“You see us as you want to see us – in the simplest terms, in the most convenient definitions. But what we found out is that each one of us is a brain … and an athlete … and a basket case … a princess … and a criminal […] Sincerely yours, the Breakfast Club” – The Breakfast Club (1985)

On the relatively rare occasions that social commentators mention Generation X, it’s to acknowledge that Generation X is the “forgotten generation.” Small wonder, since this generation is smaller in number than the Boomers who preceded them – and the two generations that followed them as well.

Yet to use boxing parlance, Generation X has punched above its weight class in the worlds of business and technology. Despite being mocked as the Slacker Generation, Xers can count some notables in their ranks. Well-known Xers include the founders or co-founders of Google, YouTube, Twitter/X, Dell, Palantir, and PayPal. Elon Musk is an Xer, and so, too, are Microsoft’s Satya Nadella, Alphabet’s Sundar Pichai, and AMD’s Lisa Su.

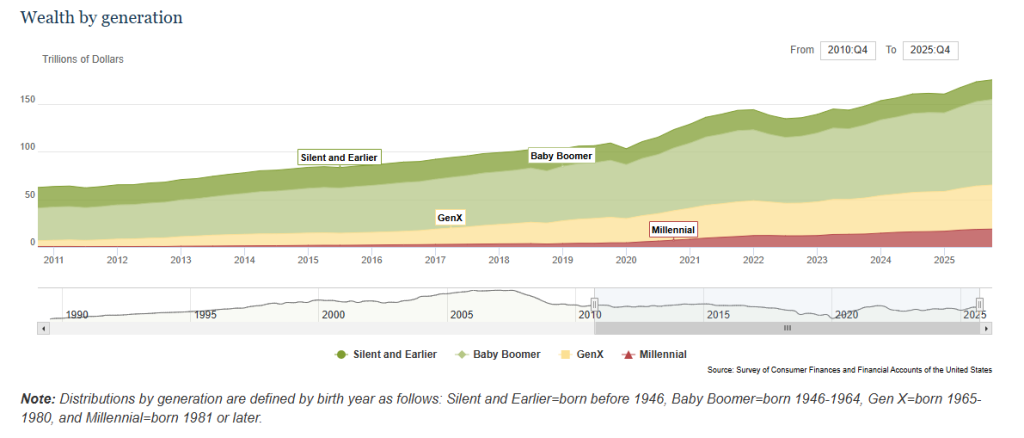

These days, Generation X as a whole is slated to play an outsized role in the economy, as well. It currently controls $46.24 trillion (26.4%) of the nation’s wealth, second only to the Boomers. What’s more, Generation X is at a confluence of several major trends that mean that this share is likely to grow.

For one thing, the members of GenX are currently in their peak earning years. The oldest Xer is now 61, and the youngest is 46. Median incomes for this generation, both individual and household, currently exceed those of any other generation in the U.S. – more than the Boomers who have begun their transition into retirement and more than middle-aged Millennials who are only beginning to age into higher-paying senior-level jobs.

That buying power is likely to increase. Though we often speak of the anticipated wealth transfer from Boomers to Millennials, the truth is that GenX is poised to be almost as big a beneficiary of this same trend. Importantly, the wealth transfer to Xers is likely to happen first. Intuitively, this makes sense: older Boomers tended to have children before the younger ones, and those older Boomers thus tended to have children during GenX birth years. One study suggests that GenX as a whole stands to inherit almost $1.4 trillion a year for the next 10 years – in the intermediate term, more than any other generation, even if the larger Millennial cohort could ultimately end up inheriting more.

While the above might suggest that Generation X is doing quite well for themselves, the bigger picture is not as rosy. Every generation is shaped by major historical events. In the case of Xers, this is a generation that faced a number of challenges.

Generation X entered working age during the economic recession of the early- to mid-1990s. Those who managed to get jobs right away nevertheless entered the workforce at a time when pensions were being phased out in favor of defined contribution plans (e.g., 401k accounts). Many Xers started their careers at companies that offered neither pensions nor 401ks, and even those who were offered access to a defined-contribution retirement account often failed to recognize their importance, because a widespread awareness of properly proactive retirement planning had yet to emerge.

