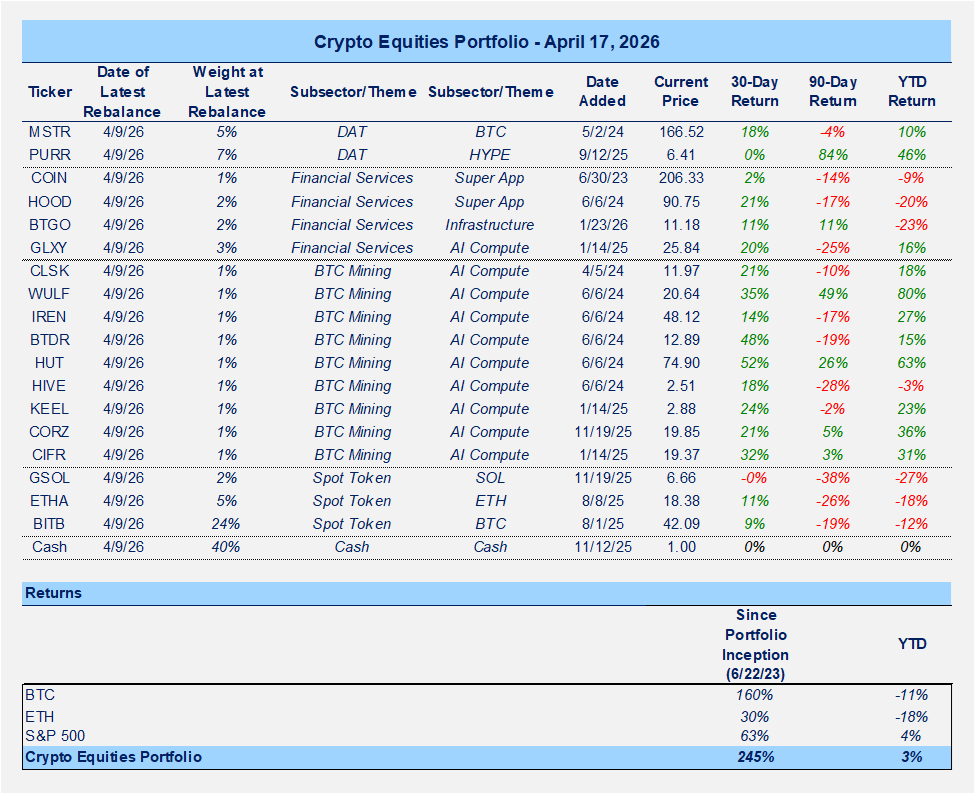

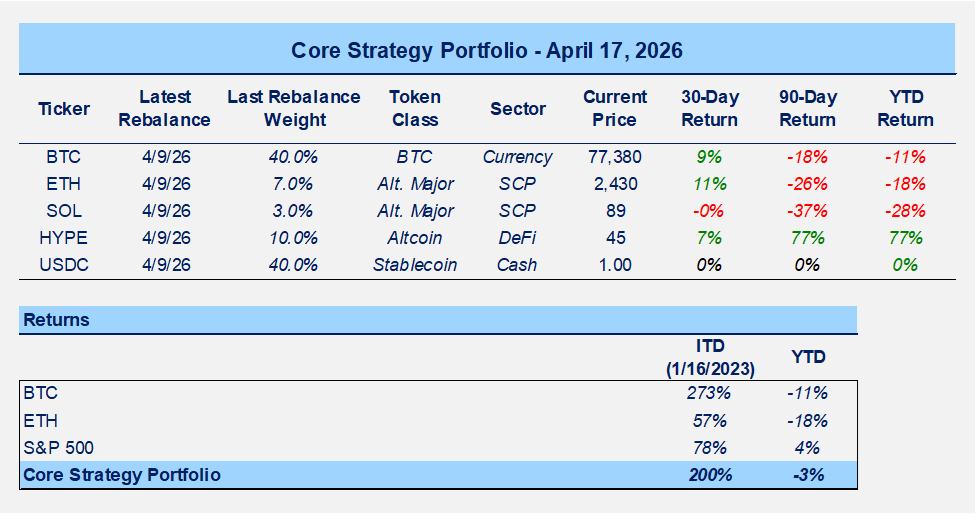

Portfolios

Getting Up to Speed

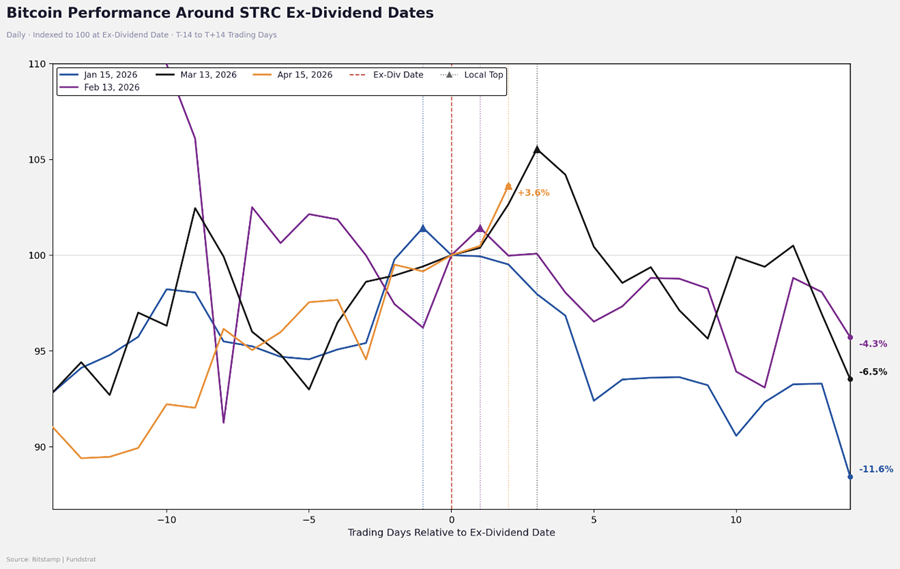

- In last week’s note, I discussed some of the reasons that I favored the continuation of this bear market rally. Among those were the anticipated roll-off of the geopolitical risk premium that had been weighing on crypto, positioning in traditional markets that were less saturated in risk, positioning metrics in crypto that suggested traders were outright defensive, and the anticipated flows from MSTR over the coming days as Saylor was likely to issue as much STRC as possible into the market ahead of the ex-dividend date on 4/15.

