Summary

- We recently upgraded Financials to overweight in anticipation of the improving healthcare situation, potentially accelerated tapering timeline, and a likely upward move in rates.

- KeyCorp is a strong regional bank with a geographically appealing profile, a strong relationship lending franchise, and a fast-growing consumer lending segment.

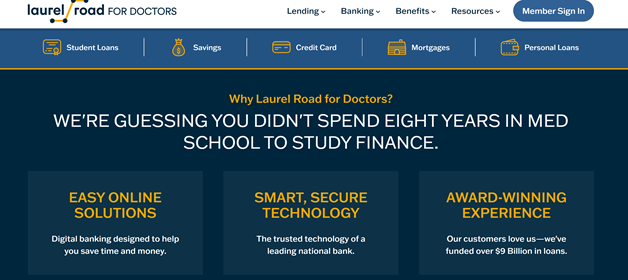

- The bank’s launch of Laurel Road For Doctors, a nationally available digital banking experience for physicians and healthcare professionals, shows innovative thinking for an often stale industry and has brought actual lending and deposit growth.

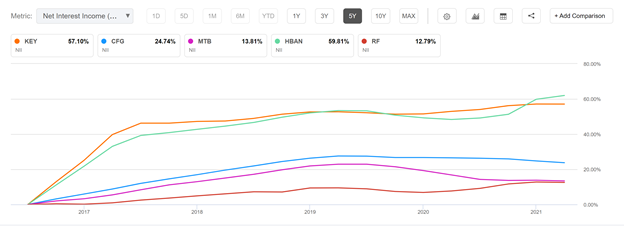

- KeyCorp has recently seen some slight margin compression from lower rates, but this should be alleviated when rates reverse course, as we expect. The bank has a healthy proportion of floating loans to benefit from rates rising as compared to peers.

- The bank has pristine credit assets and a robust and valuable presence in commercial lending. The company sees evidence of a coming rebound in commercial lending, which gives this stock additional medium and long-term upside. Utilization on commercial lines has likely bottomed.

On June 11, our Head of Research, Tom Lee, downgraded Financials from overweight to neutral. As we began to see interest rates decline significantly, we believed this would hold back upside in Financials compared to other Epicenter sectors like Energy, Materials, Consumer Discretionary and Industrials. The general rotation toward growth and away from value hurt Financials as well.

As the macro environment has changed concerning rates, we now see Financials re-coupling with other Epicenter sectors and leading the markets’ gains into YE. Financials and regional banks are considered to be good hedges against inflation as well. KeyCorp has shown improving momentum on growth and lending metrics and is an industry-leading regional bank to add to the portfolio to capitalize on macro and enterprise-level drivers.

We are known for following COVID-19 very closely to monitor its potential impact on markets. We have seen Delta roll over in the most adversely affected areas, and some of our favorite sources like IHME and Dr. Scott Gottlieb have been suggesting that the current wave is coming to an end, and that it may be the final wave of COVID-19 for the year. This means growth concerns around Delta have likely been overdone by the market, and rates should reset higher to reflect this.

This rosier scenario contrasts what happened last year when cases surged in the fall in the Northeast. We have noticed markets tend to trough well before cases peak. This fact, along with the likely acceleration of Fed tapering, removes the primary obstacles that led to our downgrade of Financials. We also have seen multiple positive technical indicators that suggest near-term upside.

Regional Banks Set To Benefit From Any Rate Rise And Acceleration of Tapering

The almighty spread is how banks primarily make money, especially the large regionals. They are engaged in the vital function of maturity transformation, where they take short-term deposits from households and turn them into longer-dated loans for consumers and businesses. The clear trend in the banking industry over the past decades has been one of consolidation. There were about 15,000 banks in 1985; today, there are about 4,500. The top four banks have over 40% of all banking assets in the United States.

We suspect that pessimism over adverse healthcare developments has come close to reaching a climax, and we believe the recent period of underperformance by regional banks compared to the S&P 500 has just reversed meaningfully. Banks have been consistently among the highest beta stocks since the virus began dominating markets. Therefore, we think they will particularly benefit in the “everything rally” we see coming on the heels of Delta’s reversal.

