“There have been mutterings that the whole food thing has gone too far in America, but I think not. Good food is a benign weapon against the sodden way we live.” – Jim Harrison

On March 27, the White House invited a large group of farmers to commemorate a $12 billion aid package that had been awarded to mitigate losses they incurred due to President Trump’s as-yet-unresolved tariff war. The president then told the assembled group that he planned to request another $15 billion in assistance. Farm welfare, which typically enjoys bipartisan support, was touted as still necessary by House Agriculture Committee Chair Glenn Thompson (R-Pa.), who cited “the disruption that’s caused by trade negotiations” and “the availability of inputs” as key reasons why even more assistance was “a must.”

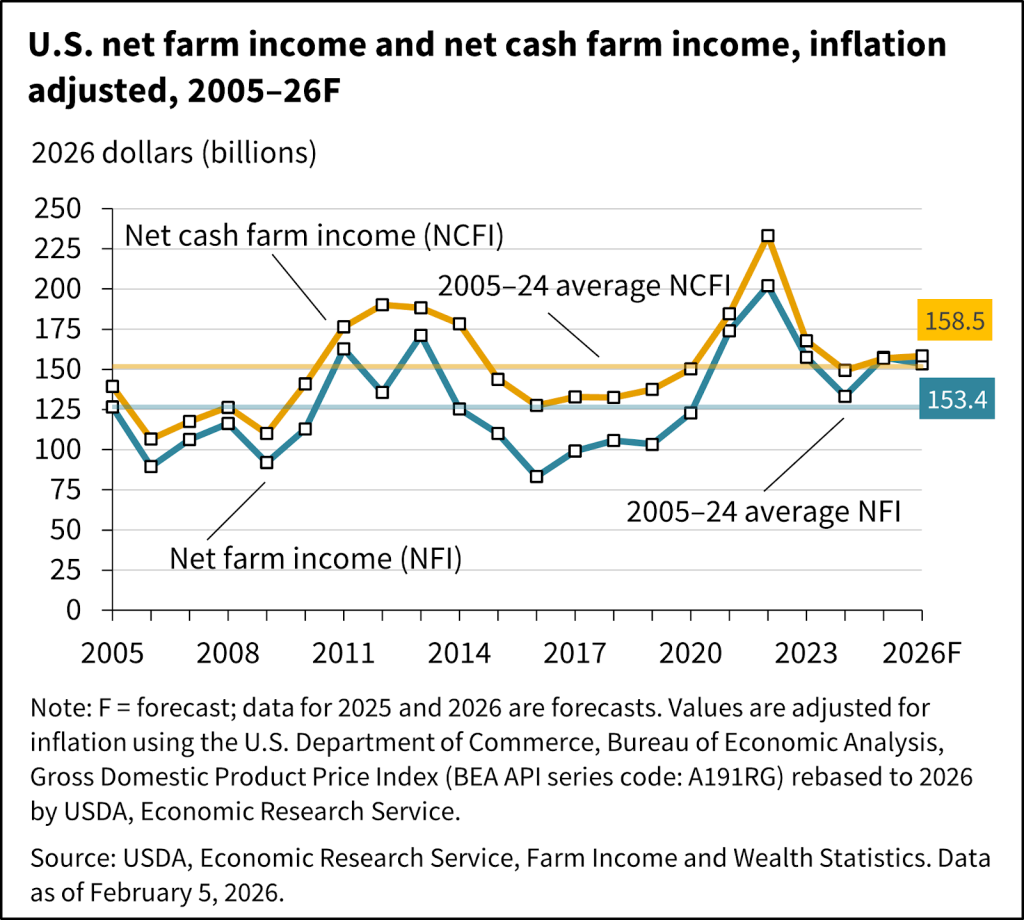

Some might question whether farmers as a group are really struggling that badly. Adjusted for inflation, farm-sector equity is projected to climb in 2026. What’s more, the most recent government projections from February 2026 have median farm household income likely to reach $110,014 in 2025 and $113,031 in 2026 – well above median household income for the U.S. as a whole, currently projected at around $85,000-$86,000. That sounds pretty good.

