The S&P 500 rose 1.07% last week, while the Nasdaq climbed 1.51%. There seems to be little question that most impactful development this week came from the Supreme Court, which overturned the tariffs imposed by President Trump under the International Emergency Economic Powers Act on April 2, 2025. By a 6-3 vote, the Supreme Court ruled on Friday that the IEEPA does not give the U.S. president the ability to impose tariffs. The decision most directly affects tariffs Trump sought to impose on what he called “Liberation Day,” but a number of other tariffs imposed last year are unaffected by the ruling.

For now, the decision arguably removes a sentiment overhang – a cloud of skeptical, nervous, or negative emotion that keeps investors cautious and on the sidelines. In this respect, “this is a risk-clearing event,” Fundstrat Head of Research Tom Lee suggested shortly after the decision.

Hours after the decision was released, the president announced plans to impose a global 10% on all imports (later revised to 15%), regardless of country-of-origin, using authority granted by Section 122. This statute empowers the president to unilaterally impose a baseline tariff on all countries for up to 150 days, after which Congressional approval would be needed. Still, Lee suggested that because the removal of elevated tariffs (at least temporarily) could have a disinflationary effect, it could also push the Federal Reserve in a dovish direction. Thus, the decision “is positive for stocks, in our view,” Lee told us.

Due to the possibility of market uncertainty as investors await clarity on the White House’s long-term response, Lee noted that tech, software, and crypto “suddenly look more interesting, because they are not caught up in the tariff messiness.”

The crux of the SCOTUS ruling is that Congress must authorize tariffs. Our Washington Policy Strategist Tom Block told us that in his view, any regular Congressional approach to authorizing the tariffs would almost certainly end up filibustered by Senate Democrats, unless the tariffs can be framed as a budgetary issue. If so, the “Reconciliation” budget process would enable them to be passed on a simple majority vote and without the possibility of filibuster. Block also pointed out the importance of paying attention to farm-state Republicans, whose constituents have been hurt by retaliatory actions taken by countries targeted by the tariffs.

Looking at the rest of the week’s market activity, Head of Technical Strategy Mark Newton acknowledged that these days, “market overall feels extraordinarily volatile, given the software, crypto damage, along with the recent decline in the Magnificent Seven.” Yet, in his view, “it really has not been.”

“This has been a bull market,” he reminded us during our weekly huddle, “but it’s just been important to be in materials and energy, of course, and industrials and not just be in technology, where everybody is still overweighted.” He reiterated “I see a lot of great parts in the market. It’s just not tech.” In fact, he noted, “breadth is still sloping higher,” citing the advance-decline ratio in the Russell 3000. Breakdowns in this metric preceded the April 2025 decline, as well as the late 2021 decline. Thus, in Newton’s view, “if we start to see evidence of this breaking, then that’ll be a bigger concern for the equity market.”