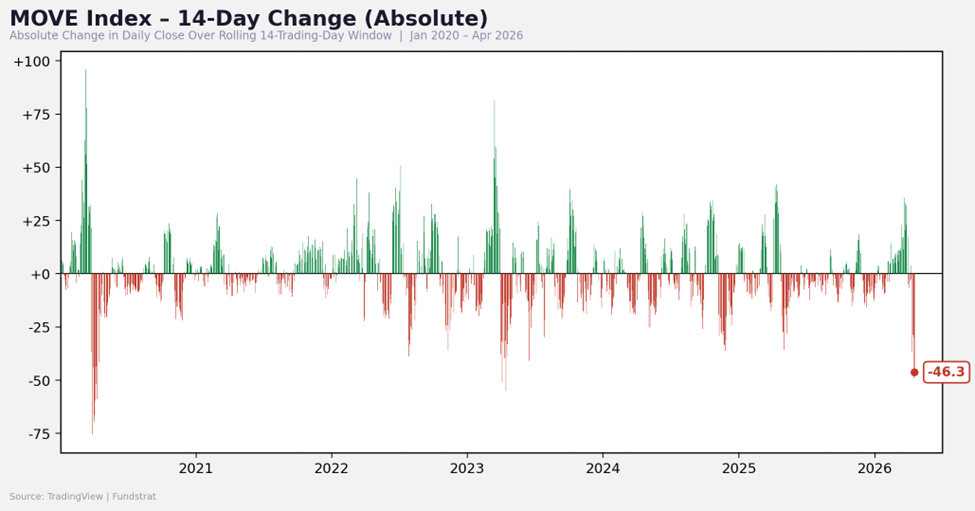

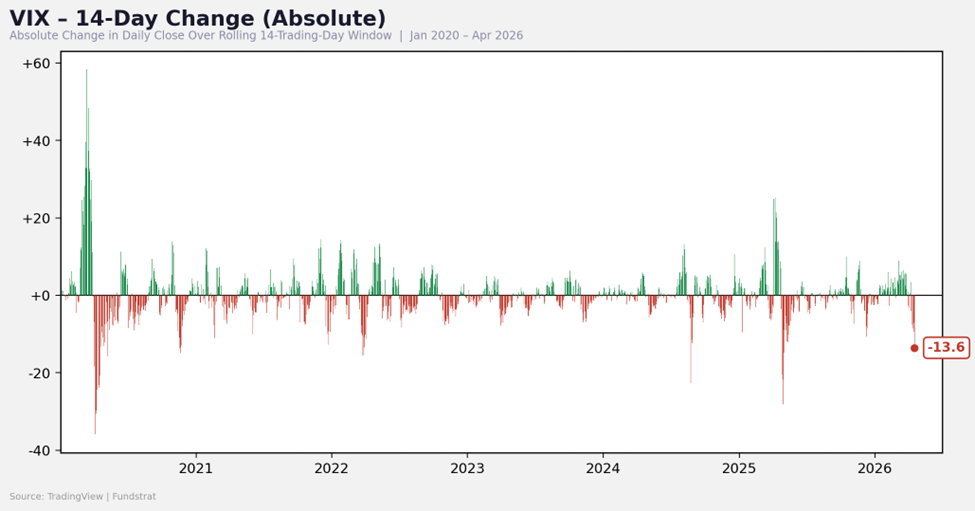

- This largely came to fruition. The VIX drew down to ~17 from an intraday high of over 35 just a month ago, crude rolled over, the MOVE index rolled over, and credit spreads came back in. We saw broader risk continue higher, with the crypto complex following suit. Based on volumes of $1.1 billion and $1.5 billion on Monday and Tuesday, respectively, I suspect that STRC likely raised more than $2 billion to purchase BTC this week. When paired with a rising Coinbase premium throughout the early half of the week, it is clear that MSTR has been making its impact felt in the order books.