Yet a deeper look suggests that all is not well: Farm bankruptcies once again rose in 2025, up 46%. And while a massive increase in government assistance helped U.S. farm net income rise in 2025, even a bigger boost in subsidies this year is now projected to still result in a decline in 2026.

It’s also important to note that those positive numbers for farm household income aren’t all that positive at all. In farming households, non-farm income accounts for 77% of household income, and median operating profits in 2025 were at a projected negative $1,498. Which means that if not for members of farming families getting outside jobs to stay afloat, farm bankruptcies very well might have spiked even higher than they did, and if not for a significant boost in already generous government subsidies, that possibility would have become even more probable.

As for farm-sector equity, that is largely explained by the increased value of the land being farmed – lately driven in some part by tech companies looking for places to build new data centers. Tech companies particularly like land with access to high-voltage transmission lines, existing water rights, and locations far from densely populated areas where locals might complain about higher electricity prices. Farmland tends to check all those boxes.

Farmers who don’t sell might be able to borrow against climbing acreage values, but such elevated land prices also come with higher property taxes and land-use costs. For anyone hoping to continue farming, higher land values thus mean little without a way to increase revenues and profits.

U.S. farmers have had it particularly rough for the past year and a half. “Liberation Day” in April 2025 wreaked havoc with U.S. farmers. Annual U.S. agricultural exports declined by more than $5 billion in 2025 (modest increases in some areas were more than offset by larger declines in soybean exports), as China (and other countries) once again zeroed in on U.S. agricultural exports for retaliation – just as they did during the first Trump term. After all, agricultural commodities are, by definition, fungible, and it’s well known that much of the current president’s base comes from farm country.

Yet as a business model, farming has not been enviable for decades. Farms have struggled to make money for the better part of a century, despite being the beneficiary of generous U.S. government subsidies since before most of us were born (1933). No wonder there’s long been such a shortage of human beings who are still willing to do farm work. Even with modern machinery, farm work remains torturously grueling – and dangerous. A farm worker is more likely to die on the job than a police officer or, during non-combat years, a military service member. Americans, even those raised in farming families and communities, are almost entirely seeking jobs that are less dangerous and less backbreaking. In 2025, more than 415,000 agricultural positions were advertised. Just 0.04% received American applicants. (Plenty has been written elsewhere about the effect of President Trump’s immigration policy on the supply of migrant farm workers that have historically filled the gap, so it need not be discussed here.)

Free-market purists might argue that we should simply let enough farms fail until the surviving production capacity declines enough to raise food prices to profitable levels. Politically, this is not so simple. In rich countries like the U.S., the rural areas tend to wield a disproportionate level of voting power relative to their city-dwelling counterparts, so realpolitik dictates that it makes sense to cater to those voters.

More importantly, an agricultural system that generates yearly surpluses is a matter of national security, and thus, so is propping it up. Making sure the people have something to eat is a common-sense guard against extreme civil/domestic unrest – simply look at the number of historical dynasties that have fallen after food shortages in ancient times, from the French ancien régime and Ming dynasty of China to Tsarist Russia and ancient Egypt. In the modern era, Hubert Humphrey and Gerald Ford lost presidential elections in part due to food shortages and prices, while the spark that ignited the Arab Spring was the rising cost of bread. Meanwhile, wealthy countries also use agricultural surpluses as an avenue for foreign aid, through which they accrue and exert influence on the world stage. (This has been a cornerstone of U.S. foreign policy since the Cold War.)

Low food prices, even if they require both government subsidies and challenges for farmers, also benefits countries with consumer-driven economies. Fifty years ago, 13.7% of U.S. household income was spent on food. Today it’s 10.4%, and it would be lower if U.S. households weren’t eating out so much more frequently. (To be fair, the percentage was lower in 2012, 9.5%). For the economy, that’s arguably been a good thing: affordable food means more disposable income, which drives a range of discretionary spending and retail investment that passes through to other sectors.

