In some ways, last week was like a mirror image of the week that preceded it. Whereas stocks began the earlier week strongly before giving up most (but not all) of their gains on Friday, last week began with a minor selloff before strengthening into Friday’s close. With this strengthening, the S&P 500 continued its weekly win streak, which now stands at eight – the longest since December 2023.

It’s a week that saw some key earnings reports, most notably from Nvidia. By any usual measure, Nvidia’s results would be viewed superlatively: the chip giant reported revenues rising 85% YoY to hit a record $81.6 billion, with earnings beating and gross margins at 74.9%. But this is Nvidia, a company from which investors habitually see big numbers. As Fundstrat Head of Research Tom Lee observed, “the stock barely reacted to the report. This arguably reflects markets expecting good results,” he suggested, but he viewed them as nevertheless “astounding” and “impressive.”

On Friday, Kevin Warsh formally took the helm of the Federal Reserve. Lee sees a fundamental policy decision awaiting him and the central bank: which matters more to structural inflation, oil prices or AI? Oil prices slid last week but remain elevated, with WTI crude at around $97 as of Friday afternoon. This could push up inflation – and if the effect persists, it could thus increase the Fed’s inclination to hike rates in the future. This possibility was already foreshadowed in the minutes from the April 29 Federal Open Market Committee (FOMC) meeting.

On the other hand, though AI might have a short-term inflationary effect due to its consumption of energy and its effect on chip prices, its likely downward impact on employment and worker wages will arguably have a deflationary effect, thus giving the Fed a dovish inclination.

The developing interplay between these two factors will be important to monitor. “Timing is key and which of these forces becomes the primary narrative in 2026 is key,” in Lee’s view.