- Around mid-week, I admittedly grew a bit skeptical of being able to reach the ~$80k round number target I had in mind after considerable underperformance on Tuesday, but it seems that Saylor’s dry powder lasted through the week, and there is a bit of a lockout rally occurring in equities, which helps crypto’s cause.

- Now, with MSTR having completed, or nearly completed, its buys, it is worth stepping back and thinking more about the near/medium-term setup. Is this a bear market rally? Or should we chase here?

The Backdrop

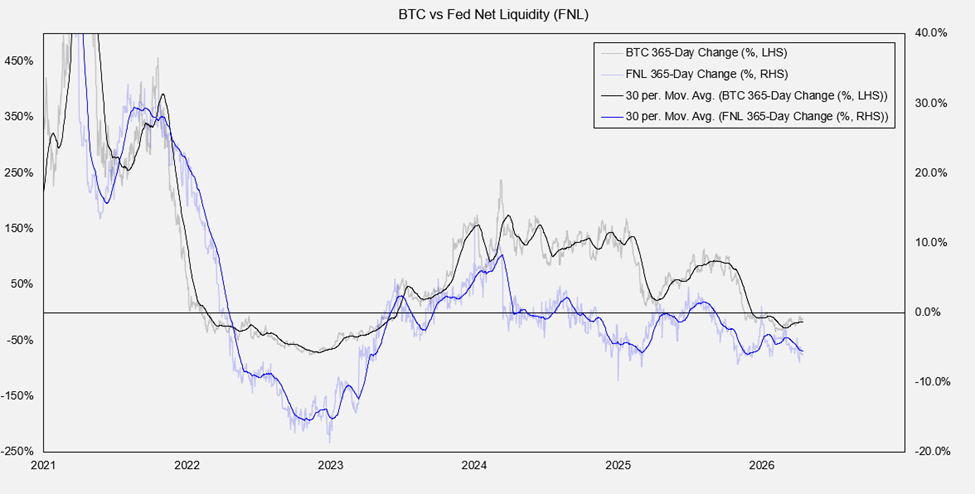

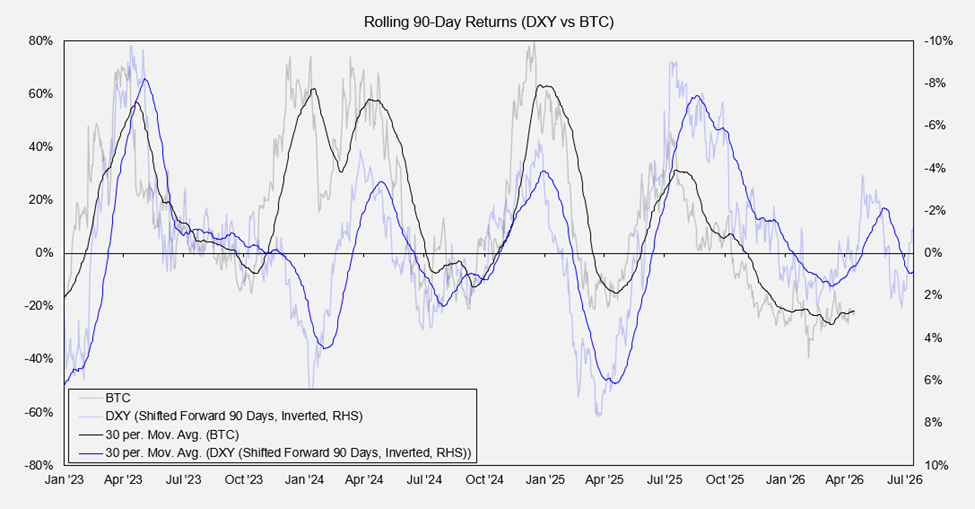

Liquidity: Liquidity is the lifeblood of crypto. As I mentioned last week, not much has changed on the liquidity front. Liquidity trends are neutral to negative on a year-over-year basis, with only modest balance sheet expansion and interest rates unlikely to be cut over the next several meetings as the Federal Reserve waits for the data to confirm that war-driven inflation was, in fact, transitory. The DXY also remains somewhat rangebound. It is therefore difficult to view liquidity trends as being overly favorable for crypto over the short/medium-term.

Risk Appetite: Another pillar of crypto success is risk appetite (measured by VIX, MOVE, which also influences liquidity conditions, and spreads). Both high-yield and investment-grade spreads have moved lower quite strongly over the past couple of weeks, in line with the geopolitical risk premium rolling off. We’ve also seen historical moves lower in both the VIX and the MOVE index, so we’re certainly seeing risk appetite re-enter broader markets and trending higher.