All this makes the case for continued subsidies more compelling, even if it goes against conventional wisdom about laissez-faire. Thus, many policy experts view the subsidy program as unlikely to change in any material sense, especially since the removal of U.S. subsidies would also put American farmers at a competitive disadvantage in global markets.

Inputs

The problems facing the American farmer (and to a certain extent, farmers all over the world) comes from the escalating costs of many of the inputs that go into the production of wheat, or spinach, or beef.

Followers of our work know that when we track inflation, we tend to focus on “core” inflation (Core CPI, Core PPI, Core PCE) – metrics that strip out energy and food components due to their higher levels of volatility.

It’s not a coincidence that energy and food are the two volatile components. The production costs of food are correlated with the costs of energy – and not just because of the fuel needed to ship the bounty of the farm to your local supermarket.

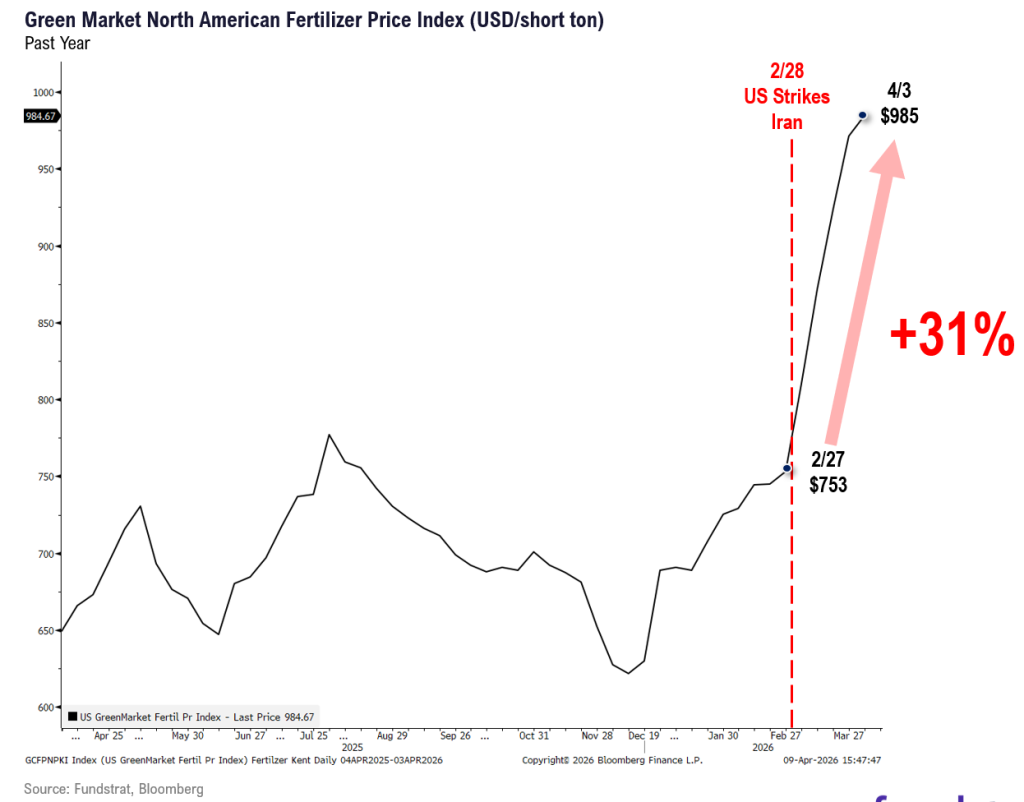

There’s also the fertilizer, and the most timely illustration of how that works is the recent war in Iran. Fertilizer, much of which is either shipped through the Strait of Hormuz or made from natural-gas feedstocks that use the same route, has gotten significantly more expensive since the Iran war began. (To be fair, the spike in fertilizer prices was more extreme after Russia’s 2022 invasion of Ukraine.)

