This year’s stock-market party has been almost entirely concentrated in semiconductor stocks, prompting many investors to question if it’s time to diversify into the Lag Seven, known as the Magnificent Seven in their heyday.

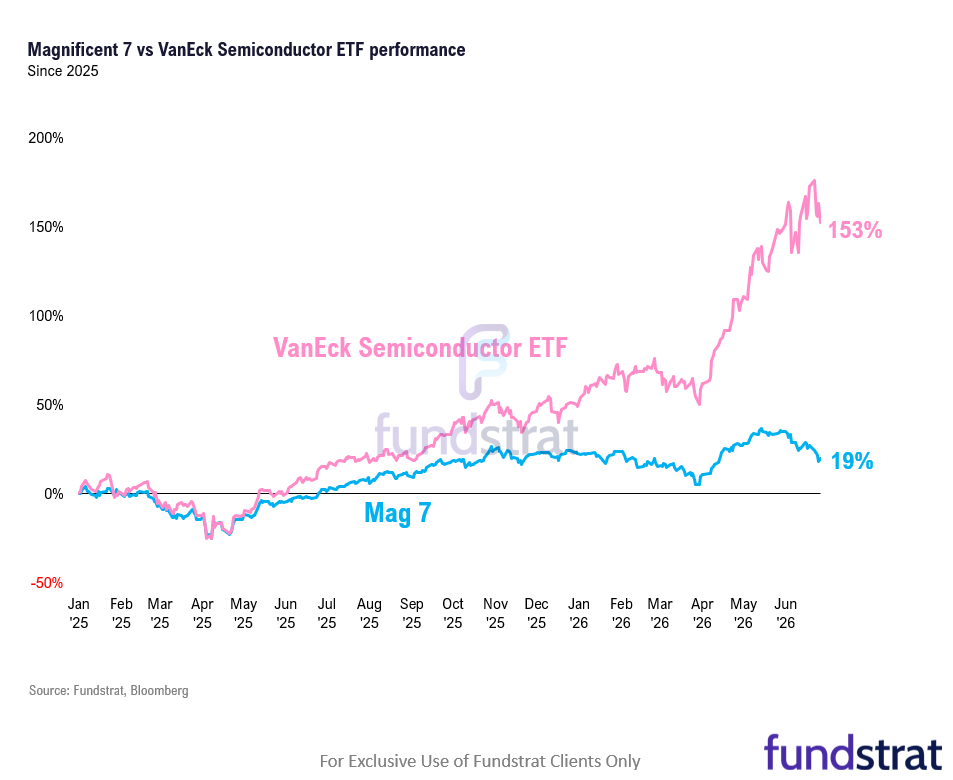

Shares of Magnificent Seven—which includes Nvidia, Apple, Microsoft, Alphabet, Amazon, Meta, and Tesla—are up 19% since 2025, while the VanEck Semiconductor ETF (SMH -4.06% ) has rallied 153% over that period. The ETF includes shares of everything from Nvidia to Intel to Micron to Broadcom.

The investing puck recently has moved away from the hyperscalers toward semiconductors because memory and storage is the real bottleneck now, leading to a bifurcation in the tech trade. Hyperscalers were the ones who first got investors excited about the prospects of AI. They spent billions building out AI infrastructure, convincing everyone along the way that figuring out how to monetize the large investments doesn’t matter, what mattered was the speed. That was their shortcoming—not foreseeing that the bill would come due one day.

The last time the Magnificent Seven (MAGS 1.11% ) were down this much so far in a year compared to the S&P 500 was in 2022.

Semiconductor stocks instead have been not only benefitting from the wave of AI investments, but also printing money from it. Shares of Micron (MU -6.30% ), for example, rallied 16% on Thursday, a day after its quarterly earnings showed that revenue surged 347% and profit grew 1,394% from a year ago. Its shares are up 259% in 2026. Other memory and storage players like Sandisk (SNDK -9.94% ), Western Digital (WDC -13.61% ), and Seagate (STX -12.33% ) have rallied 660%, 212%, and 213%, respectively, in 2026. Those three are not a part of the semiconductor ETF.

Commentary from Micron’s executives during the earnings call also reaffirmed the memory industry is evolving past its historical reputation of boom and bust cycles. They expect supply will remain tight beyond 2027, up from only this year. Micron’s stock, in particular, has been the top contributor to the semiconductor ETF’s gain since 2025.

But big gains there have meant big volatility, too.

Despite the stellar earnings from Micron this week, it seemed like investors partook in some profit taking, which influenced the broader market, as well. The semiconductor ETF finished the week down 8.8%. (Korea’s Kospi index, which holds SK Hynix and Samsung Electronics, noted bigger swings, with circuit breakers kicking in. It finished the week down 6.1%.)

Investors who felt anxious after seeing those gyrations in highflying semiconductor stocks might find some comfort in the safety of the Magnificent Seven, whose businesses aren’t just one-trick ponies. They have a diversified revenue base that predates AI, and AI feeds back into those core engines rather than being a standalone bet.