MOVE & VIX Plummet:

Spreads Tighten:

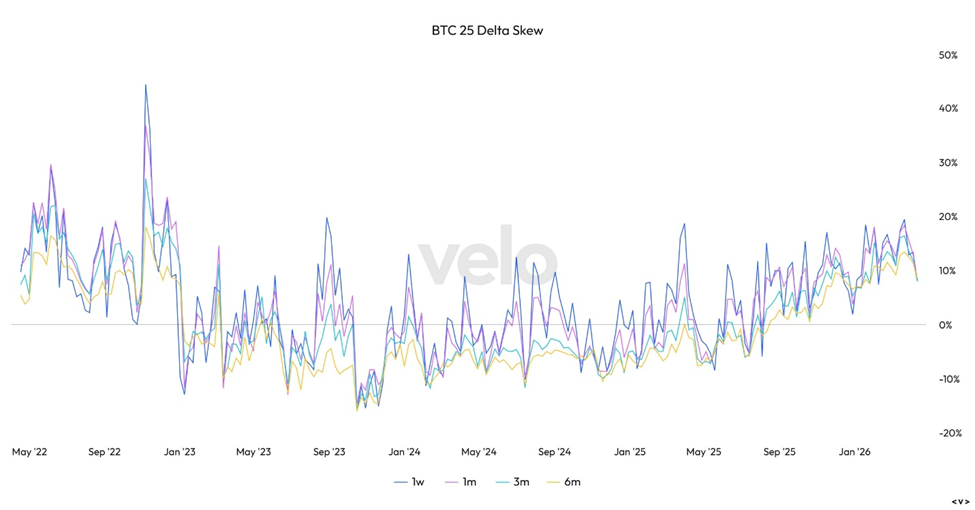

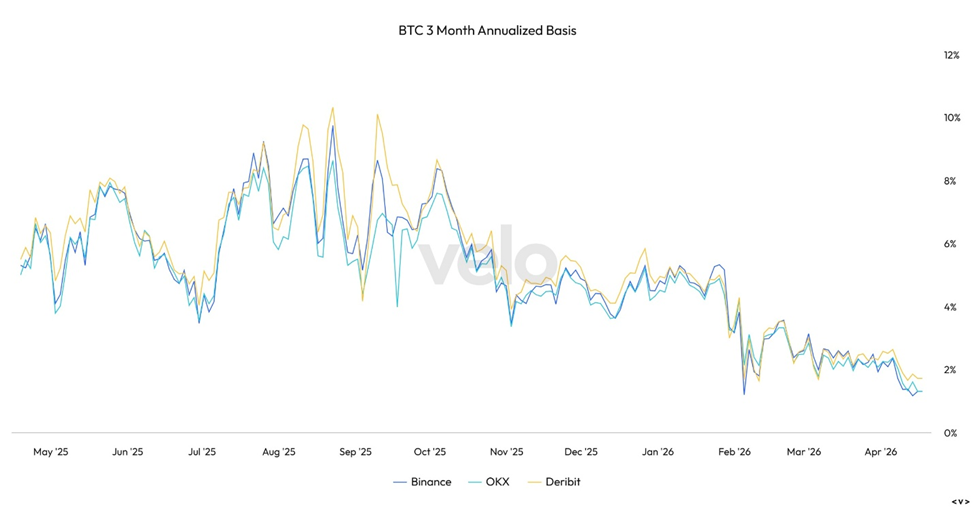

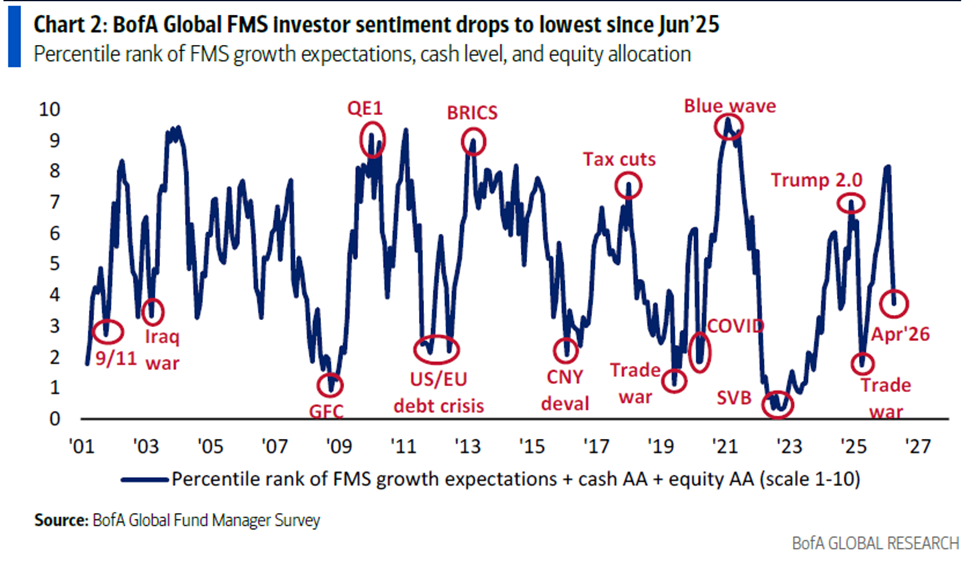

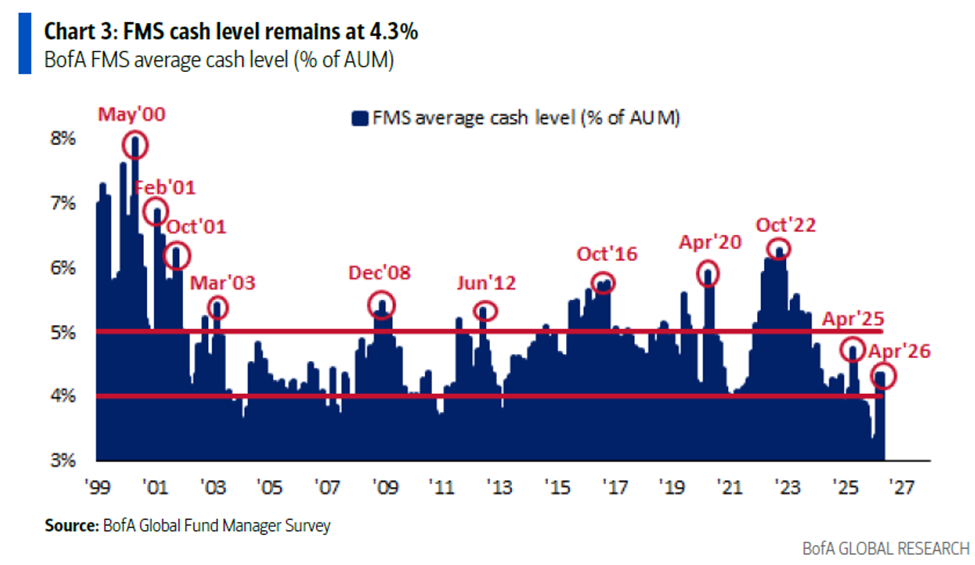

Positioning: Positioning is still not a major concern in crypto markets. Funding rates remain tame, the three-month basis continues to trend lower, and options skew still reflects defensive positioning. Positioning in traditional markets is also less of a concern than it was at the start of the year, although that is likely changing with each fifty basis point move higher in the major indices. The latest Bank of America Fund Manager Survey shows that cash levels in March remained above their cyclical lows achieved earlier in the year, while investor sentiment declined again. I suspect that much of the recent equity market strength reflects a quick re-grossing following the early April lows.

Funding Rates Negative:

Puts Remains Rich Relative to Calls:

Basis Trending Lower:

Sentiment Drops:

Cash Levels:

Flows: As discussed, MSTR has been focused on selling STRC preferred stock to raise capital over the past few months. This is a variable-rate perpetual preferred security designed to trade around par. When STRC trades below par, MSTR can increase the dividend