The “fog of war,” as characterized by Fundstrat Head of Research Tom Lee, took the stock market on a wild ride this week.

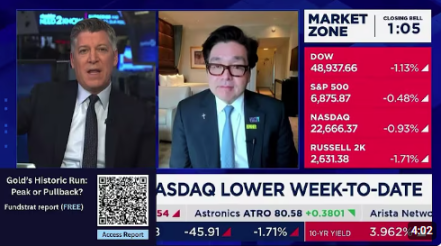

The S&P 500 lost 2.1% this week to 6,368.85 points, down for five straight weeks, marking the longest losing streak since the seven-week long stretch ending in May 2022. The Nasdaq composite, meanwhile, entered correction territory, meaning that it has fallen 10% or more from a recent high. It was down 3.2% this week. This month, the S&P 500 is on track to decline 7.4%, its worst monthly performance since 2022.

The week started off with high spirits after the president posted on Monday morning that he had a “very good and productive” conversation with Iran, reversing the declines noted by stock futures over the weekend from concerns about an amped-up war. And it didn’t matter to investors that Iran said it had no wind of such talks because at least it seemed like the president was considering an exit strategy. But as the week progressed, once again investors realized that it’s not so easy to exit the war. On Thursday, the president said he is pausing strikes to allow for negotiations.

Though the whiplash is annoying, it’s a good reminder that the president cares about the stock market. “Today was a reminder that the Trump put comes into play,” Lee said on Monday.

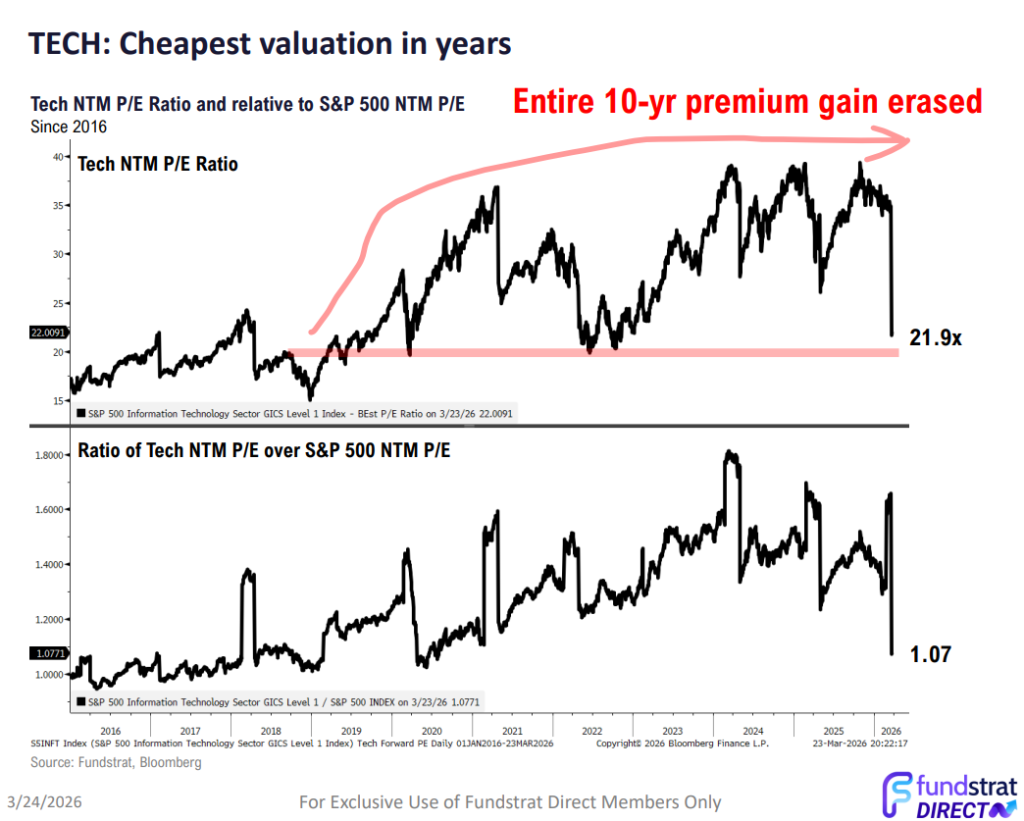

Lee highlighted that there’s still opportunities available in the market, despite all the red lately. Tech stocks, for example, are trading at valuations last seen a decade ago, he said.

Head of Data Science “Tireless” Ken Xuan believes that the end of the war is near. One reason for that is because the president set a date of May 14-15 to meet with Chinese President Xi Jinping.

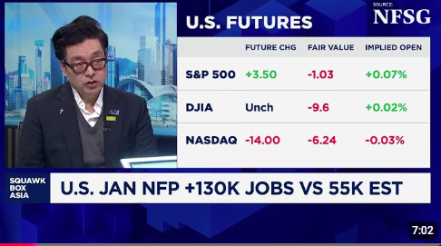

Still, it’s becoming clearer that the impact on the energy markets from the war will take months to resolve. That means that the worry of higher oil prices feeding into inflation might remain a concern for longer than expected, which could change the calculus of the Federal Reserve’s next move. As it is, the Fed is struggling to balance its dual mandate of maximum employment and price stability. They will get a fresh look at the state of the labor market on Friday with the release of the March nonfarm payrolls report.