Chart of the Week

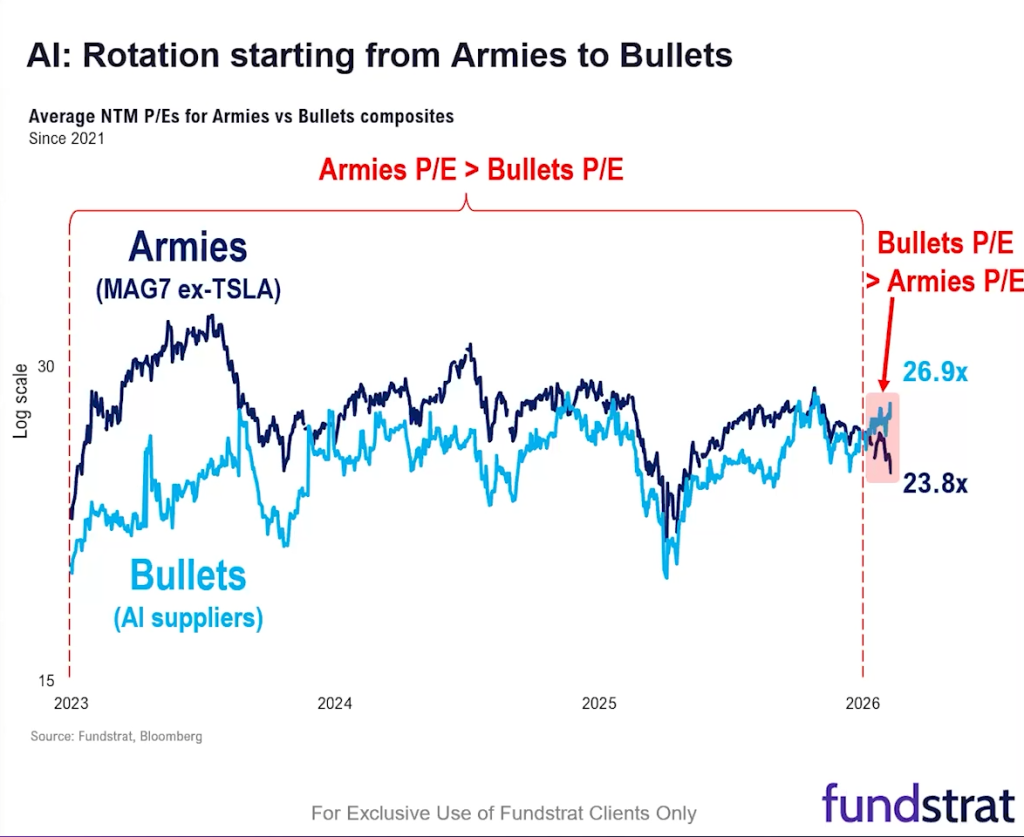

Fundstrat’s Tom Lee has been discussing the recent rotation away from the metaphorical AI “armies” – basically the Magnificent Seven excluding Tesla, and into the so-called “bulletmakers” – those supplying the “armies.” As many will recall, this is a group that includes companies in energy, memory chips, infrastructure, and networking. As Lee pointed out in our Chart of the Week above, this rotation has resulted in the bulletmakers now having a higher P/E ratio than the armies. To him, this suggests that “we’re pretty far through the rotation out of the Mag Seven.” He stressed, “We don’t necessarily want you to be a hero here, but I do think that means an opportunity is emerging when we rotate back into the ‘armies’, and I’d keep some dry powder.”

Super Court rules Trump tariffs are not legal. Attached are some thoughts post-Supreme Court:

The Supreme Court decision is as expected and is not a surprise, but the timing was unknown

The administration may try several paths, including: Congress puts these tariffs into law (perhaps using reconciliation) White House uses other measures to get new tariffs

Investors will view this as disinflationary

And some will see this as putting limits on executive power, which will be viewed positively by some investors What would we do now

This was an overhang (the decision), so this is a risk-clearing event

This is positive for stocks, in our view because of that

To us, this makes it easier for Fed to see path of inflation lower = possibly more rate cuts

Sectors

We will favor Energy/Materials as top ideas

Tech/ Software/ Crypto suddenly look more interesting, because they are not caught up in tariff “messiness”

We think MAG7, crypto and software are in the later innings of their correction

So we would be buyers of these in the coming weeks (as they make their way to their lows)

The tariff ruling sparked an initial bounce and Equities have extended gains to near the highs of the day. Technically this is a good sign, and i agree with Tom Lee that today’s decision was a risk-clearing event (for now) and should help drive Equities back to recent highs. Many sectors remain somewhat muted outside of Technology and Comm. Svcs, and market breadth is only around 3/2 positive at this time. However, the move to multi-day highs on a closing basis is a positive for SPX and QQQ and should help to drive prices higher into the time of Feb 27th which i expect could be an important time for Equities

Big news from DC with a 6 to 3 decision against the Trump tariffs. What does the White House and Republican Comgressional Leadership do in response? Any legislation under regular order would be filibustered by Senate Democrats. While aides are still researching the possibility one idea may be the Reconciliation process the Congress used to pass the BBB last year. One group of legislators to watch is farm state Republicans who in the past have been anti-tariffs as US agriculture is one of the easiest targets for retaliatory action by trading partners hurt by US tariffs. Another interesting dynamic could be next week’s State of the Union when several Justices often come and sit in the front row facing the President. President Trump can be tough on his opponents and does this action now place Chief Justice Roberts and the five other justices on the President’s enemies list? Stay tuned!

This research is for the clients of Fundstrat Direct only. Fundstrat Direct Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or Fundstrat Direct at fundstratdirect.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of Fundstrat Direct. At the time of publication of this report, Fundstrat Direct does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

Fundstrat Direct is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

Fundstrat Direct is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of Fundstrat Direct (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by Fundstrat Direct clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of Fundstrat Direct, which is available to select institutional clients that have engaged Fundstrat Direct.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

Fundstrat Direct does not have the same conflicts that traditional sell-side research organizations have because Fundstrat Direct (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by Fundstrat Direct and/or affiliates of Fundstrat Direct. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of Fundstrat Direct.

This research is for the clients of Fundstrat Direct only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but Fundstrat Direct does not warrant its completeness or accuracy except with respect to any disclosures relative to Fundstrat Direct and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where Fundstrat Direct expressly agrees otherwise in writing, Fundstrat Direct is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fundstratdirect.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.

- This was an overhang (the decision), so this is a risk-clearing event

- This is positive for stocks, in our view because of that

- To us, this makes it easier for Fed to see path of inflation lower = possibly more rate cuts

Sectors- We will favor Energy/Materials as top ideas

- Tech/ Software/ Crypto suddenly look more interesting, because they are not caught up in tariff “messiness”

- We think MAG7, crypto and software are in the later innings of their correction

- So we would be buyers of these in the coming weeks (as they make their way to their lows)

ETH 0.98% BTC 0.84% IGV -1.26% MAGS 1.61%