to attract buyers, and when it trades above par, it can issue new STRC via its at-the-market program. One should expect issuance ahead of the ex-dividend date as traders position to collect the current 11.5% yield. As demonstrated over the past few months, there has been a reliable pattern of constructive price action into, and sometimes slightly after, the ex-dividend date, with Bitcoin often rolling over afterward.

Based on volumes this week, it is likely that Saylor raised more than $2 billion in capital to deploy into Bitcoin. There was likely some degree of front-running in addition to the price-insensitive buying from MSTR over the past week. That suggests the potential (with a possible exception, which I will describe below) for an air pocket next week as this source of demand is removed.

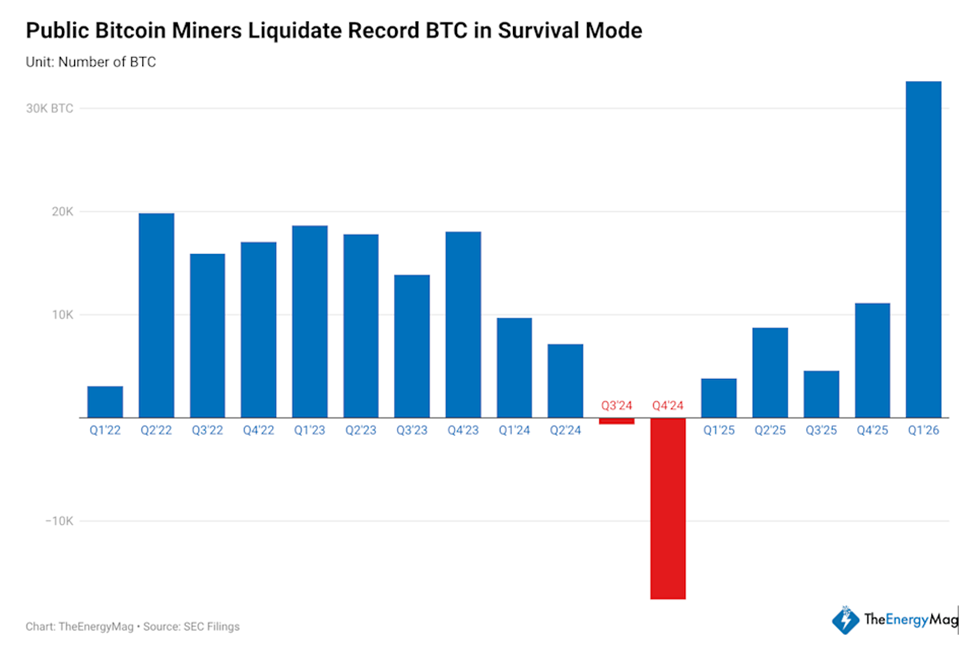

On the supply side, miners have been significant marginal sellers of Bitcoin year to date. This is being driven by declining mining profitability as well as the need to raise capital to pivot capacity toward artificial intelligence and high-performance computing. There is more opacity in this part of the market, which makes it difficult to gauge forward-looking sell pressure, but my view is that this trend is not yet complete.