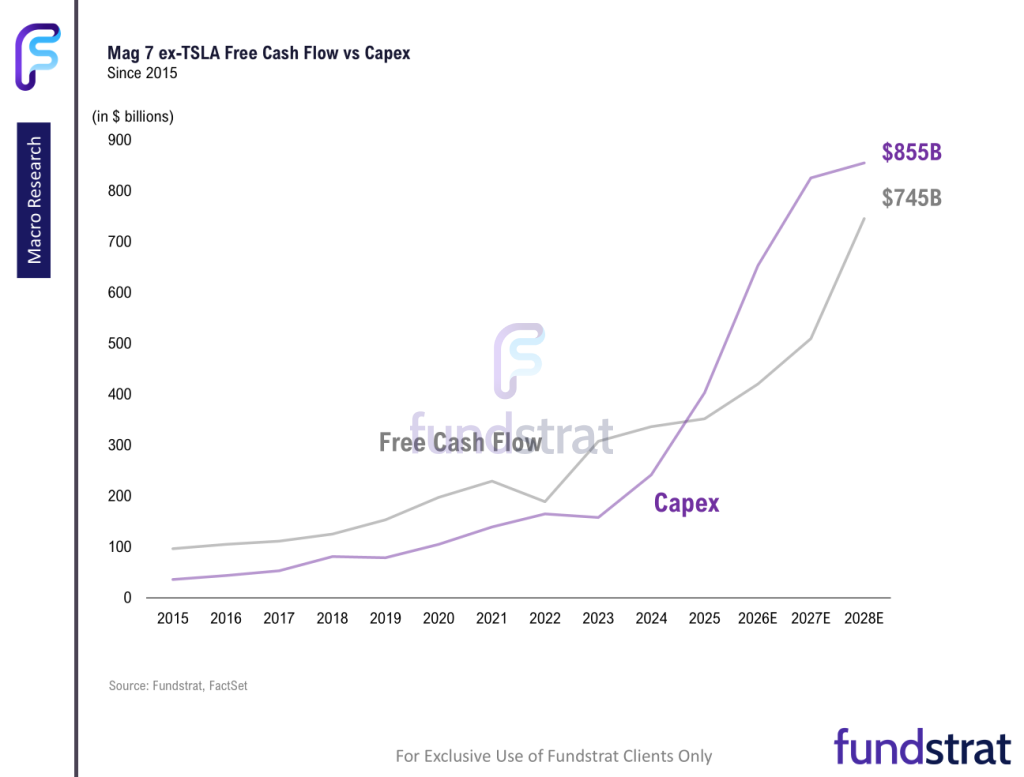

Since 2025, the Magnificent Seven’s capex spending has exceeded their free cash flow, and it’s expected to continue to be that way. However, the gap isn’t that large. In 2028, the Magnificent Seven ex-Tesla are expected to have $745 billion in free cash flow, compared to $855 billion in capex.

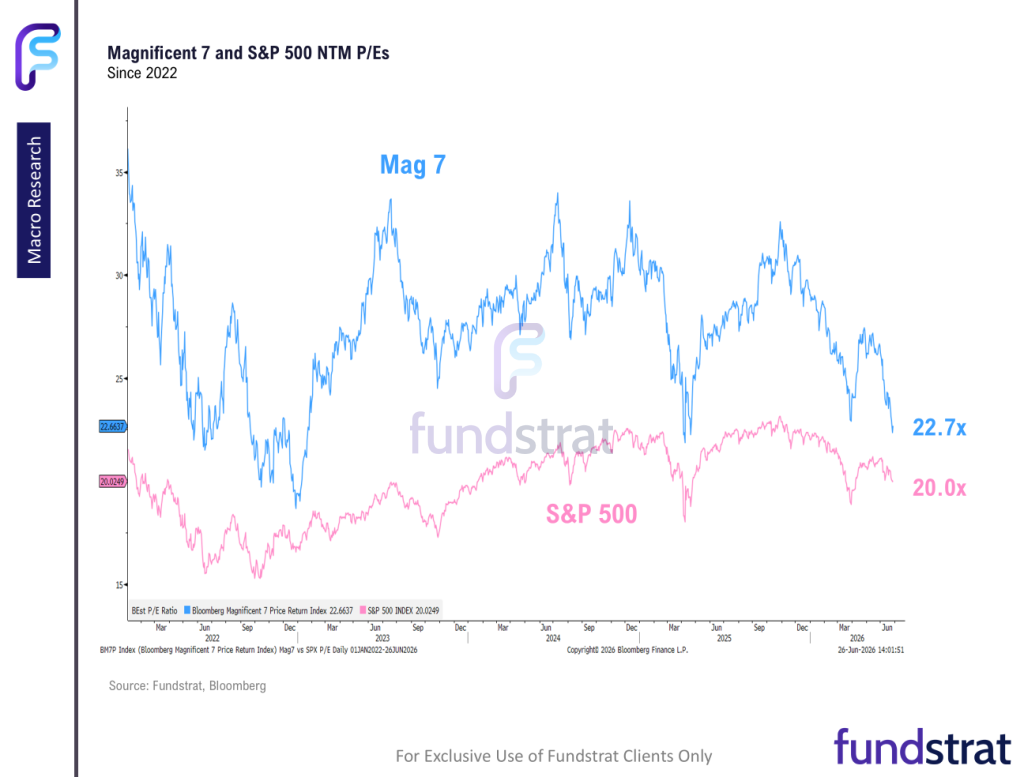

Shares of the Magnificent Seven are also trading at a discount. On a forward earnings basis, the gap between the Magnificent Seven and the S&P 500 is the narrowest since January 2023, so at some point, it’s worth asking if prices have declined enough to the point where the stocks look attractive again.