The coronavirus crisis and how banks responded have significantly repaired the lousy reputation they received in the wake of the financial crisis. This time around, the banking system has been a source of strength that the national economy relied on rather than an over-leveraged liability. Despite the high drama of the asset-backed security collapse in 2008/09 and the extreme shock the banking system endured in the crisis, it is supposed to be a pretty dull business. KeyCorp is beautifully boring in some ways while also having its finger on the pulse regarding several industry trends like digitization.

KeyCorp rode the wave of risky construction loans that resulted in more bank failures than mortgage exposure in the wake of the financial crisis. Those have gone from 42% to 14% of CRE loans from then until now. Remember, bank failures were more plentiful among the smaller banks. The bank has made a dramatic turnaround from these risky days and now has pristine credit assets, high-growth initiatives on its consumer lending side, and a better dividend yield than most peers. Share buybacks and dividends from Q2 would have returned 11% on an annualized basis, which is nothing to scoff at.

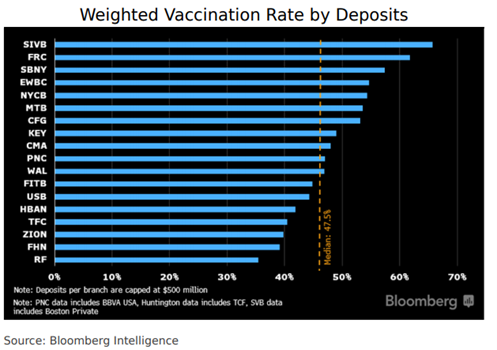

Similarly, we think that regional banks, in particular, will benefit from higher economic growth, rising rates, and a return of business borrowing and CAPEX to more normal levels. KeyCorp is well-positioned along all of these lines. It has a 69%/31% commercial to consumer loan ratio. It also has a higher proportion of floating loans than many of its peers at around 60% of all loans, which should boost net interest margins as rates rise and the curve steepens. Furthermore, KeyCorp operates primarily in states with higher median vaccination rates.

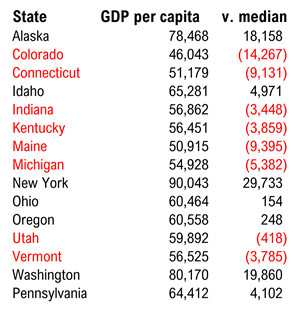

KeyCorp’s NorthEastern, Western and Mid-Western branch profile means any future problematic strains will probably less adversely affect it than banks with branch profiles concentrated in the Southeastern United States like Regions Financial or Truist. Generally, the bank has exposure in a diverse group of states where GDP per capita tends to be above the national average. Conversely, exposure to some states with lower than average GDP per capita helps the firm utilize its regional and community expertise to gain exposure to internal catch-up effects in its loans and investments.

Relationship Lending Is More Than Free Pastries

There is an old joke in banking that the last great innovation in the industry was the Automated Teller Machine (ATM), which has been around for quite some time. The business of banking is primarily concerned with the ability to profitably loan deposits out, and this is where community understanding and knowledge can translate into better returns to shareholders. The rise of the large national banks has created many opportunities for more specialized shops to get better returns in lending. KeyCorp even has a thriving investment banking practice with niche middle-market clients, which has led to robust growth on the non-interest side.

KeyCorp has made an example-setting power move in the banking industry by expanding its regional-based relationship lending expertise to expand into an industry of high-earners and voracious consumers of credit, doctors. By creating the type of specialization that works on a regional level in an affluent profession that gives the bank pipelines to loan demand in states where it doesn’t operate will likely prove a prescient and lucrative decision, in our estimation. The bank is experiencing growth in consumer customers far above its peers, and without the dramatic price cuts they have to make to attract business.