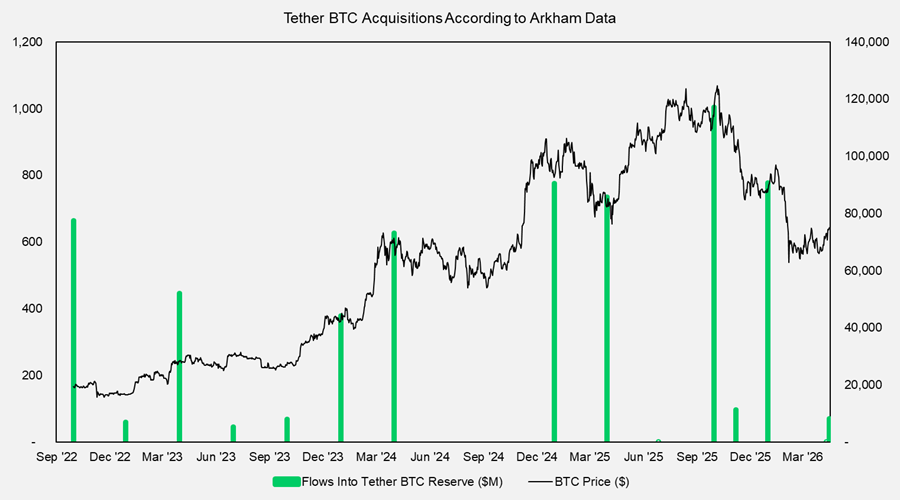

On the positive side, we have seen Tether re-enter the market for the first time in a while. Over the past year, they have allocated a considerable portion of their earnings into physical gold and appeared to have deprioritized Bitcoin. According to Arkham data, Tether received Bitcoin into its reserve address for the first time since December, totaling approximately $70 million. This is small relative to the scale of their purchases during stronger phases of the bull market, but if it marks the beginning of a new trend, it is a constructive development for the crypto complex.

STRC Performance Around Ex-Dividend Dates:

Tether Bidding Again:

Miners Have Sold So Much BTC (Do They Have More?):

TLDR: In summary, liquidity conditions are neutral to negative, risk appetite has resurfaced and is trending higher, positioning is defensive in crypto and has improved in tradfi since the start of the year. Demand-side flows are improving on the margin as STRC finds increased demand and Tether re-enters the market, but there remains the question of the air pocket in flows left between ex-dividend dates.

What Now?

Assuming one agrees with the assessment above, that the fundamental picture for crypto is mixed, but positioning and risk appetite are generally suitable for crypto outperformance, then it becomes appropriate to look for idiosyncratic drivers that could spur flows into crypto. During the bull market, we had two prominent examples in the ETF launches and the election.

Looking ahead, one identifiable potential catalyst is the passage of the Clarity Act, which should provide some confidence in the altcoin complex. I suspect that we could see marginal flows into some of the service providers in the crypto space as investors begin to speculate on increased business activity. These are companies that offer services around trading, custody, and tokenization. We may also see some marginal flows into ETH, SOL, and HYPE. But we have already seen agencies take steps toward crafting rules of the road for crypto without legislative progress, and we have not seen a response from asset prices as a direct result. Further, based on recent developments, or lack thereof, it is still difficult to underwrite passage of this act as a certainty, given competing priorities on Capitol Hill.

Could the MSTR Flywheel Force Us Back Into a Bull Market?

In thinking about other idiosyncratic ways that the market could transition into a more sustained trending environment, it is worth revisiting STRC and unpacking an interesting evolution in the demand landscape for this security.

- On-chain Demand Emerging: Tokenization remains a major theme in crypto and is often framed as a way to improve the efficiency of traditional financial infrastructure. One emerging application is centered around STRC. There are now protocols working to tokenize STRC, package it into on-chain products, and allow decentralized finance users to apply leverage in order to enhance the current 11.5% yield.

- Two protocols worth mentioning are Saturn Credit and Apyx Finance. Apyx Finance has gained the most traction so far, so it is worth focusing on that example.