Chart of the Week

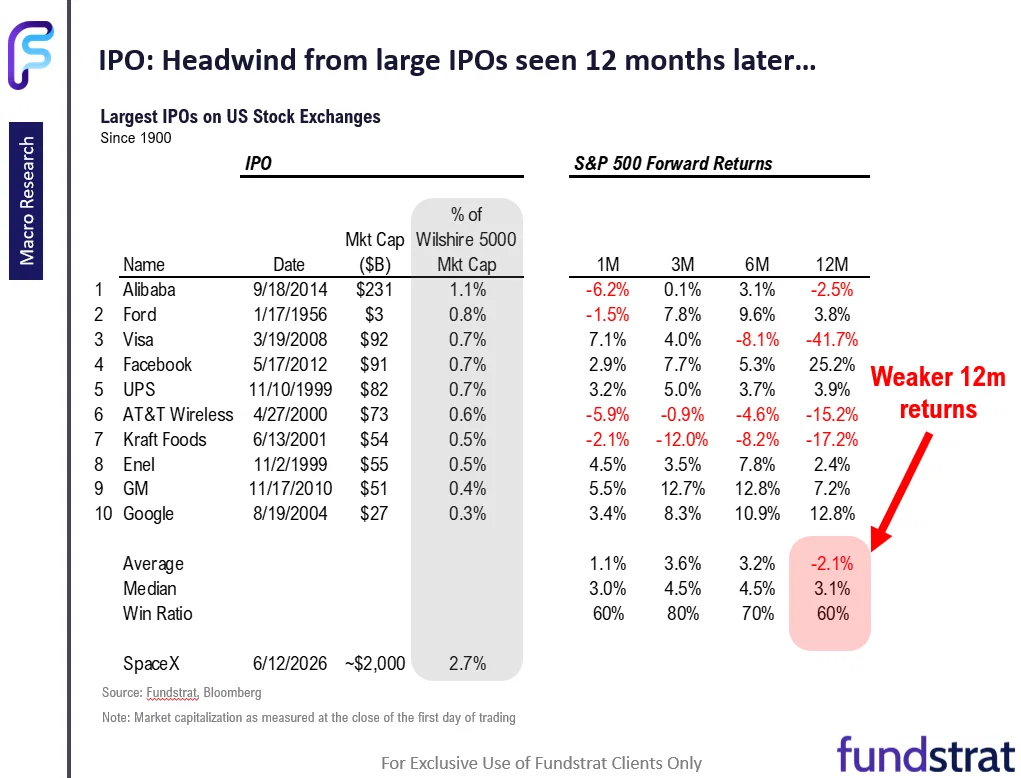

SpaceX formally announced its IPO plans last week, and it is slated to be the largest U.S. IPO ever, with the company’s pre-money valuation representing 2.7% or more of the total U.S. equity market. Investors also have high expectations for the IPOs of OpenAI and Anthropic, expected for later this year. These large public debuts raise questions about how they will affect the broader market overall. As Fundstrat Head of Tom Lee explained, “an IPO represents a sizable increase in equity supply,” with the impact generally coming about six to 12 months later after lockup expirations for shares held by early investors take place and the shares become tradeable. Our Chart of the Week shows how this manifested after the 10 largest U.S. IPOs. to date, and it is worth keeping in mind further down the road.

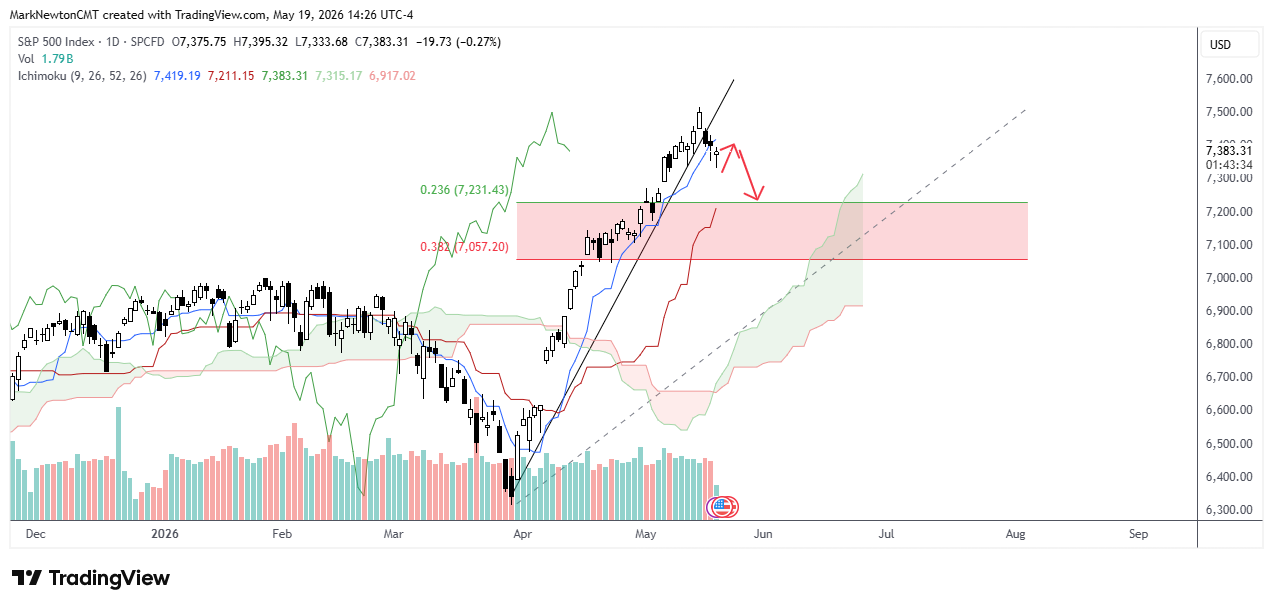

I’m out of the office this week, but important to communicate that a minor selloff has gotten underway, but one which i don’t feel has enough downward force to reach 7000 which was thought likely last week. As shown below, ^SPX officially broke its uptrend along with initial Ichimoku support (Tenkan-sen) and looks to have carved out a minor low as of intra-day basis today. If this is correct, then a mild bounce attempt could happen which then fails and turns down towards 7175-7245 in ^SPX, or a bit above 7000 which would liine up with a secondary area of Ichimoku-based support. In plain English, a mild selloff looks to be underway, but might prove somewhat short-lived into end of week this week or early next week before another rally back to highs gets underway. This daily chart shows the minor trend break and the expectation of a possible trajectory for SPX in the days ahead. Overall, I think it’s right to look for support to show up a bit sooner and at levels a bit higher than 7000, so 7175-7245 looks proper for now.

