Near-term trends are being tested after SPX’s break of 6700 on Friday, and any violation of late September lows of 6569 should result in the start of the anticipated 5% correction into November. Intermediate-term technical trends remain bullish for US Equities, and despite some of the sector bifurcation, I don’t expect that any selloff proves long-lasting before a rally back to new highs gets underway. Treasury yields and WTI Crude oil look to be turning sharply lower as of Friday, and both should continue down into November. Meanwhile, the VIX has risen back over 20, and this should mark the start of an eventual move back to 30 by November, before Equities lift into year-end. While the near-term uptrend for SPX from June at this time is intact, the trends for both WTI Crude and Treasury yields have made more technically important breakdowns. Regardless if SPX can bounce next week into 6800, I suspect that Friday’s deterioration caused some further waning in breadth and momentum that likely will give way to a Fall selloff. As mentioned in recent days, it’s important to remain vigilant as some cross-asset volatility has begun, which likely persists over the next month.

Needless to say, Friday’s sudden about-face wasn’t expected by me nor global markets right away, which appear to have been caught off-guard by signs of a possible prolonged trade war with China. Implied volatility spiked while Treasuries surged, and both the US Dollar and Emerging markets pulled back sharply, given China’s equity market weakness.

I’ve been expecting that a US equity selloff could happen between mid-October and mid-November of this year given factors such as waning breadth, sector weakness in non-Technology, rising positioning and sentiment within the US Equity market.

However, there had been precious little evidence of technical trend deterioration, and stocks like NVDA had continued to show above-average strength back to new all-time highs, which largely served to camouflage the deterioration in other sectors lately. Thus, this was expected to begin sometime in mid-October, shortly following the six-month (180-day) rally off the April 2025 lows.

Interestingly enough, even with evidence of Equal-weighted ^SPX and DJIA having pushed back to new all-time highs in the last month, this breakout failed to lead to meaningful broad-based strength in markets. Many of the sectors that had led the advance earlier this year, such as Consumer Discretionary, Communication Services, Financials, and some parts of Industrials, all began to lag performance over the last month.

However, it is today’s price weakness that is finally demonstrating the first evidence of confirming some of the negatives that had been mentioned over the last couple of weeks. ^SPX’s break of 6700 was a technical negative intra-day that immediately led price down to within striking distance of late September lows, along with a challenge of the larger area of trendline support(as shown below).

Thus, I expect that price has likely reached short-term support on Friday’s decline. However, any break of 6569 would violate late September lows along with the ongoing uptrend that would likely signify that a Fall correction had gotten underway. Until price confirms that a downtrend is officially underway, it’s premature to weigh in on downside targets. However, I believe that a 5% pullback is possible and should be healthy for US Equities ahead of a further push higher into year-end.

S&P 500 Index

TNX looks to be turning lower. Break of 3.99% anticipated

Friday’s downturn in yields looks important and negative technically and should lead to yields turning lower into November, along with yield curves likely steepening as the short end of the curve pulls back at a faster rate.

Given that many investors concentrate on ^TNX, the US Treasury Note yield index, we see below that yields have broken early October lows, given Friday’s volatility.

This is bearish for yields, technically speaking, and should lead yields to test and break prior lows near 3.99%. The progression lower in yields since July looks to be setting up for a “final” drop of this advance since July down to near 3.90%.

Such a pullback in yields would complete a “5-wave” Elliott-style decline in yields, setting up for a bounce into the end of the year.

At present, today’s move is quite bearish for Treasury yields, and I like owning SHY, IEF, along with TLT for gains into November.

US Government Bonds 10 YR Yield

Crude oil looks to have begun its descent to test Spring lows

Today’s breakdown in WTI Crude oil also looks important and negative technically, which follows today’s news of a possible re-escalation with China, giving way to the thought that a possible deeper and more protracted trade war with China might be back in the cards.

The Gaza ceasefire has served to alleviate worries about a supply disruption out of the Middle East, and the narrative on Oil is growing increasingly more bearish. Today’s breakdown to the lowest levels since Spring is a technical negative for Crude and by extension, the Energy sector.

I believe that WTI Crude futures have begun a drop to test and possibly break Spring lows. It looks right to avoid buying dips in Energy names and expect that Crude’s big-range decline today should lead Crude down to the low $50’s initially.

Light Crude Oil Futures

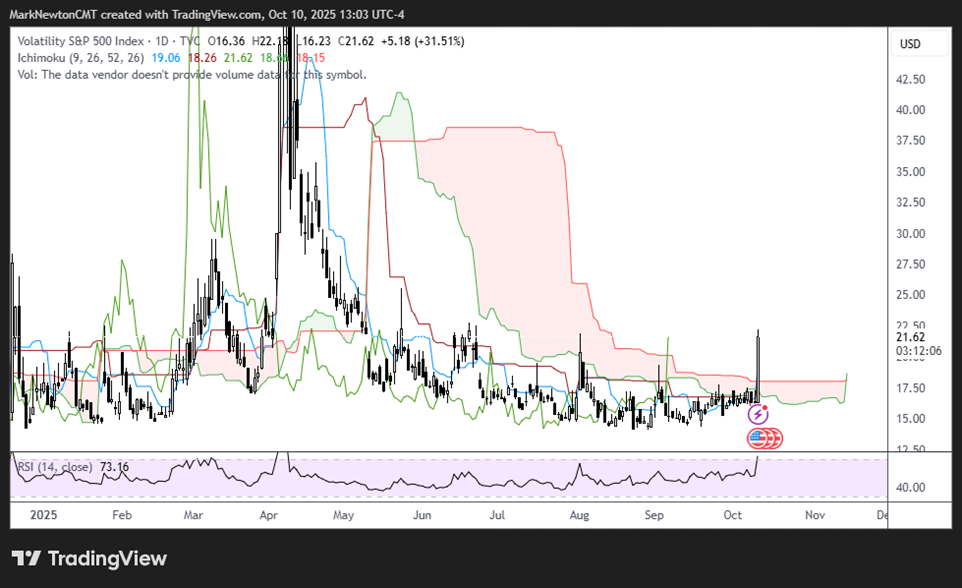

VIX likely pushes higher to 30 into mid-November, but it won’t be a straight line

The sudden lift in implied volatility looks important as the VIX moved quickly back above 20, rising to multi-week highs.

Given that markets were caught off-guard on Friday, a sharp rise in VIX makes sense, and technical targets lie near 30 into mid-November.

If Equity indices can stabilize and begin to bounce next week, a minor decline in VIX likely would make this attractive for a further push up into November.

Overall, today’s VIX strength, given unexpected news, looks to be the “Shot across the Bow” that many investors felt should happen in August or September.

However, now that markets had passed that normally negative period of seasonality without much of a selloff, positioning and sentiment had become more bullish, which, from a contrarian standpoint, looked to be a negative. Bottom line, I expect VIX to be higher into next month, but am not expecting that VIX revisits Spring lows. Technical resistance seems to target 30, which I feel is a good likelihood in the next month before Equity indices bottom and turn higher into year-end.

Volatility S&P 500 Index