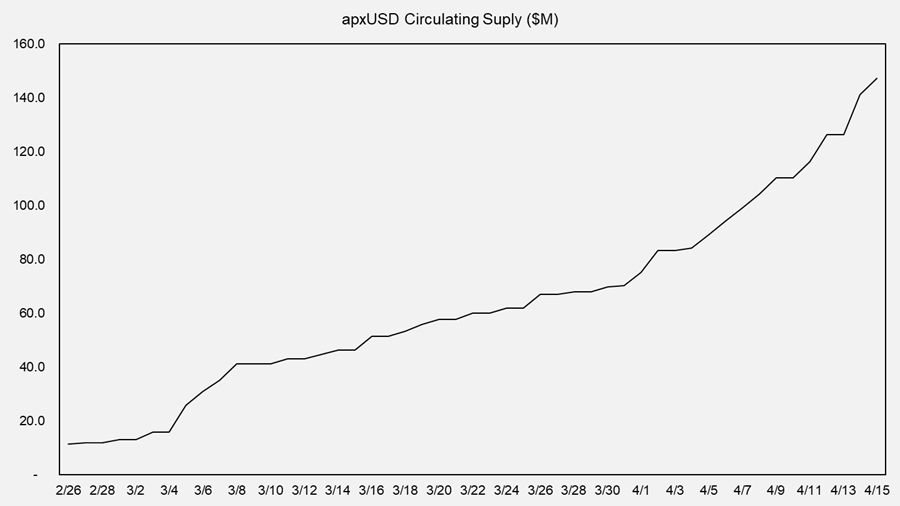

- Apyx is a stablecoin protocol built around what it calls Digital Credit. It issues apxUSD, a synthetic dollar overcollateralized by variable-rate perpetual preferred stock from digital asset treasuries such as Strategy’s STRC, and apyUSD, a savings token that passes through dividend income from those preferred shares as on-chain yield. The underlying thesis is that preferred equity dividends represent a more scalable and transparent source of yield than basis trades or funding rates, which tend to compress as capital flows increase.

- We have already seen some early traction, with total stablecoin market capitalization approaching $150 million. It is worth noting that the term “stablecoin” may be somewhat misleading from a risk management perspective, as this is fundamentally an on-chain credit product. Users should be aware of risks related to dividend stability, off-chain custody of collateral, principal risk, and potential redemption dynamics. This is not meant as an endorsement or a rejection of the product, but rather to highlight that there is now a growing source of on-chain demand for STRC. Users can access the product, apply leverage to enhance yield, and potentially use it as collateral within decentralized finance.

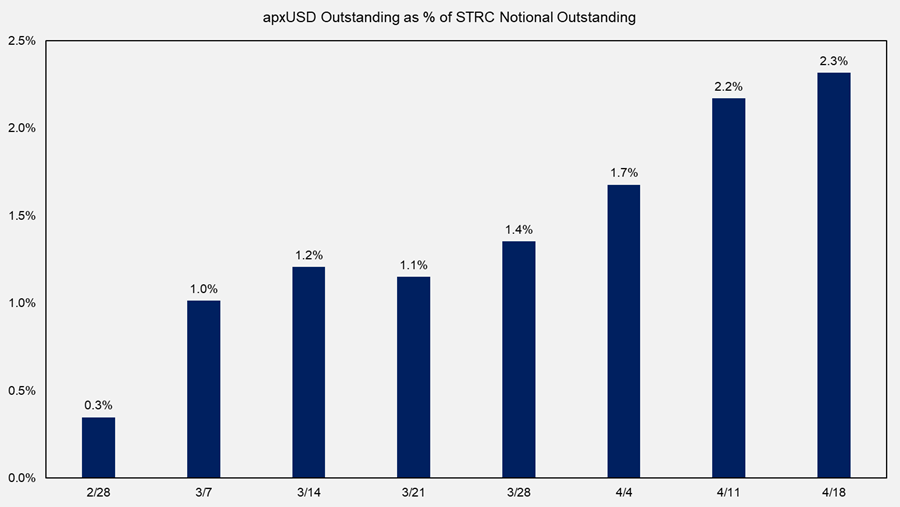

- Based on the latest available data, apxUSD supply represents just over 2% of STRC notional outstanding. It is still a relatively small portion of the overall investor base, but it is growing and could contribute to a flywheel effect if adoption continues to build.

apxUSD Demand Climbing:

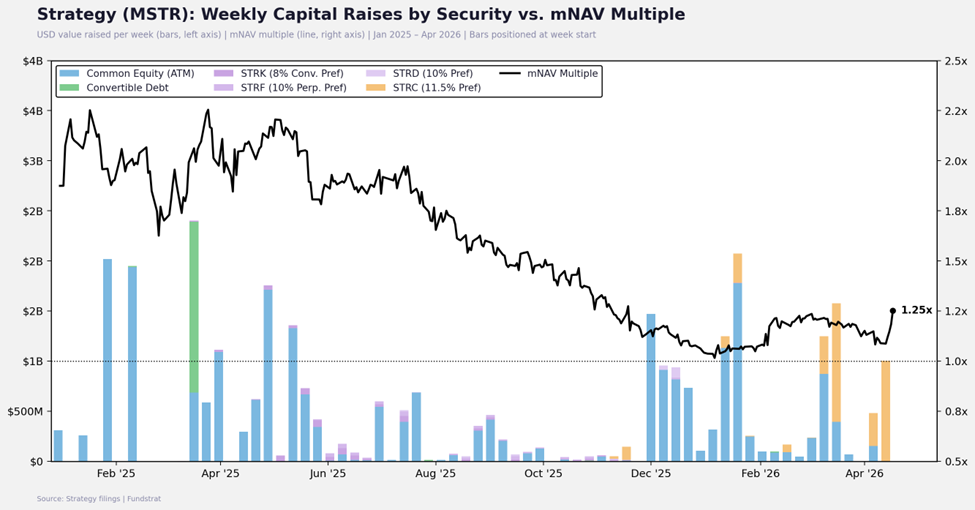

- Common ATM as a Bridge or STRC Strengthener? Another tool at MSTR’s disposal, which it has avoided using as much of late, given the focus on adding leverage to its capital stack, is common stock. This is historically the preferred capital-raising method for the company, but in recent months, MSTR has steered clear of selling new common shares. As mentioned, this is due to the renewed focus on adding leverage to its capital stack, but also due to its multiple of NAV being compressed relative to historical levels.