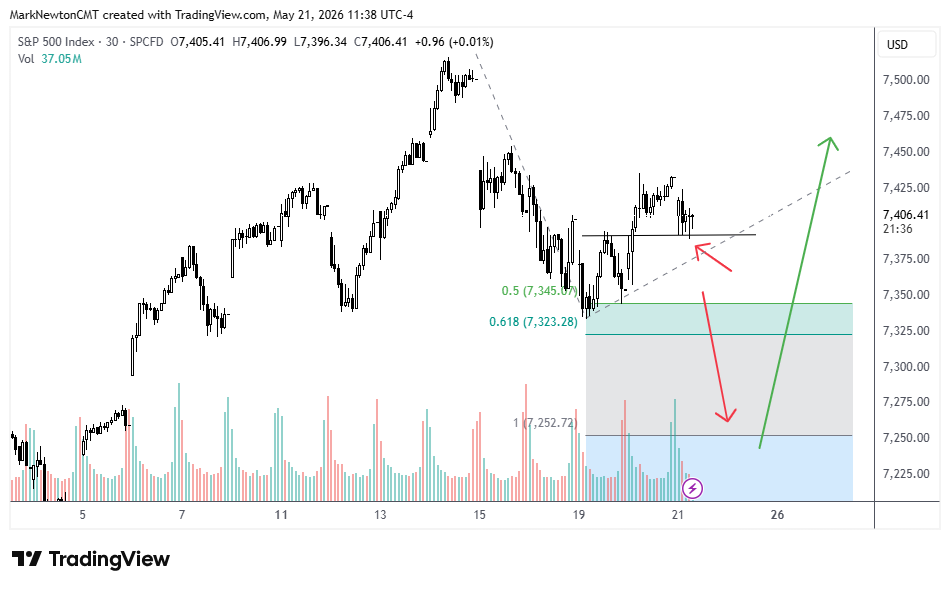

Thus far, the short-term tactical playbook seems to be on course with the selloff into Tuesday leading to a minor bounce Wednesday and now today starting to stall out. 10 of 11 sectors are lower today but only Industrials and Staples are lower by more than -0.75%, while US Dollar, Yields higher and precious metals lower. The near-term key area to focus on into this afternoon revolves around 7389 which has provided mild stabilization over the last few hours heading into Mid-day. As hourly charts show below, a break of this would also violate the minor bounce on Tuesday near that same level. Thus, a violation would undercut a short-term area of important support and likely means that a 3-5 day pullback down to near 7250 should be underway. For those that wish for more evidence, Tuesday’s lows of 7335 cannot be broken without resulting in a likely “equal-leg” decline similar to the 5/14-5/19 pullback, which should put SPX down under 7300 into early next week. However i am not expecting much more weakness, and expect that such a move would make SPX attractive to buy dips for a push back higher to new highs into June. Overall, my expectation is that US indices “could” be starting a “C wave” lower of an ABC corrective pattern that should ultimately prove buyable into next week. For today, important to keep a close eye on 7389, as an hourly close under this level indicates our short-term selling pressure to break this week’s lows is underway. (FInally, Crude oil turning back higher temporarily is thought to possibly happen as SPX is falling but ultimately, Crude looks to be in the final stages of its advance and a coming decline could get underway starting in late May. (not shown) ^SPX hourly chart shown below

Tuesday’s elections provided another big win for President Trump and strengthened his position as the dominant force in the Republican Party. The primary defeat of Kentucky Representative Thomas Massie continued the President’s winning streak of defeating Republicans who oppose his ideas. This follows the weekend primary defeat of Louisiana Senator Bill Cassidy. Any Republican defies the President at their own peril.

This research is for the clients of Fundstrat Direct only. Fundstrat Direct Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or Fundstrat Direct at fundstratdirect.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of Fundstrat Direct. At the time of publication of this report, Fundstrat Direct does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

Fundstrat Direct is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

Fundstrat Direct is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of Fundstrat Direct (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by Fundstrat Direct clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of Fundstrat Direct, which is available to select institutional clients that have engaged Fundstrat Direct.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

Fundstrat Direct does not have the same conflicts that traditional sell-side research organizations have because Fundstrat Direct (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by Fundstrat Direct and/or affiliates of Fundstrat Direct. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of Fundstrat Direct.

This research is for the clients of Fundstrat Direct only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but Fundstrat Direct does not warrant its completeness or accuracy except with respect to any disclosures relative to Fundstrat Direct and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where Fundstrat Direct expressly agrees otherwise in writing, Fundstrat Direct is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fundstratdirect.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.