Near-term Equity trends are short-term bullish, and despite the carnage continuing to be seen in parts of Technology, it’s just difficult to call the trend bearish given no material breaks of either the trend from last November nor December lows. Moreover, Equal-weighted SPX managed to rally back to new all-time highs today while DJIA just barely missed and lies roughly 90 points below. As has been discussed in recent days, it’s important to become accustomed to the violent sector rotation and cross-asset volatility being seen across markets. However, given that DJIA, IWM, MDY, ^SPX, NDX and DJ Transportation Average all hit new all-time highs in the last month, while sectors like Materials, Energy and Consumer Staples are showing stellar signs of outperformance, it’s truly difficult to yet make too much of our rotation out of various Technology stocks. While there continues to be a big push into Value from Growth, I don’t sense that its right to try to top-tick markets just yet given no signs of trend weakness. Similar to yesterday’s conclusion, it’s right to remain bullish, but increasingly more selective, and diversified around some of the other parts of the market which have begun to strengthen in recent weeks and months.

I continue to view this minor consolidation from last week’s highs as a likely buying opportunity and can’t find much fault with recent trends despite some of the exodus out of parts of Technology.

While the recent churning certainly feels quite negative, ^SPX has now closed well up off the early lows on five straight days. While it’s been difficult for sub-sectors like Software to show convincing signs of bottoming out, my view is that January lows should not be taken out right away.

Furthermore, I’m expecting a coming push back to new highs and an eventual move to 7100-7200 sometime in February before any sort of meaningful peak develops.

Despite Tuesday’s early weakness, ^SPX failed to close down under 6862 and managed to rally well up off earlier lows.

Given that most of the cycles point to late February, not late January for a peak in ^SPX and weekly and monthly DeMark counts are not in place at this time (exhaustion signals) I’m still expecting that Technology can lift and join some of the strength in other sectors before any peak develops.

As always, if meaningful weakness gets underway, then it will be right to address it which initially would take the form of a decline to new monthly lows. For now, many parts of the US stock market are working just fine, and we’ve simply seen some rotation out of Growth. While Technology demands some selectivity at this time, it’s right to favor further near-term outperformance in RSP over SPY and expect that the broader market remains in pretty good shape.

S&P 500 Index

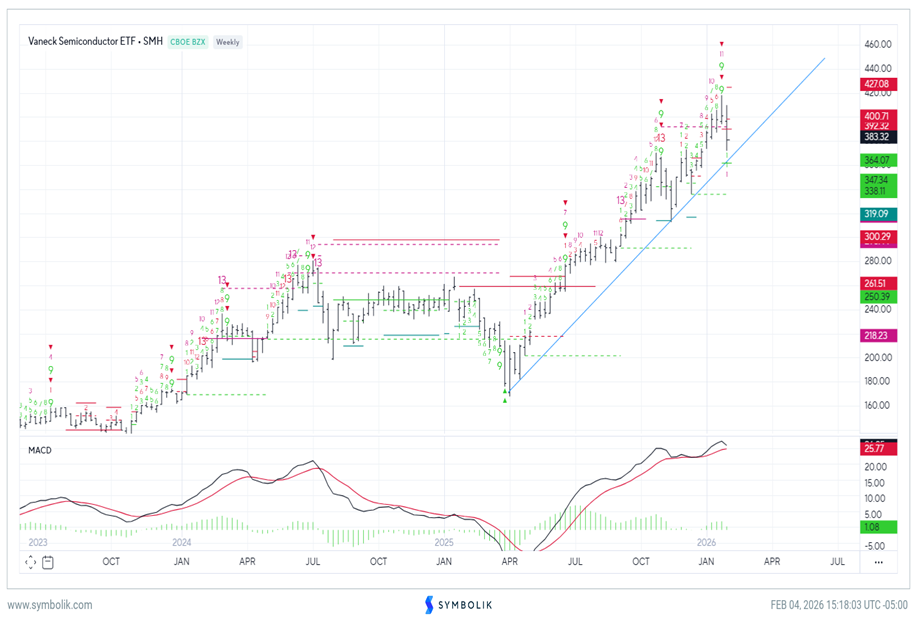

Semiconductor stocks do not look to be peaking just yet, despite the fear of any imminent rotation of the selling pressure from Software into “Semis”

There were dozens of questions today regarding the Semiconductor sector and whether the selloff has begun in this sub-sector as the Software malaise spreads to Semis. My thinking is it remains still early to expect that “Semis” are peaking out, and expect a push back to new highs before any peak is in place.