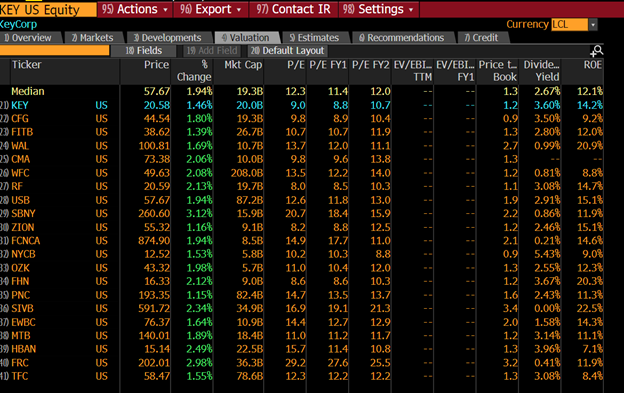

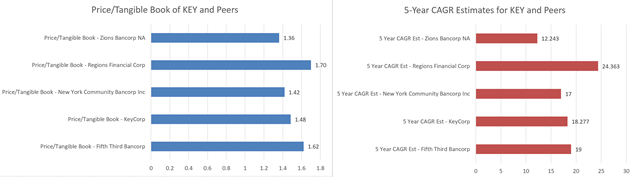

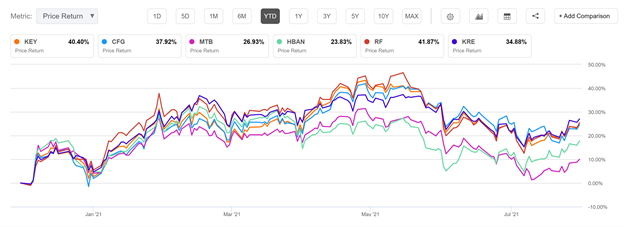

Bank stock price multiples have been declining since the beginning of the year, and many exposed to the sector got a fresh lesson in valuation risk. The improving macroeconomic conditions and healthcare situation we expect should likely lead to a reversal of this process. Even if it doesn’t, KEY seems undervalued, mainly when measured against peers. The trends in revision have been upward.

The big guys simply do a credit check and will not work very hard for borrowers who do not precisely fit the more stringent lending criteria that have been pervasive since the passage of the Dodd-Frank Act. One side-effect of these regulations has been little quirks like borrowers who are clearly qualified to buy a house being unable to secure a loan because they lack a W-2 These regulatory inefficiencies are opportunities for more specialized regional players. KeyBank, for example, keeps about 70% of its burgeoning mortgage business on its balance sheet rather than selling to GSEs. This gives them more discretion to lend to borrowers using their localized and specialized knowledge at the branch level.

The intangible knowledge and embedded nature of large regional banks in the communities they serve mean that they keep pace with the Net Interest Margins of the big guys despite their inferior network effects and cross-offerings, we believe. KeyBank is the 20th largest bank in the United States and has about $170 billion in assets, making it about one-tenth of the size of the smallest national bank, Citibank.

When Enterprise Momentum and Macro Momentum Line Up, Good Things Tend To Happen

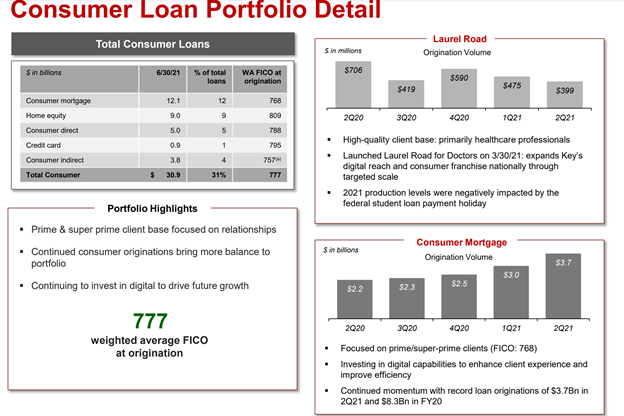

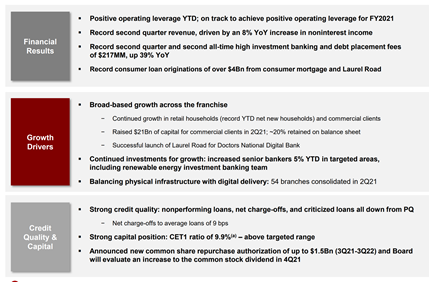

KeyCorp’s second-quarter results showed significant strength across the consumer lending business and their new forward-looking digital bank for doctors, Laurel Road. While many banks are lowering standards to seek out elusive loan growth, KeyCorp has lent to more new households so far this year than any of the whole previous ten years.