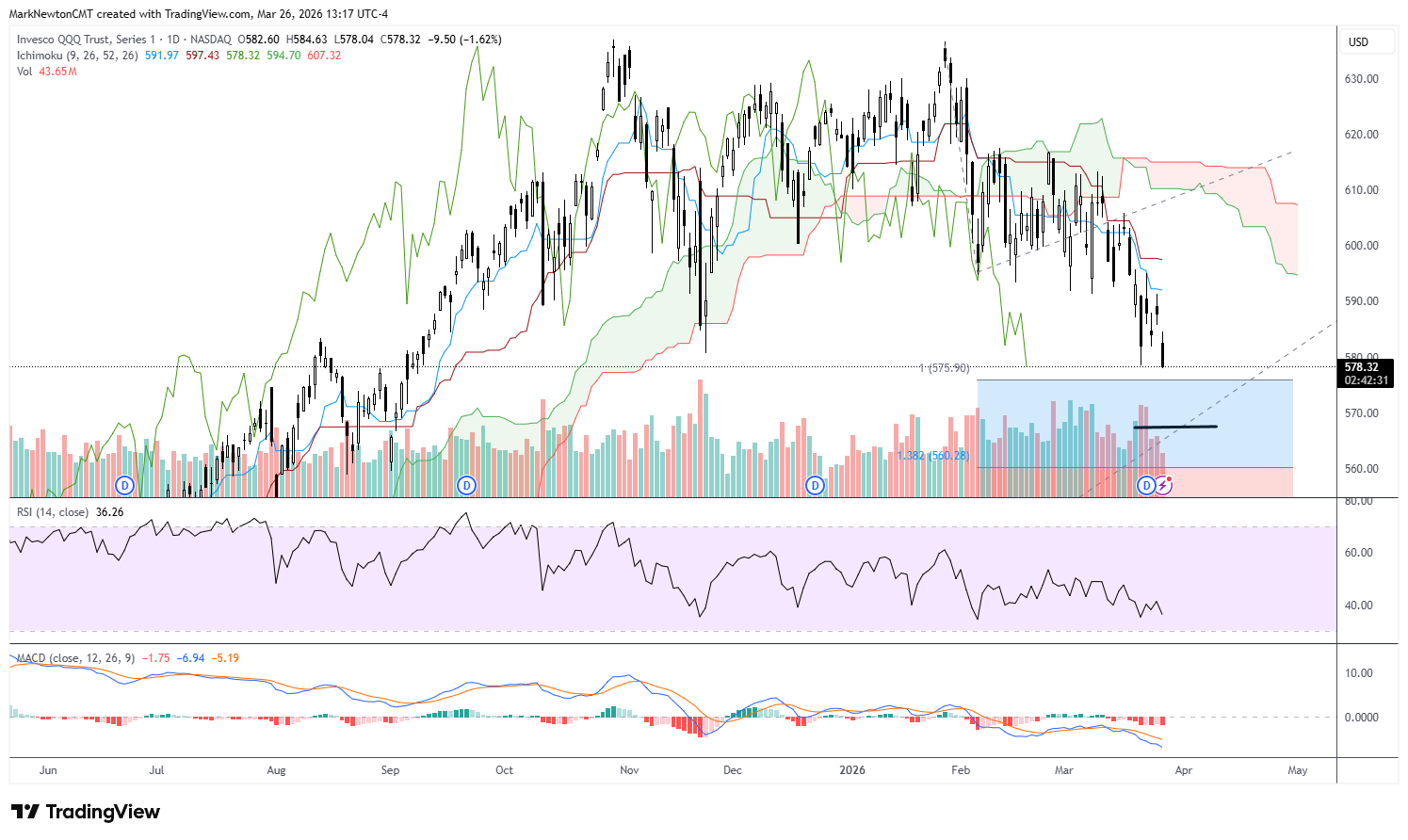

Head of Technical Strategy Mark Newton is paying attention to the opposite signs in the market. He pointed out that expectations for where five-year interest rates would be in five years from now have declined, while 1-year break-even inflation rate has surged, suggesting that “the implication is that the Fed will come in to squash inflation by hiking.”

Newton also doesn’t believe that markets are through the worst of the sell-off, in apparent contrast to Xuan and Lee. “The bears certainly have cropped up, but the bullish levels are not really showing capitulation,” he said. “My thinking is we need to see some bulls capitulate, and that would be more indicative of a potential low.”

As for buying the dip, he’s still not convinced this is a good time.

“I think we probably have one more shoe to drop, and if that happens in the next few weeks, I’d be inclined to say, ‘OK, hold your nose and buy,’” he said. “I think we’re getting close. I just don’t sense that we’re there just yet.”