There are no easy answers for farmers. They have long been trapped in a bit of a vicious cycle, constantly striving to boost efficiency only to see the (excuse the pun) fruits of their labors eroded as other farmers make the same adaptations, causing a shift along the inelastic demand curve that makes consumer food prices cheaper and thus keeps overall profits roughly constant – sometimes even slightly lower due to the increased debt load. Unfortunately for farmers, there is no option but to jump on this treadmill and adopt this new tech anyway because any farmer who refuses will soon find his crops too costly to sell at a profit.

It might be a different story for investors

That’s unfortunate for farmers, but it does arguably have a bright side for investors. One could plausibly assert that any new technology that can provide a demonstrable efficiency advantage is likely to see widespread adoption.

Companies that arguably lead the way in developing such technologies include developers of agricultural fertilizers, which in the U.S. is largely a duopoly consisting of:

- Nutrien Ltd. NTR 2.48% (18.0% YTD and 52.6% YoY). Nutrien is one of the largest providers of fertilizers, including potash, nitrogen (ammonia, urea, etc.), and phosphates. These products are essential for the efficient production of subsidized crops like corn, wheat, and soybeans. Nutrien stands out for operating its own chain of retail stores alongside its use of a traditional wholesale distributorship model.

- Mosaic MOS 3.69% (2.8%YTD and 2.3% YoY) is a competitor with Nutrien in most areas, with a greater presence in the domestic production of phosphates, which are particularly useful for corn farming but more dependent on imported basic materials like sulfur.

Many other things that farmers rely on have also gotten scarcer and/or more expensive. Seeds have become more expensive as seed companies seek to pass on higher R&D costs to farmers. The same goes for “crop protection” products such as weed killers, pesticides, and treatments that provide resistance against other pathogens. Both play an important role in improving productivity and yields, which farmers are incentivized to adopt – not just to compete with other farmers, but because federal subsidies are linked to yield and productivity metrics. One could argue that in a sense, farm subsidies are a boon to companies that sell advanced seeds and crop protection products. In fact, some companies develop and sell both:

- Corteva, Inc. CTVA (25.1% YTD and 44.7% YoY) is a major provider of genetically enhanced seeds and crop-protection products (pesticides, herbicides, etc.) It is a provider of proprietary seeds for corn, soybeans, and sunflowers that are resistant to extreme weather, pests, and – perhaps most interestingly, resistance to its own pesticides. This portfolio makes it possibly one of the biggest (indirect) beneficiaries of the U.S. agricultural subsidy program. It’s worth noting that Corteva (itself originally split from the merger of DowDupont) is planning to split itself up before the end of 2026, dividing into a seed company and a provider of crop-protection products, and some worry that this might disrupt the synergy currently enjoyed between the two divisions, which helps lock in farmers.

- Bayer BAYRY (8.7% YTD and 105.1% YoY) Bayer’s agricultural business (the conglomerate is perhaps better known as a pharmaceutical/biotech company) is a major Corteva competitor, with a similar lineup of genetically modified corn and soybean seeds and a portfolio of crop-protection chemicals. One source of uncertainty for Bayer involves litigation around its Roundup weed killer (produced by Bayer subsidiary Monsanto), scheduled to come before the Supreme Court later this month. Thousands of lawsuits claim that Roundup’s active ingredient, glyphosate, causes non-Hodgkin’s lymphoma. The company has already paid $11 billion in settlements with many cases still unresolved as of this writing. (In February, the company proposed a $7.25 billion payment to settle many of those remaining cases, and a court has granted preliminary approval.)

Two other companies worth mentioning are FMC FMC 3.61% and Syngenta. FMC is sometimes included with Corteva and Bayer as part of a triumvirate of major agricultural corporations. However, unlike the other two, the company’s portfolio is limited to crop-protection companies – no seeds or genetic research. This is arguably a disadvantage in FMC’s ability to lock-in customers, which has combined with its imminent patent expirations to spark concerns about its long-term health. In February, FMC announced that it was considering putting itself up for sale or merging with another company.