Analysts’ EPS estimates for the bank have risen significantly since the year began, and they continue to. The bank achieved positive operating leverage and expects to maintain it for 2021. Valuation is pretty competitive compared to peers, as you can see below.

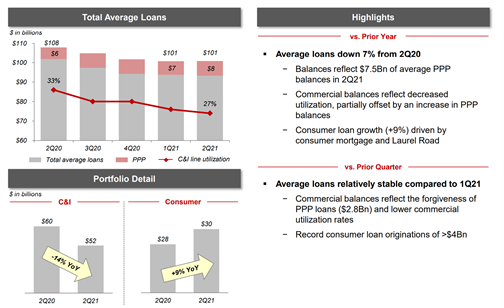

There was, however, some weakness in the C&I loan segment, which is nearly 70% of the bank’s assets. The 14% decline YoY was probably exacerbated by the rise of Delta and the adverse effect on business confidence. The utilization of commercial lines peaked at around 40% at the beginning of the healthcare crisis versus the mid-thirties historically. The company thinks a turnaround is beginning and has seen the rate stabilize around 27%.

This temporary weakness in the company’s largest segment has been mitigated by high growth on the consumer side. Still, when both components are growing at faster rates, the valuation multiple, which is lower than peers in many cases, should re-rate higher. We’re comfortable holding this bank for multiple years, given that management seems to have their finger on the pulse and that 80% of new loans are from relationship clients that use the bank’s network for a variety of loans and services.

In terms of macro drivers, we believe that the 10-yr bond rate is set up for a classic intermediate-term reversal. Cyclicals, particularly banks and transports, should be a beneficiary of this. We believe these macro tides will likely lead to most regional banks rising, but we wanted to select a stock that you could feel comfortable owning for a more extended period as well. The commercial portfolio in forward-looking areas such as renewable energy, healthcare, and technology is also favorable from a risk and ESG perspective.

We want a bank whose business model and growth will stand up to the push and pull between value and growth over time. We also want one in the middle of the road in terms of interest rate sensitivity, with high-growth initiatives, to limit the downside that has been pretty harsh in many regionals. Regional banks are very much subject to tortoise/hare logic. Superior quality benefits shareholders over time, particularly when paired with industry-leading dividends.

Risks And Where We Could Be Wrong

The banking industry is one of the most closely correlated to macro developments like interest rates and the policy posture of the Federal Reserve. Therefore, any non-consensus development in these areas could adversely affect or positively affect the price. For example, if inflation data suddenly reversed and showed strong deflationary trends, regionals would likely continue their recent adverse price activity. If rates surprise the upside, or action occurs to steepen the curve like a new “Operation Twist,” then the upside could be pretty substantial. One of KeyBank’s strengths is that we believe its management’s conservative approach will enable it to thrive better than its peers in the case of macroeconomic surprises.

There’s always a chance when picking an individual regional bank that you get nailed with some unforeseen idiosyncratic risks that might hit it at the local level or may have been missed by markets. So far this year, KeyCorp has been in the top echelon of performers amongst its peers and has not been a laggard. A bank’s credit risk and cost of funding are critical to its success and profitability, and our subject is generally ranked better than peers.

However, the most significant risk to banks, which have been amongst the highest beta sectors since COVID-19 began dominating markets, remains that adverse healthcare developments will significantly impair prospects for economic growth. Banks are undoubtedly overcapitalized, and net-charge-offs are still declining and at all-time lows. This means the typical credit risk is far more muted than the usual leading role in a bank’s business viability. Anything that stifles re-opening and loan growth could be harmful to the bank up to and including new problematic strains of the virus. Supply chain disruptions may continue to lead to lower-than-historic commercial credit line utilization. However, we are also comforted by KeyBank’s specialty in renewable energy and affordable housing.