When looking at SMH on an absolute basis, along with SMH to RSPT on a weekly and monthly, it still looks premature to make any sort of compelling case for a top.

No evidence of either weekly nor monthly “13 Countdown” exhaustion (Sells) are present like they were back in 2021, or 2024 ahead of the selloff into 2025 for Semis. I’m inclined to think that a “final” push back to new highs can happen at some point this month.

However, it is proper to say that the risk/reward on a drop to new weekly lows is growing more negative. If/when SMH can get back to highs and satisfy DeMark counts on weekly or monthly basis, or actually violate the larger uptrend lines in place on either absolute or relative charts, i’d be a lot more inclined to think Tech goes down right away.

Given that I’ve been asked a dozen questions on this, I feel it’s doubtful that everyone has miraculously picked the top for Semis right at the peak. More proof looks necessary to make any kind of bearish call on a weekly or monthly basis or even relative basis to Tech when viewing Ratio charts. However, I do feel that “Semis” likely could peak within 3-5 weeks and turn down into late Spring and could be lower than current levels.

Thus, how one attempts to play the possible “final” push back towards highs all depends on one’s individual risk tolerance and timeframe. For now, trends remain bullish and we haven’t seen material evidence of trend violation. Weekly MACD also remains positively sloped.

Vaneck Semiconductor ETF

Silver’s bounce has shown encouraging signs

The good news for Precious metals fans is that both Gold and Silver look to have made 5-waves off the lows from earlier this week, which likely means that more rally is coming in the weeks to come following some minor backing and filling of this bounce from Monday’s lows.

As discussed, I expect a lot of volatility in the metals market and my Target for Silver upside lies at either $97, or above near $101.7. After this bounce is complete, I anticipate another pullback to test and break the lows from this past Monday. (SLV)

To reiterate, I am not expecting an immediate push back to new highs. Thus, any retracement to 61.8% or 78.6% of the recent drawdown likely represents an area to hedge and/or lighten up on Precious metals longs for those with less than a six-month time window.

Silver Futures

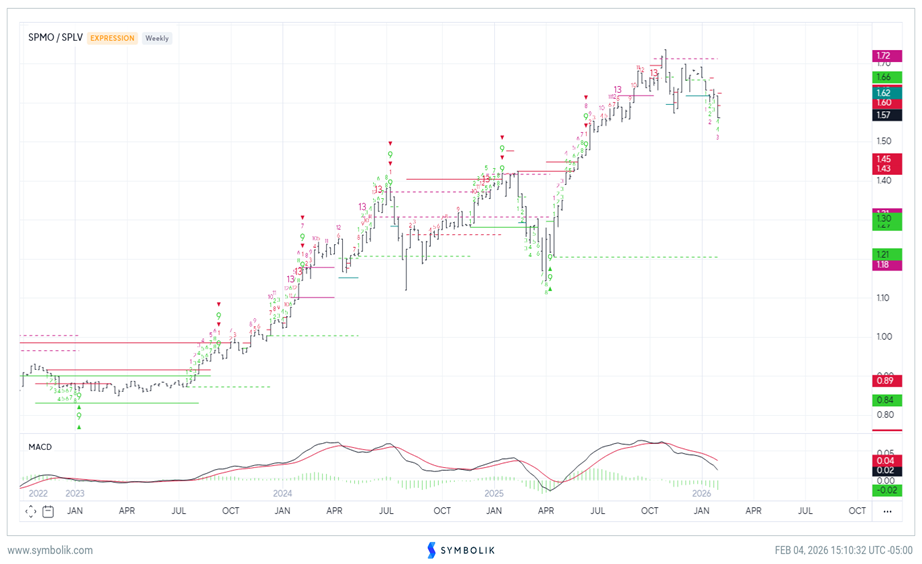

Momentum plunged vs. Value today and this might persist a bit longer

While I do expect that Technology might be getting closer towards making a comeback, it is important to relay that SPMO, the Invesco S&P Momentum ETF, made a fairly negative downside breakdown vs. the Invesco “Low Volatility ETF” SPLV.

It was said that today’s move was the fourth largest rotation from Growth to Value in more than 25 years.

As can be seen below, the ratio of SPMO vs SPLV broke prior lows and likely could show another 2-3 days of weakness into the end of this week or early next before this ratio starts to stabilize.

Unfortunately, unless today’s damage is recouped right away, it’s right to know that Value remains preferred over Growth and that the “Low Vol” areas of the market likely will do better in the days ahead than a momentum-based strategy.

SPMO / SPLV