Syngenta, once traded on the NYSE, was acquired by the Chinese state-owned enterprise Sinochem Holdings in 2017. Globally, it is the biggest provider of crop protection products and one of the largest providers of advanced seeds. On April 7, Syngenta announced Virestina, a highly touted herbicide that it claims will tackle certain “superweeds” that have evolved resistance to older, more traditional herbicides. In February, Sinochem announced plans for Syngento’s IPO on the Hong Kong Stock Exchange, aiming to raise up to $10 billion at a roughly $50 billion valuation.

Also worth noting: Syngenta and Corteva are jointly facing a possible U.S. antitrust trial this fall. The Federal Trade Commission and 12 U.S. states have jointly alleged that the two used kickbacks, passed off as distributorship loyalty programs, to suppress competition from providers of cheaper generic crop-protection products. The deadline to settle the allegations in mediation is April 30.

Don’t forget the hardware

Federal data showed that in 1980, an estimated 3.4 million people, or about 1.5% of the U.S. population at the time, worked in agriculture. Today it’s 2.6 million, or 0.8%. An increasing portion of today’s agricultural laborers work on farms focused on fresh produce and other specialty products – crops that require a level of delicate dexterity that machines have yet to achieve.

However, what used to be done by humans on farms focused on commodity crops (grains, soybeans, corn) and on meat (poultry, pork, beef) and dairy is now largely done by specialized farm machinery. It is the manufacturers of machines that mechanize the farming process that have enabled production volumes to increase even as a shrinking number of Americans work on farms. While in recent years they have been hit by higher costs related to tariffs on steel and components, they have also been able to pass most if not all of those costs onto their customers. Two major players in this industry include:

John Deere DE 3.48% (30.0% YTD and 36.2% YoY). John Deere is a leading manufacturer of high-horsepower tractors and combines, as well as crop-protection sprayers. Deere’s machines, which include specialty-crop-focused machines, feature AI-powered full automation for planting and harvesting, with satellite-assisted steering and predictive ground-speed automation enabled by live stereo camera feeds, satellite imagery, and terrain mapping. The high cost of purchasing such machines means that their revenues are highly correlated to crop prices – farmers forgo major purchases when crop prices are depressed. In the past year, Deere has seen challenges in the form of retaliatory tariffs from countries like China and Brazil, which the company expects to have a $1.2 billion impact in 2026.

CNH Industrial CNH 3.38% (25.5% YTD and 3.4% YoY). CNH focuses more on specialized equipment, such as machines for use in fruit orchards and vineyards, though they are moving to challenge John Deere’s dominance in grain farming. The company is also more focused on European and Latin American markets, a fact that explains both its heavier emphasis on alternative fuel-friendly products and its heavier exposure to retaliatory tariffs during the second Trump administration.

The disruptors

The vicious cycle we discussed earlier is not precisely a secret. Farmers are well aware of the problem, and it’s reasonable to assume that they are eager for a metaphorical escape hatch – some technology that lets them break the cycle.

To a certain extent, the companies developing such technologies are the same ones we discussed above, the same ones that currently account for so much of a farm’s expenses.

- Corteva. Corteva introduced Utrisha N in 2021. Utrisha N is a proprietary form of naturally occurring Methylobacterium symbioticum bacteria sprayed onto leaves, where the microorganisms are absorbed into the plant’s cells. Once the bacteria have colonized the plant tissue, they pull nitrogen directly from the air and convert it into a form the plant can use directly: ammonium, NH4.

- Nutrien. In 2025, Nutrien launched N-FINITY, a proprietary blend of microbes sprayed onto the soil. Once mixed in, N-FINITY is claimed to simultaneously pull nitrogen from the air into the soil, feed existing nitrogen-producing soil bacteria, and convert the organic matter in soil into ammonium.

- Bayer. Through a partnership with Ginkgo Bioworks DNA -0.76% , Bayer has developed genetically engineered microbes that could attach to crop roots and produce nitrogen, thus theoretically reducing the amount of synthetic fertilizer. (The product is still in testing.)