- However, on Friday, we saw price action in MSTR that certainly suggests some element of a squeeze, with the stock having traded nearly 17% higher intraday. As of 3 pm ET, the stock had recorded over $7 billion in volume, the highest since the 2/5 capitulation day. This also pushed MSTR’s mNAV multiple up to 1.25x. It is likely that this mNAV multiple expansion allowed MSTR to tap into their common ATM, as this is a spread to NAV that might be difficult to ignore.

- There are a couple of ways to interpret the impact of this on near-term price action: (1) it could mean that MSTR will have additional funds to purchase BTC and at least partially “bridge” the market to the next STRC ex-div date, or (2) it is possible that MSTR uses the opportunity to raise cash for its USD reserve(the funds set aside for payment of future dividends). If the former, it could perpetuate the MSTR/BTC flywheel near-term and provide some more juice into next week. If the latter, this will certainly make STRC an increasingly intriguing product for investors ahead of the next couple of ex-dividend dates. In either case, it is structurally bullish for the MSTR/BTC flywheel over longer timeframes. If raising cash for the USD reserve, it still means there is likely a demand-side air pocket ahead.

- One other important element to consider, an element that was just announced to the public, is MSTR’s desire to shift STRC to bimonthly ex-dividend dates. This would smooth out the capital-raising cadence from STRC and allow for a more constant bid from MSTR. This was just proposed, and shareholders will not vote on it until the June meeting, and thus it is not going to have an immediate impact on the market, but it is worth keeping in mind.

MSTR Capital Raises & mNAV:

TLDR: There is a world in which MSTR’s common ATM serves as a partial bridge to the next ex-div date. That said, I skew towards thinking that the company uses common ATM proceeds from any common stock sales to bolster its USD reserves. Regardless, the larger point here is that STRC demand, both on-chain and via traditional venues, might be the idiosyncratic spark that moves us into a trending environment and is the leading candidate for invalidating my view that this is a bear market rally.

Some Thoughts on Miners

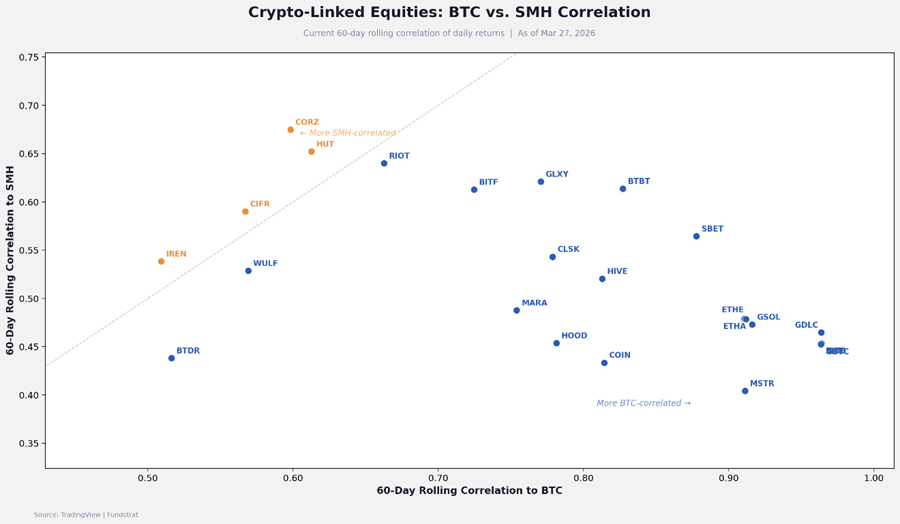

It seems clear, based on the resurgence in the tech sector since the market bottomed, that AI is leading this recovery. We have seen strong performance once again out of Mag 7, semis, and memory names. I do not find it a coincidence that the market turnaround coincided with Anthropic’s tease of their Mythos model back on 4/7. It makes sense that the best performers in our crypto equities portfolio have been the miners, as they largely consist of companies that are either diversifying or fully pivoting to servicing AI compute. In fact, many of these names now correlate more strongly with semiconductor performance (other capex receivers) than BTC. Thus, I think it is right to lean into these on any dips in the coming weeks.

Miner Correlations to SMH:

Final Takeaway

Given the broader liquidity landscape and the potential demand-side air pocket for BTC that could emerge next week (and uncertain demand beyond that), I think it’s right to still view this as a bear market rally. Recall that we had BTC bear market rallies of ~48% and ~43% last cycle, so that is why I still like maintaining flexibility (cash) in the model portfolios while finding other ways to outperform (this week the miners & HYPE did a lot of the heavy lifting). In testing the “bear market rally” view, I find that the most reasonable case for this being the start of a new bull market is the potential for an MSTR-driven flywheel to take shape.