Technical indicators also seem supportive. Fundstrat Head of Technical Strategy Mark Newton said this week that the underperformance in the Magnificent Seven now looks mature and weekly DeMark exhaustion is present on the Magnificent Seven against QQQ -1.49% relative chart.

“This looks to be in the final stages of this pullback; time to start looking for a low,” he wrote this week.

With that being said, here’s the business models of the Magnificent Seven ex-Tesla:

1) Apple (AAPL 2.49% )

- Apple barely has an AI segment, which is the point. It continues to remain focused on being a services and a hardware multiplier. AI here is explicitly framed by management as the next leg of services monetization rather than a hardware story — Apple Intelligence and the Siri revamp are designed to deepen the high-margin services annuity and drive the hardware upgrade cycle.

- In the latest quarter, iPhone revenue was $57 billion, up 21.7% from a year ago, Mac was $8.4 billion, up 5.7%, iPad was $6.9 billion, up 8%, Wearables/Home was $7.9 billion, up 5%, and Services was a record $31.0 billion, up 16.3%. So the combined non-iPhone segments are 48.7% of revenue.

- Apple shares are up 4.7% this year.

2) Microsoft (MSFT 5.43% )

- Copilot monetizes an installed base that long predates it. Microsoft now has over 20 million paid M365 Copilot seats, up from 15 million in January, with weekly engagement reaching Outlook-level habit, according to the company’s earnings call. That’s AI sold as an add-on to the Office annuity, not a separate business.

- In the latest quarter, the productivity and business processes segment added $35 billion in revenue, up 17%, intelligent cloud was $34.7 billion, up 30%, and more personal computing was $13.2 billion, down 1%.

- Microsoft shares are down 21% this year.

3) Amazon.com (AMZN 2.09% )

- A hidden engine is advertising, not just AWS, which provides on-demand cloud computing platforms. Everyone frames Amazon’s AI story as AWS, but the latest earnings result shows the breadth: total revenue was $181.5 billion. AWS was $39.79 billion of that, and advertising grew to over $70 billion in the last twelve months, with AI helping improve its targeting.

- Amazon is using AI across the retail engine — logistics routing, inventory placement, recommendations, as well. So AWS is the AI segment, but AI itself is making the retail and ad businesses structurally more profitable.

- Amazon shares are up 2.7% this year.

4) Alphabet (GOOG -2.04% )

- The bear thesis was that AI chat would cannibalize Search, but Search revenue in the latest quarter still grew 19% from a year ago. Gemini’s enterprise users climbed and Cloud accelerated, up 63%. AI Overviews and AI Mode are layered into Search (defending the ad monopoly), Gemini drives Cloud.

- Alphabet shares are up 6.1% this year.

5) Meta (META 1.11% )

- Advertising is roughly 99% of revenue, but AI is the margin amplifier. It makes the existing engine dramatically more efficient: ad impressions globally grew 19% in the latest quarter from a year ago and average price per ad rose 12%.

- In the earnings call, executives said that more than 8 million advertisers used at least one of their gen AI ad creative tools, noting particularly strong adoption among small- and medium-sized advertisers.

- Meta shares are down 15% this year.

6) Nvidia (NVDA -1.71% )

- While data centers make up a majority of Nvidia’s revenue, it’s still diversified across AI end-markets from hyperscalers to model builders to AI clouds.

- Revenue for hyperscalers in the latest quarter was $37.9 billion, up 115% from a year ago, while AI clouds, which includes industrial and enterprise, was $37.4 billion, up 73%.

- The real “not a one-trick pony” argument for Nvidia is the moat layer: the CUDA software platform extends it into autonomous vehicles and robotics, with physical AI as the next wave.

- Nvidia shares are up 2% this year.

Conclusion

Across the group ex-Tesla, AI shows up in three distinct roles (1) as a margin amplifier on an existing engine like that of Apple, Meta, and Amazon (2) as an attach/upsell layer on an installed base such as Microsoft (3) as a defensive moat protecting the core franchise with Alphabet. Nvidia, the only AI pure-play, notes a breadth of AI end-markets plus the software ecosystem. All of these companies had a diversified, cash-generative business before the AI capex cycle started, and AI is raising the return on those existing assets rather than replacing them.

That said, as always, Signal From Noise should not be used as a source of investment recommendations but rather ideas for further investigation. We encourage you to explore our full Signal From Noise library, which includes deep dives on why investors should care about Gen Xers recent memory chip gold rush, the future of malls, drone warfare, and the Trump portfolio. You can also find our take on space-exploration investments, defense stocks, and the business of farming.