Those who did understand the importance of investing got hit by the collapse of the dotcom bubble and then, a decade later, by the global financial crisis – which combined a collapse in home prices with a stock market crash. Perhaps no generation lost a larger percentage of their net worths in these two major economic events.

It’s no surprise, therefore, that although Generation X is slated to hit retirement age in five to 20 years, a PwC study suggests that 67% of them are seriously behind schedule in their financial security, with less than $100,000 saved – far less than the $1 million benchmark many financial advisors suggest. A separate study by the National Institute on Retirement Security is perhaps more alarming, reporting that within the bottom quartile of Xer households by income, the median household has just $200 (not a typo) saved for retirement.

(For those wondering how to reconcile the glum picture in the preceding paragraph with the financial strength described earlier, the answer is simple: what we currently call the K-shaped economy, with stark wealth disparity, arguably started with GenX: the wealth gap between the top 20% and bottom 20% of Xers is far larger than the equivalent gap of the Boomer cohort.)

Yet regardless of its intragenerational wealth gap, GenX still wields considerable spending power. Despite making up just 19% of the U.S. population, it also accounts for 31% of all retail spending. The generation generates the highest revenue per shopper.

It’s not necessarily a matter of consumerism or frivolity. One study suggests that as many as 31% of Xers are members of the so-called “Sandwich Generation.” That’s a more appetizing way of saying that they are stuck in between caring for aging parents while simultaneously also caring for young children – trying to make their paychecks cover both goals while still saving for retirement. In effect, Xers have a degree of financial decision-making that magnifies their influence because members of this demographic have a higher-than-expected likelihood of making spending decisions for three different generations.

The investing implications

One might expect that a generation that was burned by the dotcom crash and the GFC would be quite risk averse in their investment decision-making. Yet just the opposite seems to be true. In this bifurcated generation, it’s easy to come up with a theory for why those that have come through the various financial crises of their adult lives robustly – whether through savvy financial moves, outlier levels of professional success, or the luck of family support – remain enthusiastic participants in growth-oriented investing. The markets have treated them reasonably well, and they have the resources to insulate them from the negative short-term effects of higher levels of volatility.

Yet for those Xers who are juggling multiple burdens despite not being on the fortunate end of the wealth spectrum, preparing for retirement is simultaneously becoming more challenging and more urgent. To put it bluntly, many are desperately swinging for the fences. A Northwestern Mutual survey suggests that there’s a sharp increase in risk appetite when comparing Boomers to GenX, as measured by those investing in (or considering investments in) volatile assets like options, cryptocurrencies, meme stocks, and even sports betting/prediction markets. Tellingly, 66% of GenX respondents said they were making more aggressive moves because they “feel financially behind and believe high-risk/speculative investments will help reach financial goals more effectively than traditional methods.”

Whether you agree or disagree with this approach, what all of this suggests is that GenX as a whole represents a tailwind for risk assets in general. It also therefore represents a tailwind for companies to provide access to both risk-assets trading and prediction markets. This includes companies such as:

- Robinhood HOOD -2.67%

- Coinbase COIN 2.45%

- Interactive Brokers IBKR 4.90%

- Intercontinental Exchange ICE 1.15%

- CME Group CME 0.60%

Spending habits

Their disproportionate representation in the “Sandwich Generation” has an impact on the spending habits of many Xers, both affluent and less so. It hardly needs to be noted that those juggling careers with caregiving for both parents and children have a deficit of something money cannot buy – time.

Companies that can save time and deliver convenience are likely to be in high demand. That includes those that help deliver groceries and meals, like Doordash DASH 1.33% and Instacart CART -2.10% . It also includes companies that are ramping on e-commerce. Familiar names in this space include Amazon AMZN 4.78% , Walmart WMT -2.95% , and Target TGT -0.85% .

As they strive to help aging parents, Xers are also looking into products and services that can help their parents age at home. Companies appear positioned to capitalize on this trend include

- Best Buy BBY -2.27% . The consumer electronics retail giant is turning its “Geek Squad” at-home tech-support operations into a team that can assist its Best Buy Health division with the implementation and installation of age-at-home solutions, including medical alert buttons, fall-detection, ambient home monitoring systems – all of which enable Xers to remotely monitor the wellbeing of parents who insist on continuing to live in their homes.

- Abbott Laboratories ABT -2.40% . Abbott Laboratories targets many of the chronic health issues that often force seniors to give up on living independently and either move in with adult children or into senior residences/facilities. Among Abbott’s products are remote automated diabetes (blood sugar) monitors and implantable heart monitors.

- Addus HomeCare ADUS -2.67% . Unlike Best Buy and Abbott, Addus is entirely focused on home care, providing home-health assistants who can visit seniors’ homes to assist in various tasks ranging from meal preparation to bathing and medication reminders. The company’s services include helping harried Xers navigate the labyrinthine U.S. healthcare and health-insurance system.

- CVS CVS -0.79% . Through CVS Health and through CVS’s 2023 acquisition of Signify Health, CVS is moving beyond retail pharmacies and pharmaceutical benefits to expand into in-home health care. Signify specializes in in-home health evaluations, sending doctors, nurses, and physician assistants into homes to assess elderly fitness and living conditions, and to conduct home-safety assessments.

For the most part, however, it’s worth assessing the spending trends of wealthy and less-wealthy Xers separately. While many marketing surveys report that Millennials and Zoomers prize experiences more than material goods, that’s actually a trend that originated with the age group that preceded them.

The aging X generation understands that you can’t truly enjoy the good life without good health. As a result, they are among the leading spenders on preventative health, anti-aging, longevity products and services such as those provided by:

- Life Time Group Holdings (LTH -2.79% ). Life Time runs a chain of premium athletic clubs, a growing number of which are expected to begin offering MIORA, an in-house precision medicine platform that offers personalized workouts, hormone optimization, and metabolic/nutritional plans targeted at affluent Xers looking to maximize their lifespans.

- Hims & Hers Health (HIMS 9.58% ). Hims & Hers is a leading provider of anti-aging and preventative therapies, treatments, and supplements, including prescription-strength skin treatments, hair regrowth, and weight-management programs and products (including some types of GLP-1 treatments).

This demographic segment also explains why GenX accounted for 42.8% of global luxury travel revenue in 2025, the biggest share of any generation. Among the leaders in luxury travel of the X variety include Marriott MAR -1.93% , Hilton Worldwide Holdings (HLT N/A% ), and Hyatt Hotels Corporation (H -5.89% ). All three hospitality giants have been explicit in expanding their luxury portfolios with an eye toward affluent Xers, incorporating high-end, “curated” experiences into their offerings.

As for their less financially advantaged generational cohorts, spending tends to be far less discretionary. In fact, lower-income Gen Xers often struggle to make ends meet, relying on credit cards and carrying hefty credit card balances.

A Bankrate study shows that 53% of Generation X carries credit-card debt, while Experian data suggests that the average Xer credit-card balance hovers around $10,000. Both numbers are higher for GenX than any other generation in the U.S. For reasons discussed above, this is understandable and not surprising. If this trend continues, then companies poised to benefit include:

- Capital One COF 0.73% , one of the largest credit-card issuers in the U.S.

- Synchrony SYF 2.88% , a major provider of private-label/store-branded credit cards

- Encore Capital ECPG 0.49% , a purchaser (and collector) of defaulted debt, including credit-card debt.

In conclusion

Generation X was often referred to as the latchkey kids, left to fend for themselves as their parents focused on other matters. Yet perhaps they continued to be overlooked because this cohort was particularly difficult to lump into a single homogenous group with a defining set of characteristics.

In some ways, as we’ve discussed above, that is still the case. There’s no simple, uniform answer to what Gen X needs and wants, and the bifurcation in wealth seen in this generation means that there might not ever be. Hopefully, this piece has provided some insights about how to view and assess both forks of Generation X – and why both business and investors should take the time to do so.

That said, as always, Signal From Noise should not be used as a source of investment recommendations but rather ideas for further investigation. We encourage you to explore our full Signal From Noise library, which includes deep dives on the recent memory chip gold rush, the future of malls, drone warfare, and the Trump portfolio. You can also find our take on space-exploration investments, defense stocks, and the business of farming.