While there will surely be a price exacted for such advances, the silver lining for farmers is that this time, they could eventually pay for themselves – or come close to it. Although it’s important to stress that no economic/business studies have been done on this topic, here’s some back-of-the-napkin math behind the possibility:

For every acre, roughly $15 worth of nitrogen-fixing biologicals such as the ones described above could reduce the need for synthetic fertilizer by 25-40 pounds. If this scenario holds true (and existing studies show that the benefits are not always this extensive), then it is possible that the farmer could thus claim carbon credits of up to $5 to $12, and his fertilizer costs would decline by $12 to $26 per acre. Under the optimal outcomes in this crude hypothetical, $15 worth of biologicals could result in benefits of up to $38.

As we mentioned earlier, fertilizer prices are closely tied to energy prices, and this is not always ideal. Two companies in particular are seeking to produce fertilizers with reduced reliance on fossil fuels. They are:

- CF Industries CF 3.57% (56.9% YTD, 73.4% YoY) CF is developing green ammonia that uses solar-generated electricity to apply electrolysis to water and air. Notable projects include the construction of a $4 billion green ammonia plant in Donaldsonville, La. Importantly, however, manufacturing costs for green ammonia are currently far more expensive than its traditional analog, but because electricity accounts for the majority of those costs, improvements in renewable-energy technologies could narrow that gap. (Note that green ammonia is also being investigated as a potential zero-carbon fuel.)

- ICL Group ICL 1.33% (-6.5% YTD, -15.6% YoY) ICL is a major chemicals and diversified fertilizer company. Its low-carbon fertilizer solutions focus on using mined polyhalite, a naturally occurring mineral formed during prehistoric times and found primarily in the United Kingdom. Polyhalite crystals can practically be used as is, requiring only crushing and screening (to ensure uniform crystal size). Because it requires no other processing, ICL claims that its resulting Polysulphate fertilizer has the lowest carbon footprint of any major synthetic fertilizer available.

There are also hardware-based disruptive technologies that could potentially benefit farmers. Here are some companies in that space:

Valmont Industries VMI -3.53% (5.8% YTD, 53.1% YoY) Valmont is a leading provider of precision irrigation systems. On average (across geographies and crop types), water accounts for 15-25% of a farm’s operating costs, and with the tech industry adding significantly to water demand, farmers that can make do with less water will have an advantage. Valmont’s technology works by monitoring soil moisture and plant stress to adjust irrigation in real time.

Trimble TRMB -3.47% (-17.3% YTD, +11.6 YoY) Trimble develops GPS, laser, and optical technology for use in autonomous farming. A key product is their “Spot Spray” technology, which identifies individual weeds and sprays only them – instead of the standard practice of drenching the entire field. This could not only reduce chemical usage and costs (some real-world trials suggest that the potential reduction could be up to 90%), but help farmers cater to demographics seeking food with fewer chemical inputs.

AGCO Corporation (AGCO) (16.2% YTD, 44.5% YoY) Although a manufacturer of traditional farm machinery such as tractors (including its Fendt line that has lightheartedly been dubbed the “Mercedes Benz of tractors”), AGCO differentiates itself through its brand-agnostic “Retrofit” technology—allowing farmers to add smart tech to old equipment to save money. Retrofit allows farmers to add technologies such as precision planting and autonomous tillage to older machines. The company’s business is currently heavily focused in Europe, though it is moving to aggressively expand in the U.S.

We will discuss the other side of the agricultural sector – the agribusinesses who constitute the direct customers of U.S. farmers – in a future Signal From Noise. In the meantime, we’ve come to the part of this note in which we remind readers that as always, Signal From Noise should not be used as a source of investment recommendations but rather ideas for further investigation. We encourage you to explore our full Signal From Noise library, which includes deep dives on the recent gold rush, the future of malls, drone warfare, and the race to onshore chip fabrication. You can also find our take on space-exploration investments, defense stocks, and the rising wealth of women.