two-week return of 5.8% and a win rate of 64%. The counterpoint here would be that most prior instances of negative returns have occurred during bear markets, which we arguably are currently in.

HY Spreads vs BTC:

VIX Decreases vs BTC:

The Takeaway

All in all, my base case remains that this is a bear market rally for crypto. This view is largely driven by the mixed liquidity backdrop, a lack of clear catalysts, and the potential for positioning to become a concern again.

That said, near-term conditions have improved and I view the odds of a break of ~$72k resistance as favorable. As a result, I am rotating modestly further out along the risk curve while keeping overall exposure largely unchanged. This reflects a balanced stance. If the market breaks higher, as I expect, we should see higher beta assets outperform on a relative basis. If conditions deteriorate, I retain flexibility to reduce risk and redeploy at more attractive levels.

Portfolio Changes:

- BTC (-5%): I am reducing our BTC allocation by 5%, rotating capital further out along the risk curve.

- SOL (Maintain at 3%): I am maintaining our 3% allocation to SOL.

- ETH (+2%): I am adding 2% to ETH. ETHBTC is testing a medium-term downtrend resistance, and a breakout in BTC above the upper end of its range around ~$72k would likely drive a similar break in ETHBTC.

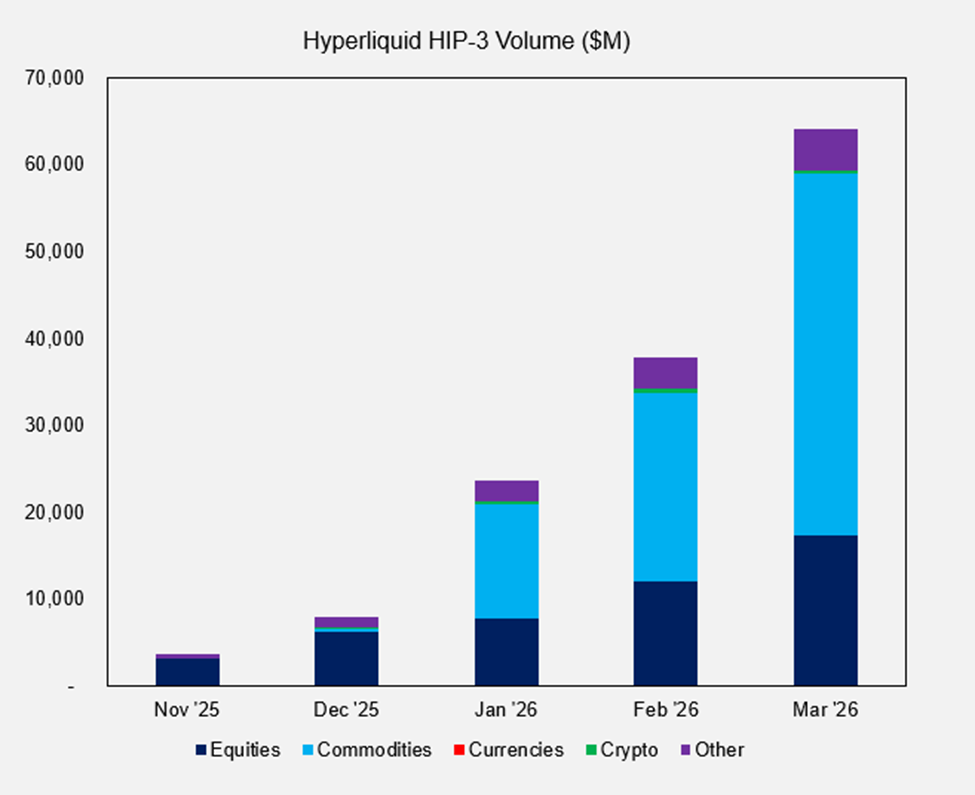

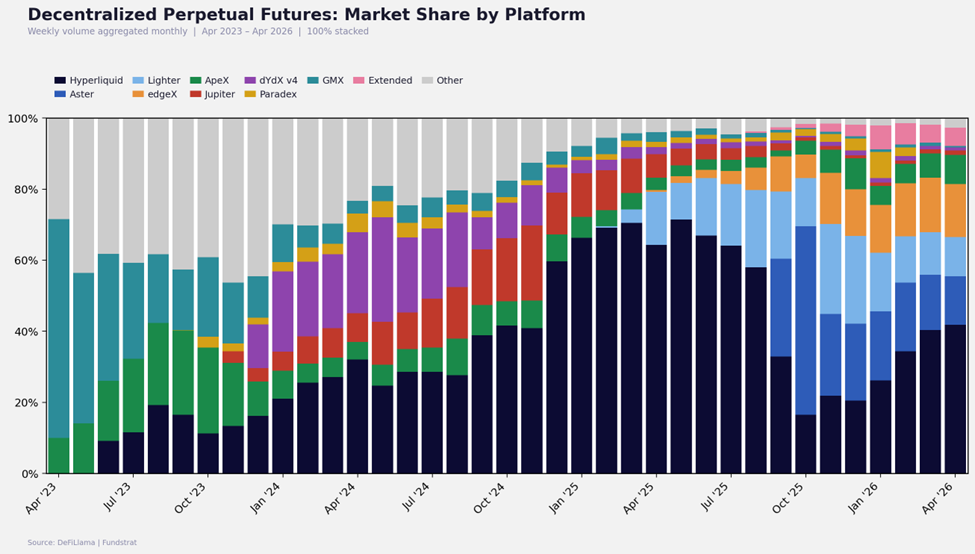

- HYPE (+3%): I am increasing our HYPE allocation by 3%. The token continues to exhibit outsized strength, up ~70% YTD and ~50% since the onset of the war. HIP-3 markets generated over $60 billion in volume in March, largely driven by trading of TradFi-linked assets.

- Equities Portfolio: Making commensurate changes to spot token exposure to remain consistent with the token portfolio.

ETHBTC At Resistance:

Hyperliquid’s Perps DEX Dominance:

$64B in HIP-3 Volumes in March: